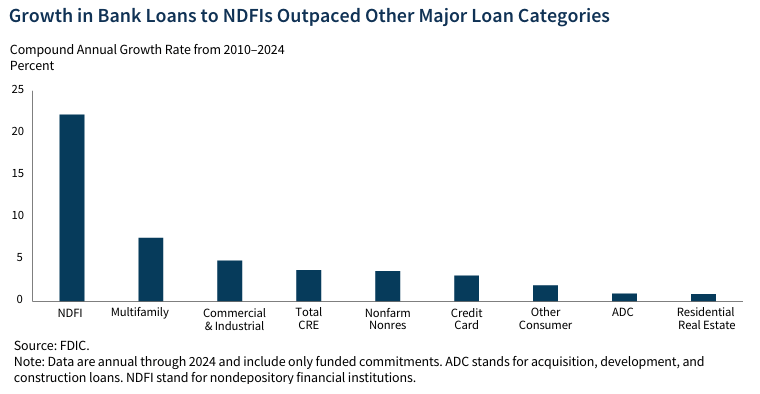

The rapid, sustained rise in loans from banks to non-depository financial institutions (NDFIs) — which grew at a 21.9% compound annual rate from 2010 to 2024 — increases systemic risk by creating intense interdependencies. These exposures, particularly through credit lines, can act as transmission channels for financial distress, as bank stability becomes directly tied to the performance of often-leveraged nonbank lenders.

The growing importance of non-bank financial institutions (NBFI)s also caught the attention of the Federal Reserve in recent study (Duque Gabriel & Sterling, 2025).

Both types of institutions operate outside the traditional banking system but are often interconnected with banks, posing different levels of risk.

Essentially, all NDFIs are NBFIs, but not all NBFIs are NDFIs, as some NBFIs can take specific types of deposits.

Key Differences:

- Definition & Scope:

- NBFI (Non-Bank Financial Institution): A broad category including investment funds, insurance companies, pension funds, and finance companies. Some NBFIs, such as certain finance companies, might take limited deposits.

- NDFI (Nondepository Financial Institution): Specifically refers to institutions that do not accept deposits from the public, such as mortgage lenders, private equity funds, and broker-dealers.

- Deposit Taking: NDFIs strictly do not take deposits, whereas the broader NBFI category can include entities that might hold specialized or time deposits.

- Funding Sources: NDFIs rely on alternative funding sources like equity, debt issuance, or bank credit lines.

- Focus: NDFIs often focus heavily on lending and credit intermediation (e.g., mortgage companies), while NBFIs cover a wider scope including asset management, insurance, and brokerage services.

The Fed’s study also highlight gaps in understanding NDFI’s role

- existing studies often focus on long-term averages rather than time-varying trends.

- the literature rarely quantifies the size of credit lines relative to GDP, despite their systemic importance.

- there is limited analysis of sectoral heterogeneity within the NBFI sector. By addressing these gaps, this study provides new insights into the evolving bank-NBFI nexus.

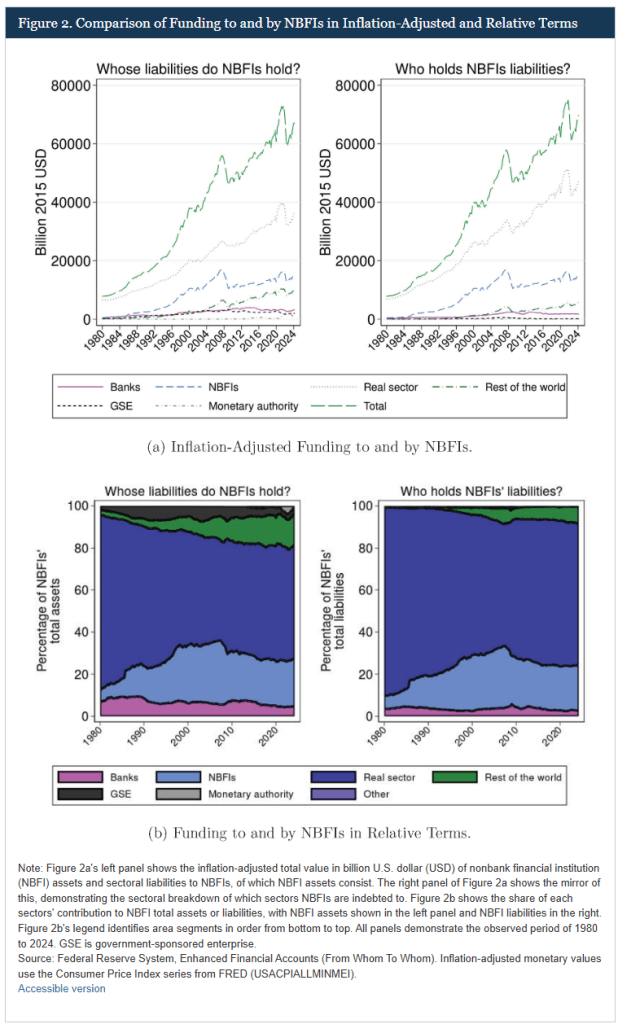

NBFIs have emerged as key intermediaries in the financial system, acting as both recipients and providers of funding within a complex network of interdependencies.

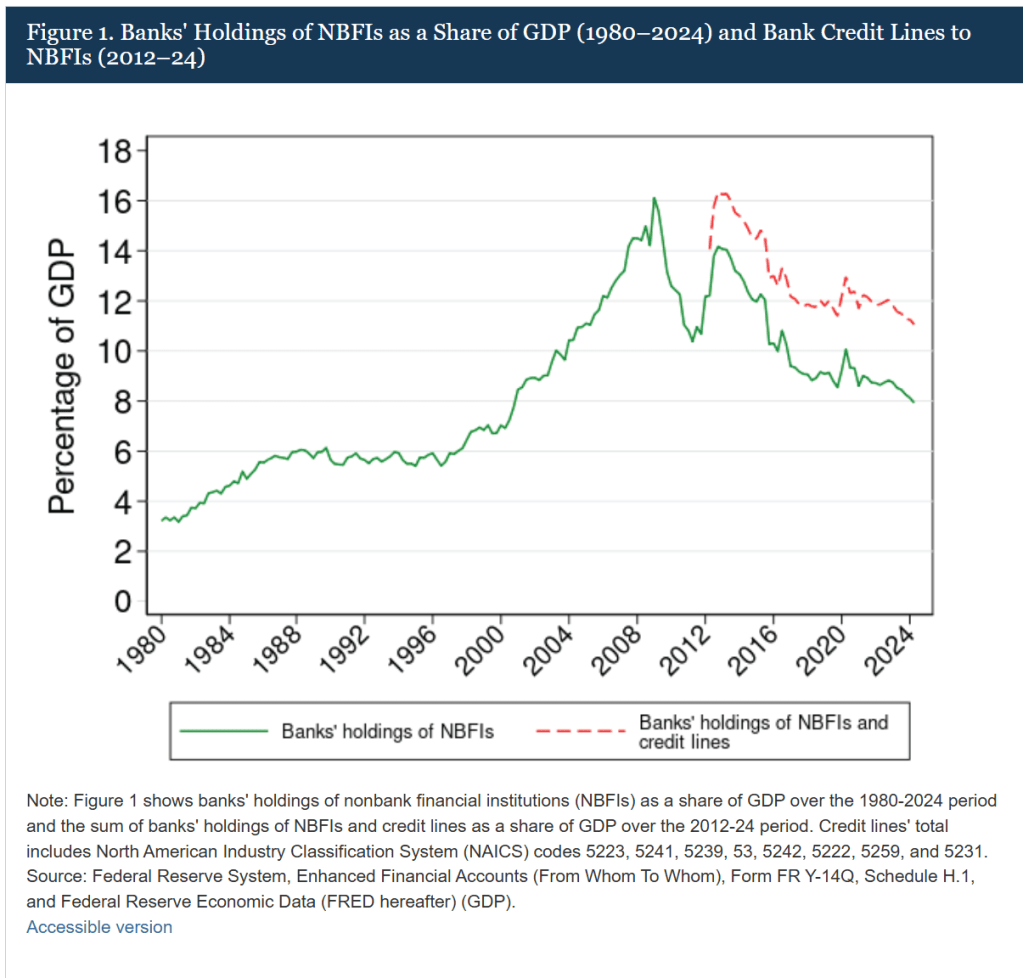

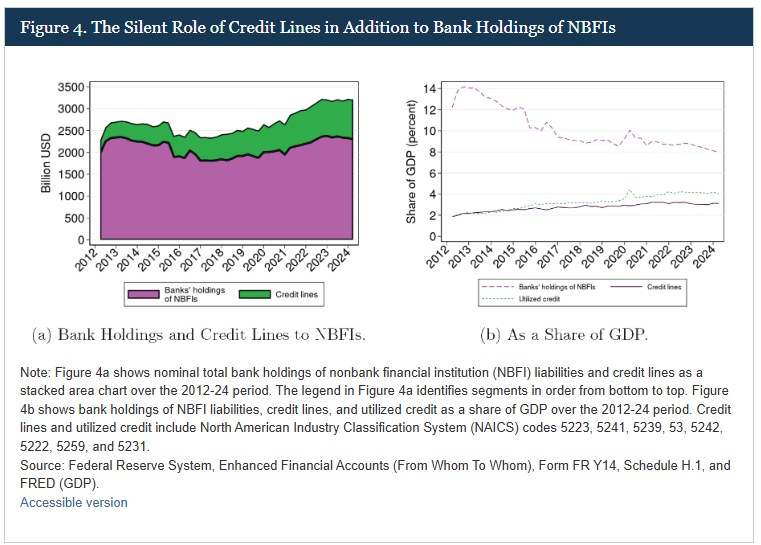

The Fed observes Ccedit lines to NBFIs have more than doubled since 2012, partially offsetting the decline in direct funding. This shift indicates a re-allocation of bank exposures away from direct holdings to contingent liabilities which are off-balance-sheet vulnerabilities.

NBFI credit lines is a significant systemic risk if drawn simultaneously during periods of stress.

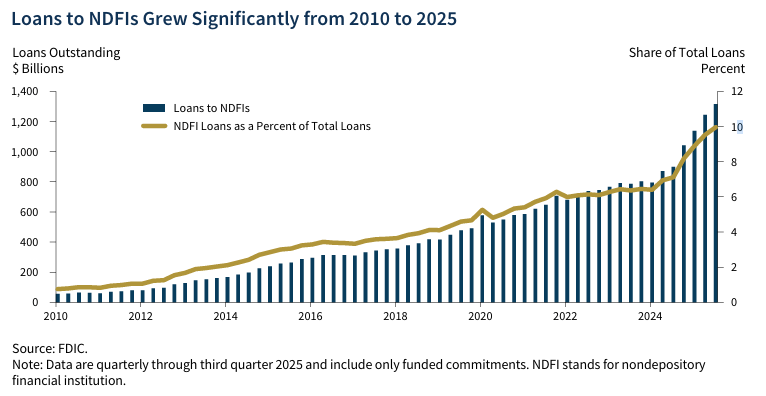

Focusing on NDFI segment in a recent paper published by FDIC (Federal Deposit Insurance Corporation, 2026), NDFI loan growth outpaces the next segment by 3x.

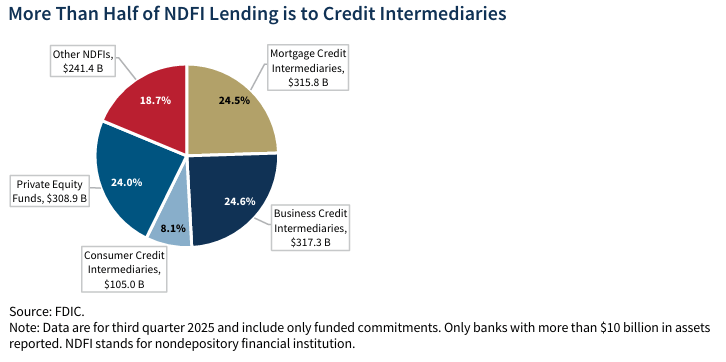

More than half of bank lending to NDFIs is to credit intermediaries, and about a quarter is to private equity funds.

Overall, while this lending offers revenue to banks, it creates a “transformed” risk structure where banks are indirect, highly exposed participants in the risks taken by nonbanks.

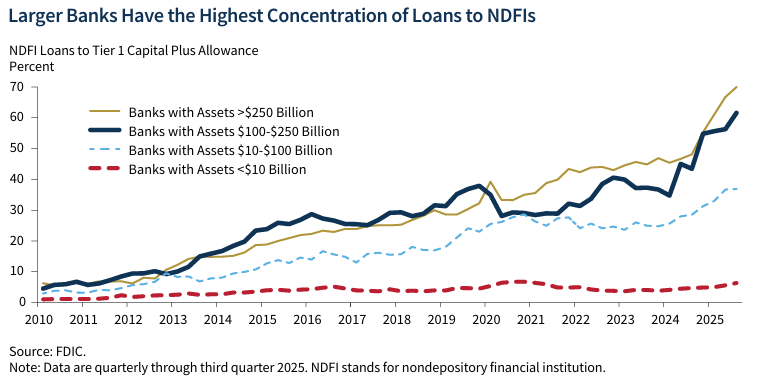

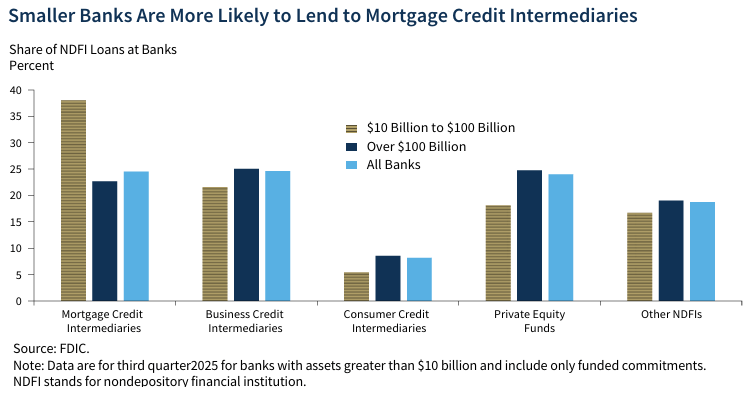

Large banks (>$100 billion) evenly distribute their exposure across private equity, business credit, and mortgage credit NDFI subcategories.

Regional banks (assets between $10 billion and $100 billion) see ~40% of NDFI lending in mortgage credit intermediation at almost 40 percent, while banks with assets greater than $100 billion.

The increased risk arises from three factors:

Rapid growth + risk concentration

- By 2025, it reached roughly 10–13% of total bank loans

- Large banks hold a disproportionate share of this exposure

Greater interconnectedness with “shadow banking”

- NDFIs are less regulated and more opaque than banks

- This creates complex links between regulated banks and less-regulated credit markets, which can transmit shocks

Structural vulnerabilities

- Private credit (a major NDFI category) can involve:

- higher leverage

- illiquid assets

- limited transparency

- These features can amplify stress during downturns.

Duque Gabriel, R., & Sterling, J. (2025, July 14). Shifting dynamics in bank funding of nonbank financial institutions: The rise of credit lines. Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/shifting-dynamics-in-bank-funding-of-nbis-the-rise-of-credit-lines-20250714.html

Federal Deposit Insurance Corporation. (2026, February 17). Bank lending to nondepository financial institutions. https://www.fdic.gov/analysis/2026-02/bank-lending-nondepository-financial-institutions