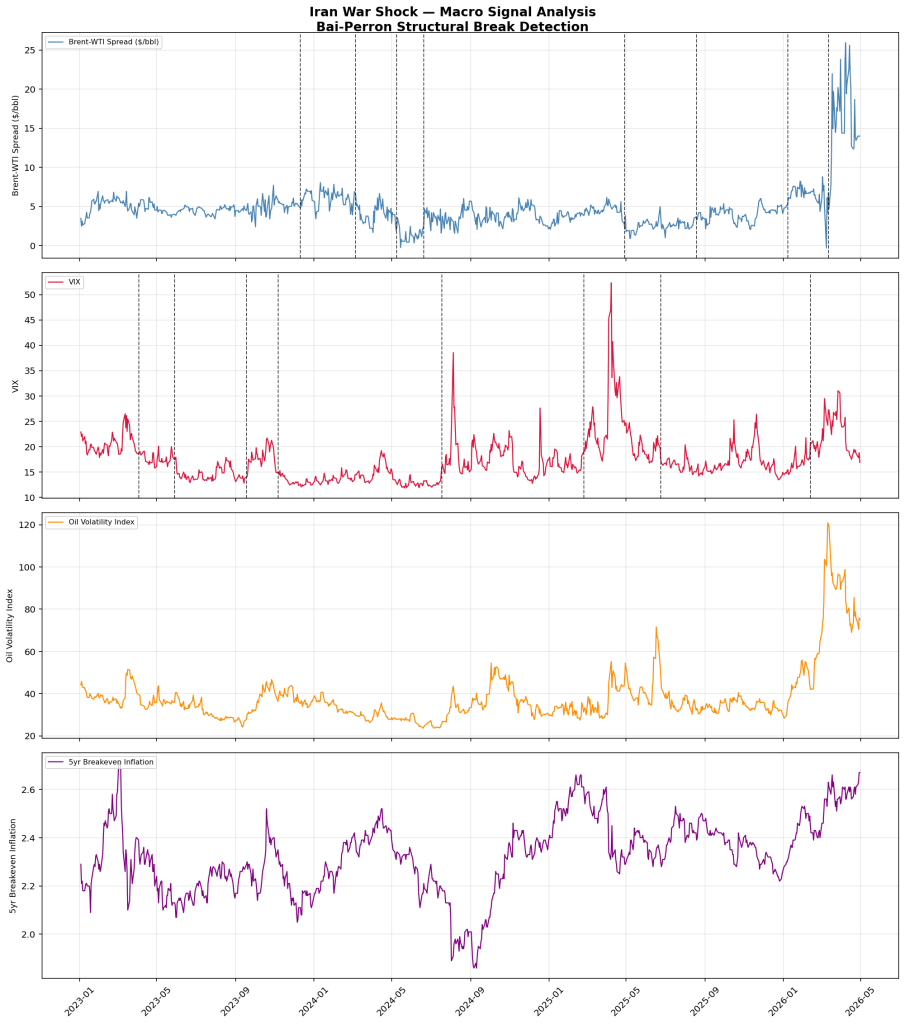

How does one detect a structural break in global oil markets subjected to geopolitical shocks (e.g., the Iran War)?

When did the Iran War signal a regime change in global oil markets?

Signal Detection

The Bai-Perron (2003) procedure endogenously detects multiple, unknown structural breaks in time series data. It flags regime breaks by identifying when parameters in a linear model change over time, providing consistent estimates of break dates, even with heterogeneous errors.

Bai-Perron can be implemented in Python using the ruptures library, which offers off-line change point detection in the analysis and segmentation of non-stationary signals (C. Truong et al. (2020)).

Implemented algorithms include exact and approximate detection for various parametric and non-parametric models. rupturesfocuses on ease of use by providing a well-documented and consistent interface. In addition, thanks to its modular structure, different algorithms and models can be connected and extended within this package.

The global nature of oil markets presents a range of possible time series signals to be considered:

WTI (West Texas Intermediate)

Very liquid US oil benchmark

Not directly exposed to Iran War risk

WTI has a history of decoupling from Middle East stress due to shale supply dynamics in the US.

Brent

Global seaborne benchmark with North Sea delivery

Captures the Europe/Asia demand dynamics and offers a better proxy for global supply disruption over WTI.

JCC (Japan Crude Cocktail)

Weighted average of crude imported into Japan

Dominated by Middle East sour grades

Published monthly reducing the timeliness of the signal.

Dubai/Oman

Physical Middle East benchmark sour crude.

Most directly exposed to Hormuz risk

However, Dubai/Oman is less liquid and is more difficult to access using public data (e.g., FRED api).

In considering the daily geopolitical risk of impending war strikes, we focused on 2 oil benchmarks available through FRED api:

Brent: global price signal

Brent-WTI spread: geopolitical premium signal isolating market demand fluctations. A sustained widening of Brent-WTI spread flags seaborne supply risk.

We considered three other signals:

VIX: financial system fear

5-year breakeven inflation: the commodity pass-through to inflation expectations.

WTI Crude Volatility (OVX): the VIX equivalent for oil

Observations

We examined the period January 3, 2023 – April 30, 2026 comprising 860 observations. This period encompasses the current hostilities, the 2025 war strikes, and the Tariff shock.

The Bai-Perron algorithm flagged breaks in the time series data.

Window

Brent-WTI

VIX

Gap (days)

Notes

Apr-Jun 2025

2025-04-29

2025-06-24

~56

Tariff Shock

Aug 2025

2025-08-29

–

–

No VIX

Jan-Feb 2026

2026-01-08

2026-02-12

~35

Strong

Mar 2026

2026-03-12

2026-02-17

~28

Close

The Jan-Feb 2026 signal cluster report is consistent with persistent commodity chain effects.

The Brent-WTI spreads presents a dramatic structural brak spiking from ~$5.bbk baseline to $15-25/bbl.

The OVX confirms this spike suustaining coincidental elevation and peaking ~120.

The 2025 breaks appear minor.

We identified the onset of the Iran War Shock regime via the Bai-Perron structural break detection on the Brent-WTI spread, a direct proxy for Hormuz supply risk, with the boundary confirmed by concurrent VIX elevation (2026-02-12).

References

Bai, Jushan; Perron, Pierre (January 2003). “Computation and analysis of multiple structural change models”. Journal of Applied Econometrics. 18 (1): 1–22. doi:10.1002/jae.659. hdl:10.1002/jae.659

Truong, C; L. Oudre, L; Vayatis, N. Selective review of offline change point detection methods. Signal Processing, 167:107299, 2020.

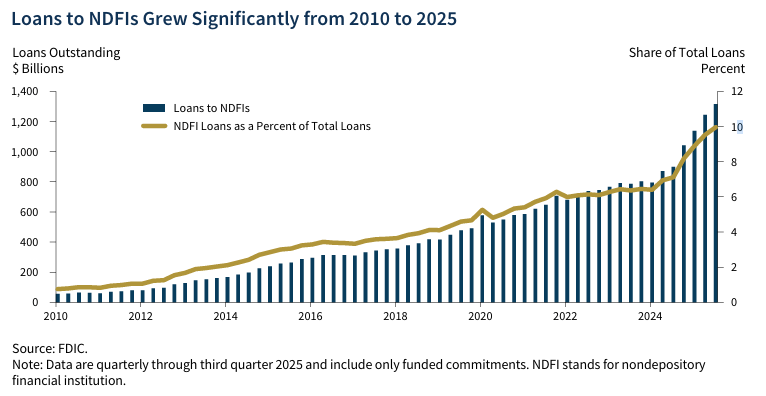

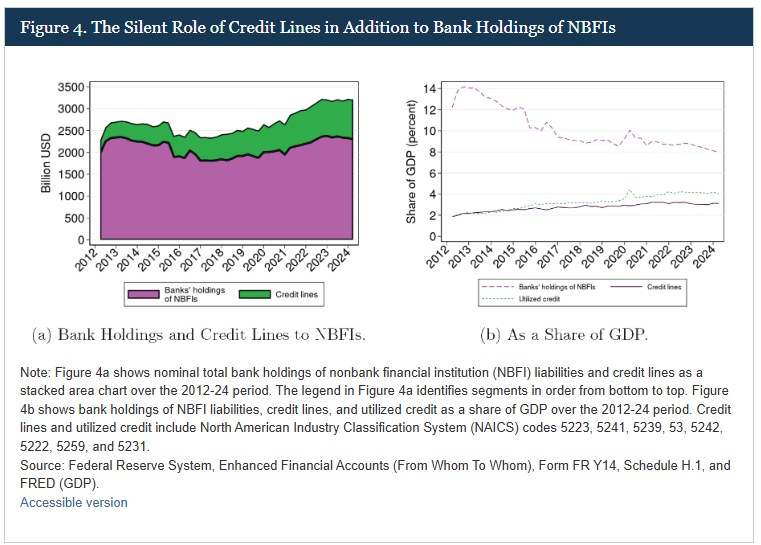

The rapid, sustained rise in loans from banks to non-depository financial institutions (NDFIs) — which grew at a 21.9% compound annual rate from 2010 to 2024 — increases systemic risk by creating intense interdependencies. These exposures, particularly through credit lines, can act as transmission channels for financial distress, as bank stability becomes directly tied to the performance of often-leveraged nonbank lenders.

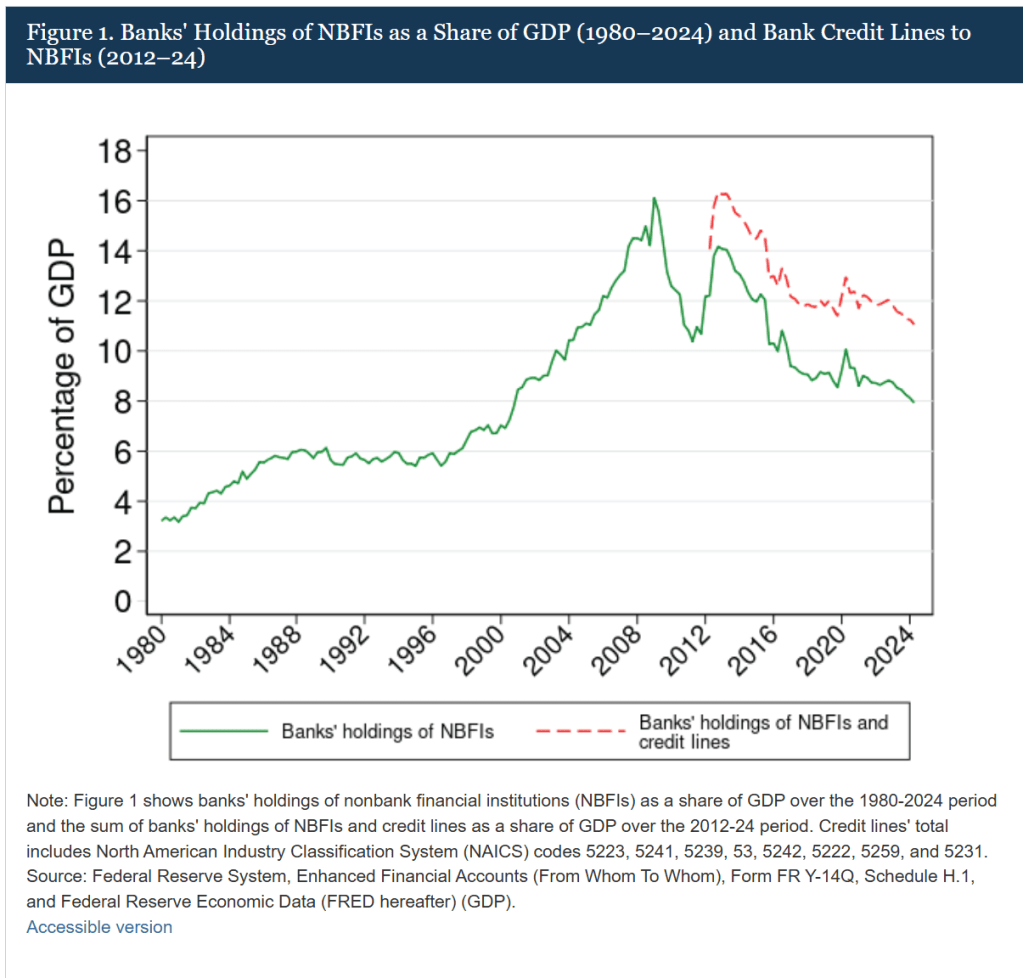

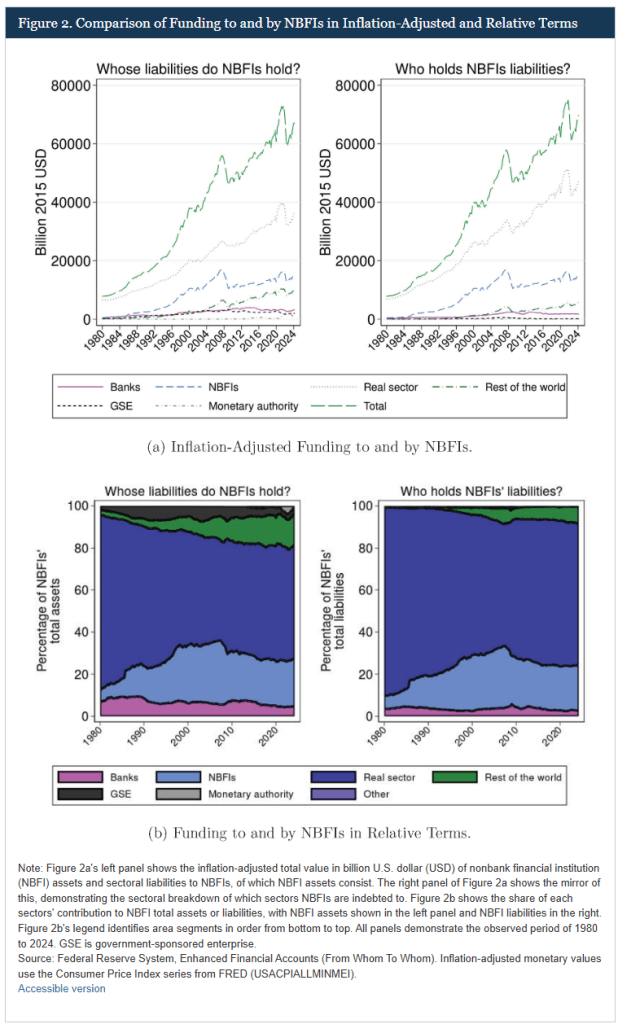

The growing importance of non-bank financial institutions (NBFI)s also caught the attention of the Federal Reserve in recent study (Duque Gabriel & Sterling, 2025).

Both types of institutions operate outside the traditional banking system but are often interconnected with banks, posing different levels of risk.

Essentially, all NDFIs are NBFIs, but not all NBFIs are NDFIs, as some NBFIs can take specific types of deposits.

Key Differences:

Definition & Scope:

NBFI (Non-Bank Financial Institution): A broad category including investment funds, insurance companies, pension funds, and finance companies. Some NBFIs, such as certain finance companies, might take limited deposits.

NDFI (Nondepository Financial Institution): Specifically refers to institutions that do not accept deposits from the public, such as mortgage lenders, private equity funds, and broker-dealers.

Deposit Taking: NDFIs strictly do not take deposits, whereas the broader NBFI category can include entities that might hold specialized or time deposits.

Funding Sources: NDFIs rely on alternative funding sources like equity, debt issuance, or bank credit lines.

Focus: NDFIs often focus heavily on lending and credit intermediation (e.g., mortgage companies), while NBFIs cover a wider scope including asset management, insurance, and brokerage services.

The Fed’s study also highlight gaps in understanding NDFI’s role

existing studies often focus on long-term averages rather than time-varying trends.

the literature rarely quantifies the size of credit lines relative to GDP, despite their systemic importance.

there is limited analysis of sectoral heterogeneity within the NBFI sector. By addressing these gaps, this study provides new insights into the evolving bank-NBFI nexus.

NBFIs have emerged as key intermediaries in the financial system, acting as both recipients and providers of funding within a complex network of interdependencies.

The Fed observes Ccedit lines to NBFIs have more than doubled since 2012, partially offsetting the decline in direct funding. This shift indicates a re-allocation of bank exposures away from direct holdings to contingent liabilities which are off-balance-sheet vulnerabilities.

NBFI credit lines is a significant systemic risk if drawn simultaneously during periods of stress.

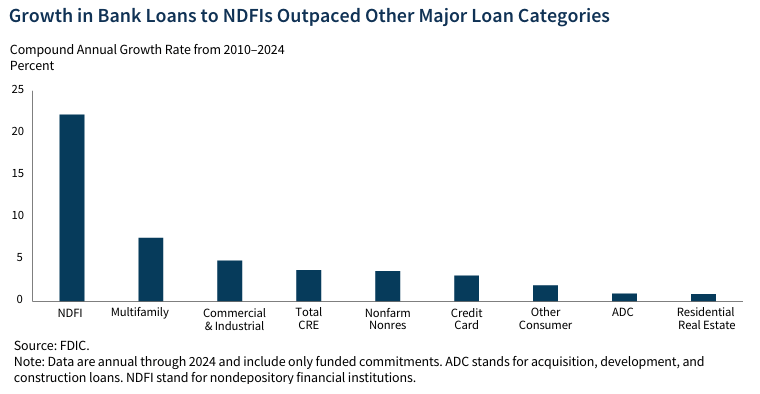

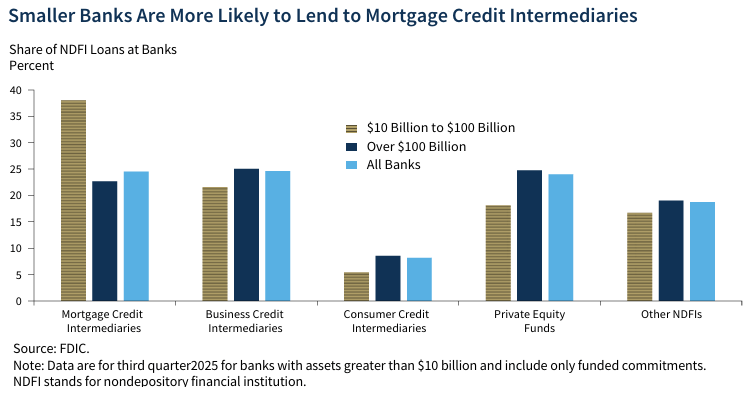

Focusing on NDFI segment in a recent paper published by FDIC (Federal Deposit Insurance Corporation, 2026), NDFI loan growth outpaces the next segment by 3x.

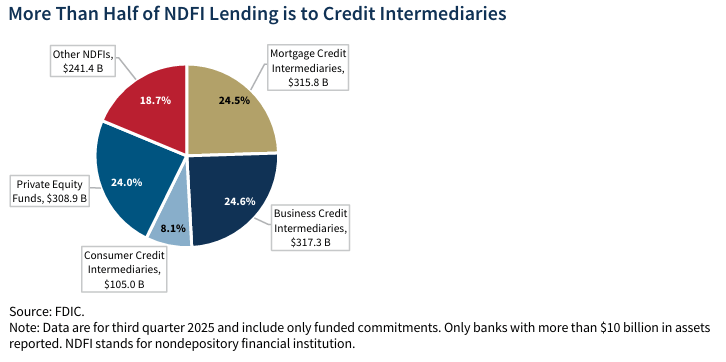

More than half of bank lending to NDFIs is to credit intermediaries, and about a quarter is to private equity funds.

Overall, while this lending offers revenue to banks, it creates a “transformed” risk structure where banks are indirect, highly exposed participants in the risks taken by nonbanks.

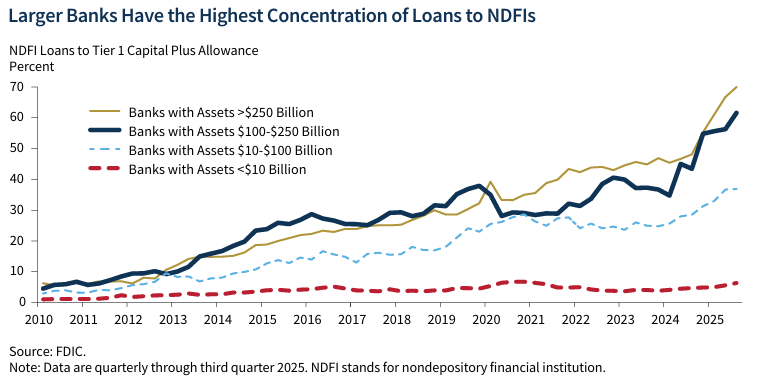

Large banks (>$100 billion) evenly distribute their exposure across private equity, business credit, and mortgage credit NDFI subcategories.

Regional banks (assets between $10 billion and $100 billion) see ~40% of NDFI lending in mortgage credit intermediation at almost 40 percent, while banks with assets greater than $100 billion.

The increased risk arises from three factors:

Rapid growth + risk concentration

By 2025, it reached roughly 10–13% of total bank loans

Large banks hold a disproportionate share of this exposure

Greater interconnectedness with “shadow banking”

NDFIs are less regulated and more opaque than banks

This creates complex links between regulated banks and less-regulated credit markets, which can transmit shocks

Structural vulnerabilities

Private credit (a major NDFI category) can involve:

higher leverage

illiquid assets

limited transparency

These features can amplify stress during downturns.

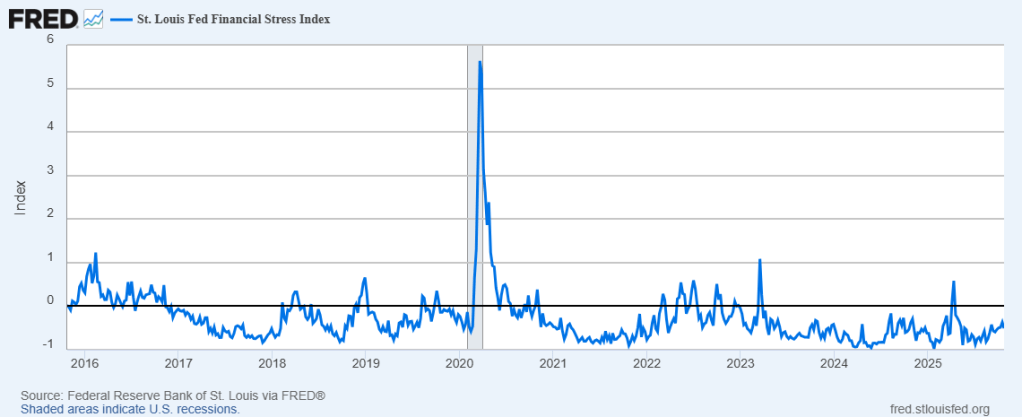

With the greatest global commodity shock dynamic propagating, it’s timely to examine the banking landscape at the water’s edge just before the tsunami sweeps in.

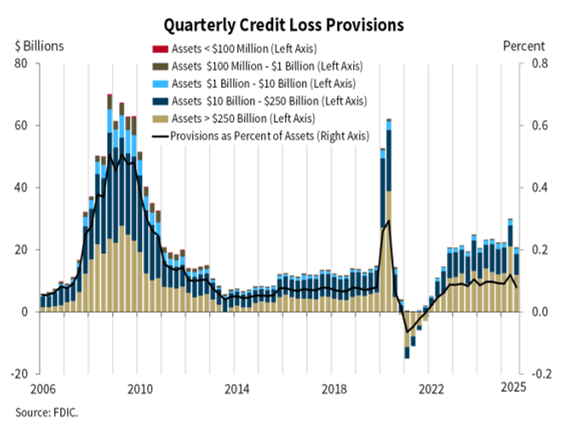

Per FDIC, the banking industry’s loss provision expense was $20.8 billion in the third quarter 2025, down $9.2 billion QoQ mostly due to Capital One’s acquisition of Discover Financial Services. Overall, loss provision decline would have been much less QoQ and YoY.

It’s a quiet time right now though things are starting to get interesting.

In the coming weeks and months, I’ll be following the Regionals through the Hormuz Shocks as they face their greatest challenge since the Great Financial Crisis.

Let’s set the stage.

From Great Financial Crisis to Covid

Credit shocks and reflation are a recurrent theme in the banking sector.

A decade later after the Great Financial Crisis and bank failures, the Covid macro shock was quickly followed by the failures of Silicon Valley Bank (SVB) and other regional banks (Regionals).

SVB failed in March 2023 primarily from interest rate risk on its securities portfolio — a held-to-maturity bond book that collapsed in market value as rates rose 525bps in 18 months and large uninsured depositors ran for the door.

SVB was not a one-time event. It cointegrates with the rising risk in the commercial real estate market (CRE), particularly the office sector collapse under remote/hybrid work policies introduced in the Covid era.

Like the subprime mortgages of the Great Financial, CRE credit stress and Regional bank risk are connected by the same root cause — the Fed’s aggressive rate cycle. The transmission mechanism is rising rates that simultaneously:

compress securities portfolios (SVB’s direct problem)

suppress transaction volume and refinancing activity in CRE markets

increase debt service costs on floating-rate CRE loans at maturity or reset, and

deflate property valuations as cap rates rise.

Banks that survived the securities mark-to-market problem — as many regionals did, notwithstanding Silicon Valley et al. — were then exposed to the second-order credit effect showing up in CRE charge-offs through 2023 and 2024.

The Covid crisis removed several hundred billion dollars from bank balance sheets which was replensihed by Fed liquidity. But interest rate increases to curb inflation quickly reduced balance sheets for several years.

The Covid-SVB period also coincides with the Regionals’ adoption of the Current Expected Credit Loss (CECL) provisioning standard that came out of the Great Financial Crisis. CECL’s pro-cyclicality shifted the credit loss allowances (ACL) ahead of credit shocks.

The question we should see answered in the upcoming commodity shock is whether CECL is up to the task for protecting the Regionals.

CRE Dynamics Post-Covid

Post-Covid, CRE returns lagged other major asset classes for three years, largely due to falling property prices, prompting investors to recalibrate allocation targets lower.

Valuations appear to have hit bottom in 2025, with tightening supply and accelerating demographic tailwinds positioning several sectors for renewed strength.

The drivers of the earlier decline — which bled into 2025 — are well understood:

Higher-for-longer interest rates. Interest rates remained above pre-pandemic levels, and stable assets carried borrowing costs significantly above historic lows, strengthening valuation discipline and leading to lower prices and reduced refinancing options

CRE sector bifurcation. Office continued losing value, particularly in California, New York, and Washington, while industrial and logistics activity remained stronger in markets like Texas and Florida.

Tariff and policy shocks. Increases in both tariffs and immigration restrictions raised costs for builders and developers throughout 2025.

Investor reallocation. Through the end of June 2025, property sales activity in the Americas was up 12% year over year, suggesting a recovery trajectory, while European markets dropped 15% due to bond rate shifts and trade policy.

By late 2025 into 2026, conditions were improving: debt costs eased, lenders reentered the market, and deal activity picked up — with Q3 2025 sales volume up more than 40% year over year.

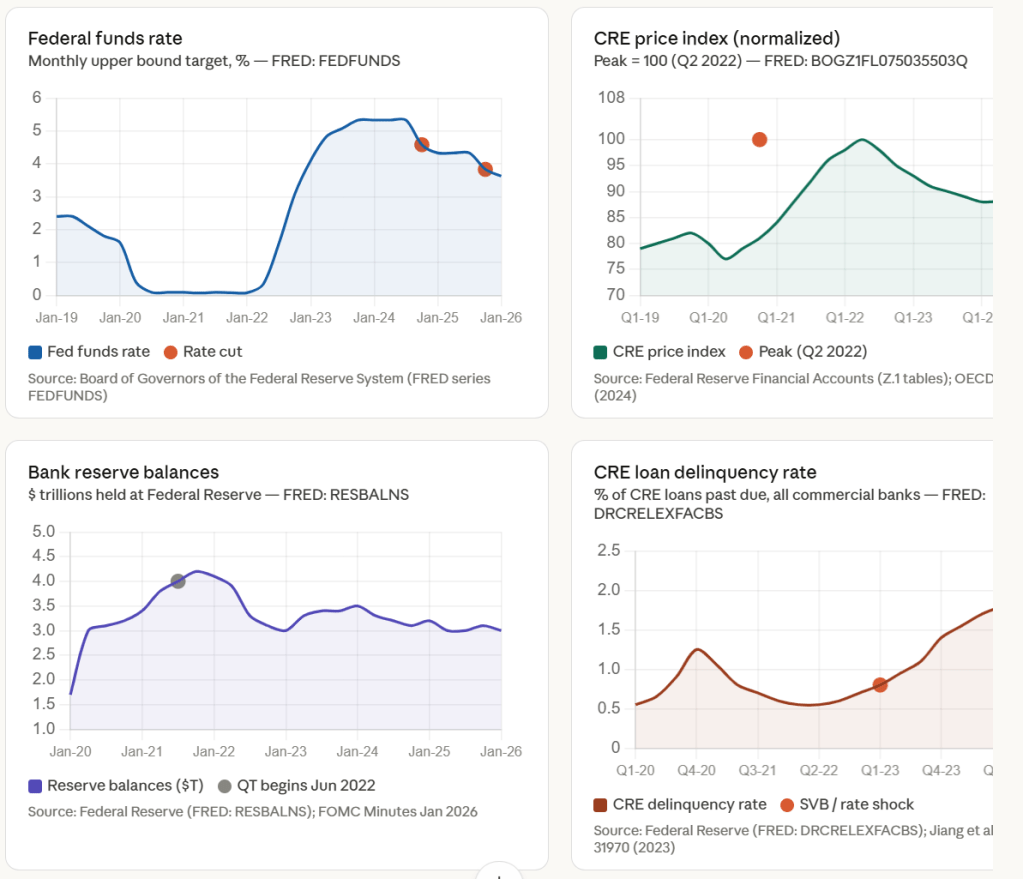

The short version: CRE price declines were largely a 2022–2024 story driven by rate hikes and office demand destruction, with 2025 being more of a trough/stabilization; and bank reserve rates have actually been cut, though reserve levels are being actively maintained at ample levels by the Fed buying short-term Treasuries.

Let’s review some key observations related to the CRE sector:

Claim 1 — CRE prices declined ~11% (US) from their mid-2022 peak, driven by rate hikes and structural demand shifts

The OECD Economics Department (Working Paper No. 1829, 2024) documents that commercial property prices in the United States declined significantly since their peak in mid-2022 — falling OECD 11% by late 2023 — driven by higher global interest rates and the adjustment to new demand patterns from teleworking and e-commerce.

Full citation: OECD Economics Dept. WP No. 1829 — “Commercial Real Estate Markets After the End of Low-for-Long: Risks and Policy Challenges” (December 2024). https://doi.org/10.1787/0f9ae118-en

Claim 2 — CRE’s ~25% share of average bank assets made it a systemic risk amplifier after rate hikes

Jiang, Matvos, Piskorski & Seru (NBER WP 31970, 2023) show that CRE loans represent about 25% of average bank assets, totaling $2.7 trillion, and that after property value declines from rising rates and the shift to hybrid work, 14% of all CRE loans and 44% of office loans were in negative equity — with a 10% default rate implying $80 billion in additional bank losses.

Full citation: Jiang, E.X., Matvos, G., Piskorski, T. & Seru, A. — “Monetary Tightening, Commercial Real Estate Distress, and US Bank Fragility” — NBER Working Paper 31970 (2023). https://doi.org/10.3386/w31970

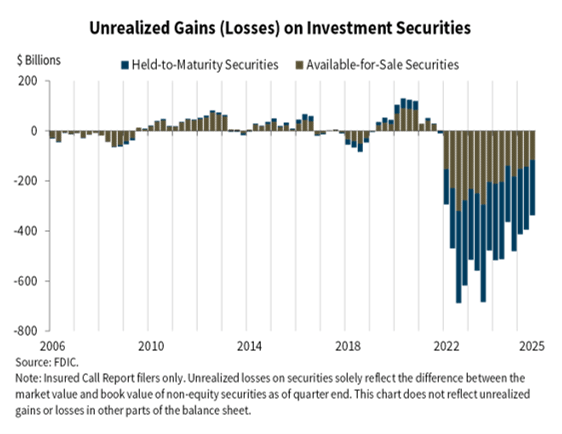

Claim 3 — Rate-driven mark-to-market losses of ~$2 trillion in bank assets amplified CRE fragility

Extending the same mark-to-market methodology to Q3 2023, the analysis finds that almost half of US banks (2,405 institutions) accounting for $11.6 trillion of aggregate assets had negative capitalization when all non-equity liabilities were taken at face value — with additional CRE losses eroding remaining capital buffers and increasing the risk of runs by uninsured depositors. NBER

Claim 4 — REIT credit lines create a systemic risk channel between CRE and bank balance sheets

An NBER working paper on shadow banking documents that commercial property prices dropped about 21% since the Federal Reserve started raising interest rates in March 2022, with the correction erasing the property price appreciation over the preceding two years, and shows REIT utilization rates on bank credit lines spike markedly during periods of market stress — making credit lines to REITs a potentially significant source of systemic risk for banks.

Claim 5 — Bank reserve balances held near $3T; the Fed restarted T-bill purchases to maintain “ample” reserves

At its December 2025 meeting, the Federal Reserve approved new purchases of Treasury bills and coupon bonds at up to $40 billion per month for reserve management purposes — not quantitative easing — designed to provide an ample supply of reserves, with this operation expected to run until April 2026.

Primary source: FOMC Implementation Note, December 2025; FOMC Minutes January 27–28, 2026 (Federal Reserve). FRED series: RESBALNS.

Claim 6 — Office sector structural vacancy represents a long-run headwind distinct from the cyclical rate shock

The OECD paper further documents that in the United States, smaller and regional banks sharply increased the share of CRE loans in total loans since the pandemic, while the largest banks did not — and with more than half of CRE loans backed by commercial non-farm non-residential properties, they are particularly exposed to strained conditions in the office and retail segments.

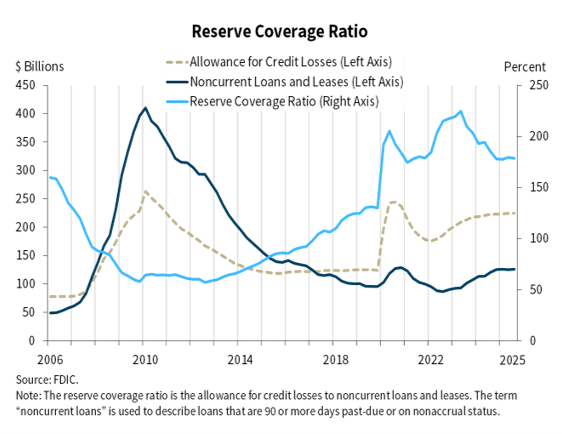

Reserving Trends

Here’s what FDIC reports. Note the widening gaps between large banks and community banks (with Regionals in between).

The story here has three distinct threads worth unpacking carefully.

Thread 1 — Coverage ratio: declining from a post-pandemic peak, but still elevated

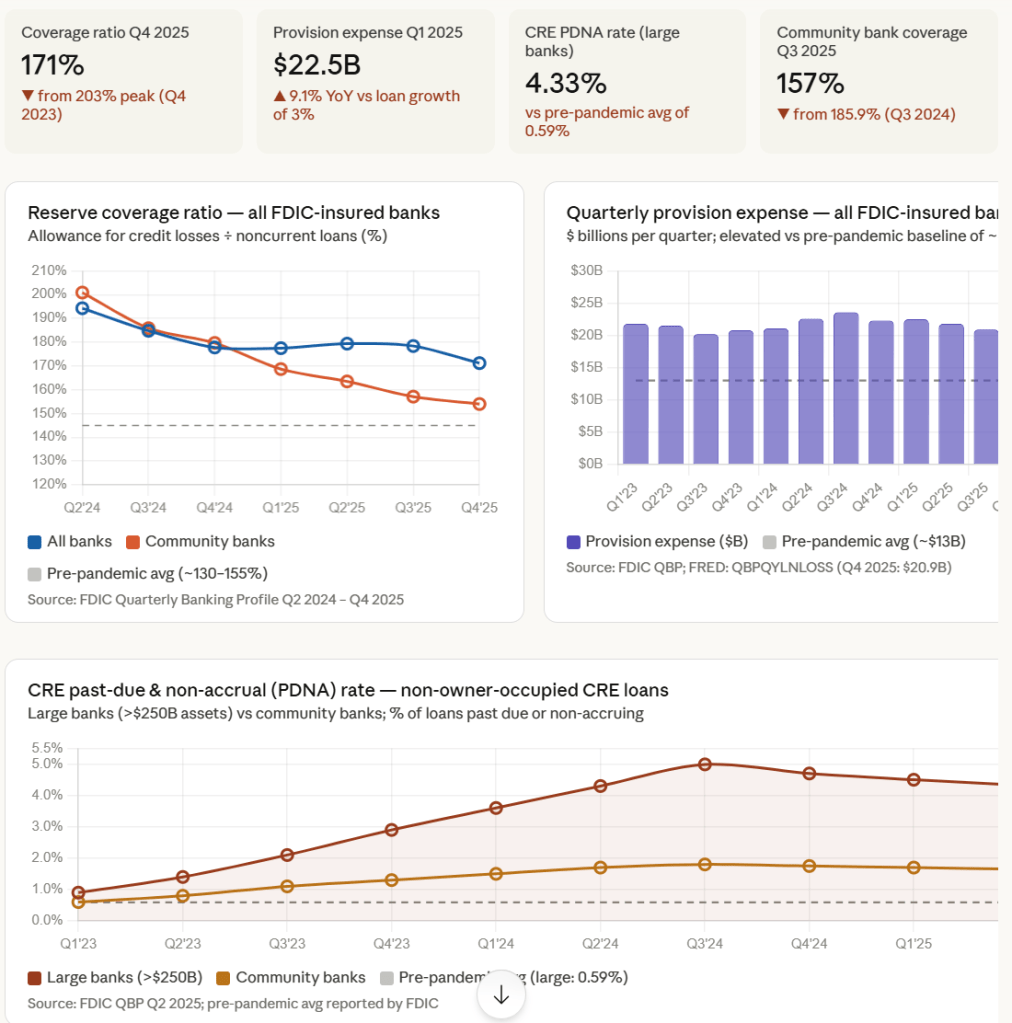

In 2023Q4, the industry coverage ratio — allowance for credit losses to noncurrent loans — was above 203%. Consistent declines have brought it to 177.5% as of Q1 2025. The most recent FDIC data show a further decline: in Q4 2025, the funded allowance for credit losses decreased slightly while noncurrent loan balances increased, resulting in a decrease in the reserve coverage ratio to 171.2%.

The mechanism driving this is not that banks are releasing reserves aggressively — it’s that noncurrent loan balances are growing faster than banks are building the allowance.

Community banks are feeling this more acutely: the reserve coverage ratio at community banks declined from 163.5% in Q2 2025 to 157.1% in Q3 2025 as the allowance for credit losses increased at a slower pace than noncurrent loan balances.

Thread 2 — Provision expense: persistently elevated but plateauing

The industry’s provision expense was $22.3 billion in Q4 2024, and provision expense has been higher than the pre-pandemic average for the past ten consecutive quarters.

In Q1 2025, provision expense was $22.5 billion — a modest increase of just $66.5 million from Q4 2024 — and the industry continued to build reserves, as provision expense exceeded net charge-offs by $1.2 billion for the quarter.

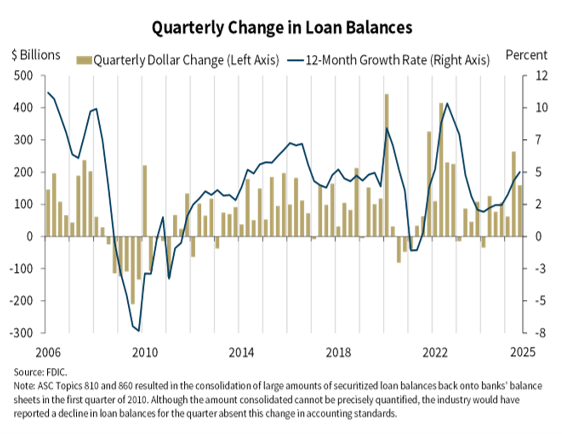

Quarterly provisions for loan losses and loan loss reserves were up 9.1% year-over-year even while loan growth was tepid at just 3%, signaling that banks are reserving defensively relative to their book growth.

Thread 3 — CRE-specific stress: large banks hit hardest in absolute terms, but better capitalized

Banks with greater than $250 billion in assets reported a non-owner-occupied CRE past-due and non-accrual rate of 4.33% in Q2 2025, down from the recent peak of 4.99% in Q3 2024 but well above the pre-pandemic average of 0.59%. However, these banks have lower concentrations of such loans relative to total assets and capital than smaller banks, mitigating overall risk.

Regionals? Not so good.

The macro overlay going into 2026

Trade uncertainties and elevated tariffs could reverse the current trajectory of declining credit-loss provisions, as community banks with concentrated CRE exposure remain particularly vulnerable, with provisions at some institutions already lagging behind rising credit losses.

The declining coverage ratio despite elevated provisions is a late-cycle signal — it means the denominator (stressed loans) is outrunning the numerator (reserves).

This dynamic concentrates at Regionals because they appear structurally central in networks precisely because they carry disproportionate CRE exposure relative to capital.

The Fed?

In our petrodollar monetary system, inflation follows oil prices.

Oil prices increased more than 40% in March 2026 before breaking out over $115.

Now faced with the Hormuz shock, the Fed is stuck in a delicate position: the FOMC voted 11-1 to hold rates at 3.5%–3.75% at the March 2026 meeting, balancing expectations of a pickup in inflation from higher energy prices against a soft but stable labor market.

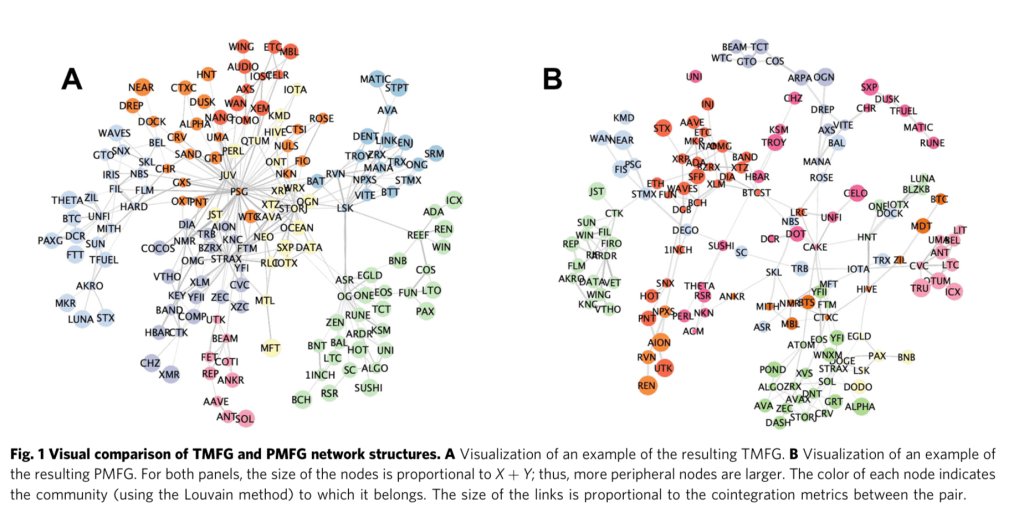

Diversification is the cornerstone of risk-adjusted portfolio construction. Yet, despite being a well-established principle in finance, diversification has been overlooked in pairs trading strategies, which often focus solely on selecting the most cointegrated pairs in isolation from the broader market structure and without accounting for their combined behavior within a portfolio. Here, we address this gap by introducing a network science framework to construct diversified pairs trading portfolios with minimal risk exposure, using cryptocurrencies as a case study. Our approach builds the structural network of assets based on their cointegration and then applies the Planar Maximally Filtered Graph and Triangular Maximally Filtered Graph to extract an effective market representation, which provides the essential market map for constructing diversified, risk-optimized portfolios. We show that selecting pairs that bridge communities significantly increases portfolio risk and reduces the average returns, as these pairs exhibit less stable long-term relationships because they are influenced by different market dynamics. Conversely, selecting peripheral pairs enhances the overall portfolio performance, consistently outperforming the conventional pairs trading approach of selecting the top cointegrated pairs. Finally, we conclude that incorporating the market network structure where pairs are embedded is essential for building diversified portfolios that mitigate hidden risks and cascading failures.

Contemporary risk management and regulatory policies seek to blunt the “too big to fail” hubris – a mindset said to be the ignition point for the Great Financial Crisis. To guard against increased risk from undue concentration, policies seek to diversify exposure by building connections.

Network science and statistical physics teaches cascading failures of all kinds can also arise from a “too connected to fail” dynamic.

In fact, be it a “too big to fail” network component, or a a “too connected to fail” community, cascading events can be two edges of the same sword.

In this paper, Grande & Borondo (2025) report selecting pairs that bridge ticker communities significantly increases portfolio risk and reduces the average returns. Such pairs exhibit less stable long-term relationships because they are influenced by different market dynamics.

Network-based approaches to portfolio diversification has been a rapidly growing part of the literature over the past decade. Network approaches reduce concentration risk (“too big to fail”), leading to more balanced and lower-risk portfolios.

In this paper, Grande & Borodono demonstrate incorporating the network structure rather than relying solely on pairwise co-movement metrics can guide the construction of more resilient pairs trading portfolios with a high concentration of peripheral pairs, thereby reducing exposure to cascading failures.

Market chatter seems to be rising reflecting growing fears credit market stress is ascending as Treasury yields fall and other economic warning signs are lighting up.

Manufacturing data and labor markets are retreating and the Fed is shutting down its QT policy ahead of possible rate cuts.

A bank liquidity crisis occurs when a bank lacks sufficient cash or other highly liquid assets to meet its short-term financial obligations, such as sudden large withdrawals by depositors. This can happen because banks often fund long-term assets like loans with short-term liabilities like deposits, creating a maturity mismatch. If many depositors withdraw their funds at once, a bank run can occur, and the bank may be forced to sell assets at a loss to cover the withdrawals, potentially leading to failure.

This dynamic is not restricted to banks. Long-dated capital projects in the energy sector can experience similar systemic risk where funding investments assumes demand is sufficient to recover project costs.

Following the Great Financial Crisis, network science literature has explored cascading dynamics among financial instituations. Among other things, the literature compares the stability of ring and complete network structures and shown completely connected systems tend to be be stable under small shocks but give way to instability under large shocks. In contrast, ring networks tend to be more resilient under large shocks while less so under smaller disruptions.

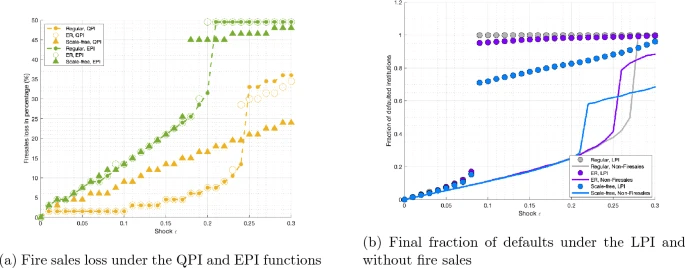

Fire sales and default contagion dynamics are the principal vectors are two of the main drivers of systemic risk in financial networks. Contagion reflects direct balance sheet exposures between institutions while the consequential fire sales reprices asset valuations thereby transmitting distress throughout the financial system.

Detering et al. (2020) develop a model explaining the joint effect of the two contagion channels and investigatea structures of financial systems that promote or hinder the spread of an initial local shock. They characterize resilient and non-resilient system structures by criteria that can be used by regulators to assess system stability. Further, they provide explicit capital requirements that secure the financial system against the joint impact of fire sales and default contagion.

Amini et al (2025) builds on Detering and presents a framework to better understand the joint impact of fire sales and default cascades on systemic risk in complex financial networks. They quantify quantify how price-mediated contagion across institutions with common asset holdings can worsen cascades of insolvencies in a heterogeneous financial network during a financial crisis. In the numerical studies we investigate the effect of heterogeneity in network structure and price impact function on the final size of the default cascade and fire sales loss.

System or network models typically segments into 3 categories:

Regular networks (without network heterogeneity)

Erdös-Rényi (ER) random networks with low heterogeneity when institutions have a degree (i.e., connections with other entities) close to the average degree

Scale-free networks (with high heterogeneity)

Amini modeled financial institutions in these ways and tested the resulting dynamics following a range of shocks.

With exponential price impacts, Aminim observed small shocks below the critical shock value for the scale-free network. Network heterogeneity does not have a significant influence on the fire sales loss.

For the quadratic price impact, small shocks trigger larger fire sale losses in the scale-free network.

Networks with higher heterogeneity has a smaller critical value for the shock. When the shock exceeds the critical value for the regular network , the regular network has the largest fire sales loss, while the scale-free network has the smallest loss. This dynamic arises because the scale-free network, has a larger proportion of institutions with low degrees (such as 1 and 2), which have a higher chance of surviving after a large shock. This makes the scale-free network more resilient to a large shock compared to the other two networks.

Aminimi observes their simulations highlight the importance of ensuring that a financial network can withstand large cascades under stress scenarios that put pressure on specific characteristics such as capital or liquidity reserves.

Presently, there is little evidence banking regulations capture these dyanmics.

____________________________________________

Amini, H., Cao, Z. & Sulem, A. Fire sales, default cascades and complex financial networks. Math Finan Econ19, 225–260 (2025). https://doi.org/10.1007/s11579-024-00381-z

Detering, N., Meyer-Brandis, T., Panagiotou, K. et al. An integrated model for fire sales and default contagion. Math Finan Econ15, 59–101 (2021). https://doi.org/10.1007/s11579-020-00273-y

This morning I wrote about the possible significance of an American pope. Of course, strictly speaking, Bergoglio was the first American pope. Strictly speaking—but perhaps metaphorically speaking as well. What seems beyond doubt is that he was the first Globalist pope.

Commenter Doug Hoover wrote today about events from 2013 which many may not recall, or the significance of which they may never have recognized:

America cut off their [Vatican] connection to SWIFT, freezing their ability to transfer or accept money.

America picked an American Pope.

What DH is referring to is NOT the recent death of Bergoglio and the election of Prevost/L14. He’s referring to the coerced removal of Ratzinger/B16 under cover of a “resignation” in 2013. I was still wondering whether to go “there” when commenter American Cardigan appeared to rise to the bait:

Haven’t seen evidence yet that the Vatican is reconnected to SWIFT.

It is clear that SWIFT intervened directly in Church affairs. Was there a blackmail coming from who knows where, (perhaps Soros, Clinton and Obama) through Swift, exercised on Benedict XVI?

“When a bank or territory is excluded from the System, as was the case with the Vatican in the days preceding Benedict XVI’s resignation in February 2013, all transactions were blocked. Without waiting for the election of Pope Bergoglio, the Swift system was unlocked upon the announcement of Benedict XVI’s resignation.”

In point of fact, Vatican City was reconnected to Swift before Bergoglio was elected. That B16 was removed seems beyond doubt. The perps have never taken public credit, so the exact origin of the decision remains murky. Presumably America at least acquiesced in the coup, but it’s conceivable that it was actually instigated by non-American forces and coordinated with America:

The great globalist powers are in a hurry and Ratzinger was a clear obstacle, a slowdown on their lightning-fast trajectory.”

…

And immediately after his [B16’s] passing [i.e., resignation], SWIFT unblocks Vatican transactions, reopens ATMs, and brings the IOR [one of two Vatican banks] back to the honor of the world.

They didn’t wait for Bergoglio to be elected; the expulsion of the “white terrorist” was enough for him.

In the good and unattainable salons between Wall Street and Washington and London, they already knew that the conclave would give the throne to a modernist, to someone they could trust.

How come? Had the SWIFT sanction been coordinated with the “conspirators” in purple who, led by [Jesuit “black” terrorist] Carlo Maria Martini (a cardinal who asked for euthanasia for himself, it should be remembered…) had marked Bergoglio as their candidate for years already?

Was there an agreement between the conspirators with a strong external power, to which they are close in ideology?

But it seems to understand that Ratzinger’s resignation is – he was forced to step down from the throne of Peter under construction.

So, Bergoglio was—perhaps in more than one sense—the first American pope. More to the point, he was probably the first inarguably non-Catholic pope. Regular readers will have seen me use that term fairly regularly. I do use it in all seriousness. Anyone who cares to search the archives here will find that I have questioned the faith of both Wojtyła and Ratzinger on philosophical grounds, but I also recognize that questions of this sort are rarely unambiguous. The Neomodernist takeover—fronted by Bergoglio—does appear to be one of those unambiguous events, allowing for the Neomodernist (and Globalist) desire to continue using the visible institutions of the Catholic Church for their own purposes.

What led to the Globalist Coup—or Regime Change, if you prefer? It could have been that they simply judged that the time had come to remove this hated obstacle, but Traditionalists would argue that it was specifically the wild success of Ratzinger’s 2007 motu proprioSummorum Pontificum that enraged the demonic forces of the Globalists and led them to take action. Technically, Summorum Pontificum allowed for the widespread use of the traditional Roman liturgy, what is often referred to as the Tridentine Mass—which is the codification of the Roman liturgy that reached its first definitive form under Gregory I in around 590. The core of the Roman liturgy is its “canon”, which has roots that go back far earlier than Gregory. It is the earliest documentable “eucharistic prayer”. The point is that, until the post Vatican 2 revolution, the Roman Canon was the only eucharistic prayer known to the Catholic Church. The Roman Canon embodies the core of the Catholic faith in its worship. Post Vatican 2 the Roman Canon was—for practical purposes—supplanted by a variety of Neomodernist (“Teilhardian”) tinged “prayers”. Don’t take my word for it—Ratzinger himself referred to the “cosmic” aspects of the New Order. And so Traditionalists argue that this threatened widespread return to full Christian faith and re-evangelization in the West aroused the demonic forces of Globalism to a fury. Do you see now why so much importance has been attached to Prevost’s documentable use of the traditional Roman liturgy?

All of that lends urgency to the questions surrounding the most recent conclave. It appears that the most radical Neomodernist forces were routed. Exactly where Prevost fits in isn’t entirely clear. He rose rapidly under Bergoglio and was complicit in some of the worst excesses regarding the appointment and removal of bishops (itself a troubling matter—as if bishops were little more than functionaries or vicars of the “pope”). On the other hand, there are documentably hopeful signs that Prevost will take the faith he professes seriously. Look, I’m not making some sort of unqualified endorsement of Prevost, but I am suggesting that God can work through imperfect human beings, flawed individuals.

Inevitably, this leads to Trump and his money—his reported $14 million donation to “the Vatican”. We know that Trump’s first election win in 2016—three years after Ratzinger’s removal—frustrated Globalist plans. While MAGA shares some features with Globalism, the appeal to normal people—who could be influenced by religious faith, as opposed to demonic ideology—posed an existential threat to the Globalist establishment. Trump’s predilection to deal making—especially with Russia—was viewed, rightly or wrongly, as a setback for the Globalist agenda. We saw how that frustration played out in the removal of Trump in 2020, but the debacle of the four Zhou years forced the Globalists to reconcile to a Trump return.

As I’ve noted several times, a little remarked feature of Trump’s 2024 campaign was his persistent outreach not just to Catholics but to the most traditionalist strains of Catholicism. Trump’s repeated use of traditional Catholic iconography during the campaign was unparalleled in American politics, yet passed with next to no comment. Who was behind this? One thing seems certain—Trump himself could hardly have formulated that outreach. This wasn’t coincidence or a whimsical feature of the campaign. And now we learn of Trump’s prominence in Rome—including his reported cash infusion as well as the influence of Trump connected cardinals like Dolan in the election itself.

What does it all mean? I can’t tell you. It could be that Trump—are some in his circle—have contrived to engineer a liberation of the Catholic Church from its “Babylonian Captivity” under the Neomodernists. Certainly this could work to Trump’s political advantage, both at home as well as in his dealings with Europe, where traditionalist Catholics are one among the few reliable opponents of the Globalist order. If any of this is the case, we should expect L14 to move fairly quickly. Will any of these developments have a positive impact on the notoriously mercurial and emotional Trump, who is highly impressionable when it comes to imagery and symbolism? We can hope.

If you had a bad week in markets since “Liberation Day”, here’s your “Daisy”.

Stephen Miran.

American economist and current chair of the Council of Economic Advisers since March 2025. (Sorry Mark, you’re STILL a “bridesmaid” and a hilarious talking head for a very sketchy operation — LOL)

Let’s take some liberties with what Stephen actually said, and paraphrase Miran’s key points:

“Listen up, you Freeloading Bozos – we do it all for you. We give and we give and we give. But there ain’t no more to give.”

“We provide you ‘serious muscle’ – a security umbrella creating the greatest era of peace mankind has ever know. Our dollar, Treasury securities, and reserve assets underwrite the global trading and financial system which made you (and our DC War Party politicos) richer than you really should be.”

“As much as we love you all (COUGH), this party is not cheap or free for us. You’re pigging out and your damn trade deficits are unsustainable.”

“Your pig-out trashed our manufacturing sector. Our working-class families and their communities (beloved voters that they are) are getting pillaged.”

“Our voters have been paying for your peace and prosperity”.

“The USDs and Fed policies the world loves kept everyone’s borrowing rates insanely low making the rich richer and the poor poorer. But things are getting out of hand – notably in currency markets.”

“The Don says the party’s over.”

“So, we’re going to make some changes with the PRC/PBOC in mind.”

“Want to continue enjoying our USDs and DOD? Time to pay up. We can do it the easy way or the hard way – but regardless what you decide, things are going to change.”

“Here’s the deal — you can accept tariffs on your exports to the United States without retaliation. That’s the easy way.”

“Or, you can stop unfair and harmful trading practices by opening your markets and buying more from America — a lot more. That’s also the easy way.”

“Or, you can start paying your own way defending your pathetic little fiefdoms – also part of the easy way.”

“Or, you can build factories here in the USA. Easiest of all.”

“Or, Venmo the dough directly to us. We can make that work if you prefer.”

“We’re still here for you freeloading cherry pickers as you work the numbers. Our trading systems, too”.

“But, however you decide to pay, it’s time to pay. And, one way or the other you will pay.”

“Prefer retaliating? Don’t recommend it but, hey, I get it – there are some hotheads out there. OK, we can do it that way, too Remember who supplies your weapons, ammo, spare parts and intelligence to your defense. How long do you think you can run on inventory. Our Carrier Strike Groups, and advance-deployed Army, Marine Corps, and Air Force can pack up and leave as quick as we dumped Afghanistan. And remember who runs SWIFT.”

“As Treasury Secretary John Connolly famously said in 1971 when the US suspended gold convertibility, and threw an extra 10% across-the-board tariff on y’all, the dollar is ‘our currency, but it’s your problem‘”.

Last night I had the privilege of being included in a Zoom call with Steve Bannon, former investment banker and media executive, host of the “War Room” show and chief political strategist during the first seven months of Donald Trump‘s first term in office. Much of what Bannon presented wasn’t surprising, but what seemed significant was that he confirmed that Trump and his team will go on the offensive from day one in office. “The days of thunder begin on Monday,” he said, and the world will not be the same again. Bannon wasn’t talking about Trump going on the offensive against the Chinese, Iranians or the Russians. Trump and his team are preparing to take on the “they.”

“They,” in Bannon’s words, are the people who control the world’s most powerful empire and, elections or no elections, democracy or no democracy, they will not voluntarily relinquish their privileges and the control over their empire: there will be a fight. In a few recent podcasts, I discussed what this likely implies, simply on the basis of what the nature of this power struggle entail

Namely, taking on the imperial cabal is a fight to the death. “They,” are vicious, unscrupulous and extremely vindictive. If Trump and his team falter in this struggle, the cabal will not content themselves with merely defeating Trump politically. I believe they would not relent until they entirely destroyed him, his fortune, his collaborators and his family.

The price of defying the Empire

When the United States declared independence from the British Empire, the signatories of the Declaration of Independence were not just a bunch of belligerent rebels with nothing to lose. In many ways, they were similar to the people flanking Donald Trump today. They were all educated men of means and privileged members of society.

They all defied the Empire and pledged their lives

Of the 56 signatories, twenty four were lawyers and jurists; eleven were wealthy merchants; nine were farmers and large plantation owners. In signing the Declaration of Independence they provoked the wrath of the empire, knowing for sure that if they were captured their penalty would be death. Five of them were in fact captured by the British as traitors and tortured before they died. Twelve had their homes ransacked and burned. Two lost their sons and another two had their sons captured and imprisoned.

Nine of the 56 fought and died from wounds or hardships in the revolutionary war. Carter Braxton, a wealthy planter and trader saw all his ships sunk by the British Navy. To pay his debts he was forced to sell his home and his properties. He died a poor man. To avoid capture, Thomas McKeam had to move his family around the country almost constantly. He served in Congress without pay and his family was kept in hiding. Ultimately, his possessions were taken from him and he too, died in poverty. The home and properties of Francis Lewis were destroyed and his wife was jailed. She died within a few months.

The properties of Ellery, Clymer, Hall, Walton, Gwinnett, Heyward, Ruttledge, and Middleton were vandalized and destroyed by British troops or their proxy terror squads. British General Cornwallis took over Thomas Nelson‘s home for his headquarters. It was destroyed during the battle of Yorktown and Nelson died bankrupt. John Hart had to flee his homestead after his fields and gristmill were destroyed. For over a year he hid, living in forests and caves. When he returned home, his wife was dead and their 13 children all vanished. The grief and distress killed him within a few weeks. Norris and Livingston suffered similar fates.

When the imperial cabal decided to break up the United States, which precipitated the Civil War, they were confronted by President Abraham Lincoln. In 1863, Russian Czar Alexander II came to Lincoln’s aid by dispatching his Baltic fleet to New York and his Pacific fleet to San Francisco. The move blocked the Empire’s intervention on the side of the Confederation, which was planned by the British with the support of France and the Vatican. The U.S. – Russian alliance ultimately prevailed and the United States was preserved.

Alliance between Russia and the USA saved the union from the British Empire. Note how Lincoln is portrayed as a troglodyte in London.

But to exact their revenge, the cabal dispatched assassins. Abraham Lincoln was killed in 1865, shortly after the end of the Civil War, and Alexander II was assassinated in St. Petersburg in 1881. In 1917 the whole family of the Czar Nicholas II was killed by the Bolsheviks on the orders of the New York banker Jacob Schiff. Arguably, the low life expectancy among the Kennedy family men is also likely due to their propensity to irritate the imperial cabal.

I do believe that Donald Trump and at least some of the people around him are probably well aware of all this and understand the stakes in the struggle they took on. During our call last night Steve Bannon confirmed that this is indeed the case. The nature of this conflict dictates that “they” can’t be left standing and whoever comes into the White House after four years of Trump will be tasked with continuing the struggle until the imperial cabal is entirely uprooted and disenfranchised.

The clash is global and it’s between two systems of governance

Just like in the Middle East, Ukraine and elsewhere, what we’ll witness is another front in the struggle between two systems of governance. In that sense, the geopolitical conflicts around the world will likely be subordinated to the civil war shaping up in the United States, which could prove the central battle in the whole conflict. That civil war might not resemble the civil wars of the past with large armies fighting one another in fields and insurrections in cities. Instead, we’ll likely see chaos, sabotage, assassinations and terrorism in the U.S. – but also in Europe and the U.K.

One of the participants in yesterday’s call was also Christine Anderson, member of the German AfD party and the European Parliament. She reported that the authorities in Germany, as in France, UK and other European nations, are “berserk,” and that the Trump election has pushed them over the edge of overt authoritarianism which they no longer even bother to conceal.

As a result, there’s open talk about cancelling the upcoming 23 February elections in Germany, and more aggressive censorship of social media. Elon Musk‘s recent interview of AfD leader Alice Weidel only added to the hysteria and now German authorities want to prosecute Musk as they construed his interview of Weidel as an illegal campaign donation.

Participants from the UK reported perhaps the most distressing news, agreeing that the situation in the nation is simply awful, that they do not even recognize their country. One doctor said that he sees that people are increasingly giving up and many are “losing the will to live.” One concrete piece of news, which was confirmed to be true, is that for some months now, elected politicians no longer appoint judges in Britain. I did not understand who does appoint them as our call ran overtime before I had the chance to ask, but I’m sure it’s probably some really nice people.

Another distressing development in the UK is the upcoming Climate and Nature Bill which, if passed, will legally enshrine Britain’s commitment to net zero policies, which could prove devastating to its economy including the energy market, farming and industrial output. I elaborated what net zero entails for the British economy in this article.

You could get away with a 40 billion trade deficit if your currency was the world’s reserve currency, but the British pound is not.

In all, it seems that the days of thunder begin next week. These are the times to be brave. Maybe Trump and the people around him just want a bigger slice of the pie and there’s nothing more to it than that. But perhaps the struggle is bigger than that. Steve Bannon recently spent four months in prison – not a country club, as he said, but a real prison. Trump had two, perhaps more attempts at his life. The struggle is very real.

However, Trump’s adversaries are in a panic, according to Bannon. Most of them really didn’t think Trump would win the elections last November. Bannon said that Trump is a “blunt force instrument,” and that the cabal sustained a “blunt force trauma.” Hundreds, perhaps thousands of their minions, including Dr. Anthony Fauci, are jockeying to obtain pardons from the Biden team, even on a pre-emptive basis. Well, we’ll find out – it won’t be boring.

Late yesterday afternoon Judge Nap featured a session with Jeffrey Sachs that held out tantalizing possibilities for those of us—and who isn’t?—who are trying to come to grips with what Trump is up to these days with his many and provocative public statements. This followed mere hours after my post expressing deep disquiet regarding Trump’s “hellish” threats directed at the Middle East.

The session begins with a video of Professor Sachs speaking—he’s at the Cambridge University Student Union and he’s talking about the US Deep State in historical perspective. That perspective is to shed light on current events. I’ve done a transcript of that portion, but I’ll give away the punch line—this video was linked at Truth Social by none other than Donald J. Trump. Now, we already know that Trump in the past was an outspoken critic of our fraudulent forever wars, but I think it goes without saying that he wouldn’t lightly draw attention to what Sachs is saying—all of what Sachs is saying—without acquainting himself with the contents. So:

Sachs: It’s a game. This is the Deep State and they have their wars, and every war has been phony. Some wars the American people are basically never told about–for example the war in Syria. You may actually hear from grownup reporters–who are lying through their teeth or ignorant beyond imagining–that, ‘Oh, the war in Syria, yes, Russia intervened in Syria.’ Well, do you know that Obama tasked the CIA to overthrow the Syrian government, starting 4 years before Russia intervened? What kind of nonsense is that? And how many times did the New York Times report on Operation Timber Sycamore, which was the presidential order to the CIA to overthrow Bashar al-Assad? Three times in 10 years! This is not democracy. This is a game, and it’s a game of narrative.

Why did the US invade Iraq in 2003? Well, first all it was completely phony pretenses. It wasn’t, ‘Oh, we were so wrong–they didn’t have weapons of mass destruction [after all].’They actually did focus groups in the fall of 2002 to find out what would sell that war to the American people.Abe Shulsky–if you want to know the name of the PR genius. They did focus groups on the war! They wanted the war all the time, they [just] had to figure out how to sell the war to the American people, how to scare the shit out of the American people. It was a phony war. Where did that war come from? You know what? It’s quite surprising. That war came from Netanyahu, actually. You know that? It’s weird, and the way it is, is that Netanyahu had, from 1995 onward, the theory that the only way we’re going to get rid of Hamas and Hezbollah is by toppling the governments that support them–that’s Iraq, Syria, and Iran. The guy’s nothing if not obsessive. He’s still trying to get us to fight Iran–this day, this week. He’s a deep, dark, son of a bitch–sorry to tell you–cuz he’s gotten us into endless wars, and because of the power of all of this in US politics he’s gotten his way. But that war was totally phony. So what is this democracy versus dictatorship? Come on–these are not even sensible terms!

Judge: That of course was Professor Jeffrey Sachs at the Cambridge Student Union. Why do I run that? Because that was posted, a reference to it was posted, on Truth Social by the President Elect of the United States [Donald J. Trump].

Now that—linking to Sachs calling Netanyahu a “deep, dark, son of a bitch”—is remarkable even by Trumpian standards. I can’t actually think of any reason why Trump would do that other than that he really believes it. Sachs himself argues that that isn’t the action of a guy who wants to get America into another crazy war. The big question is this: How far does this reveal the inner Trump? Sachs is clearly on solid ground when he argues, in the discussion that follows, that Trump—in the portion of his remarks that were clearly made for the benefit of the Russian leadership—is now openly recognizing that Russia has legitimate security interests in their “near abroad”, and explicitly so in Ukraine. Doug Macgregor must certainly be smiling today.

How far we can extrapolate to the Middle East is another matter, and yet …

Trump’s link to Sachs’ remarks either directly preceded or followed hard on the heels of Trump’s statements about bringing “hell” to the Middle East. Can we say that Trump was signalling that we should take his rhetoric with a grain of salt? But a PR savvy guy like Trump has to understand the dangers of positioning himself out on a limb. By the same token—on the other hand—adopting by link Sachs’ characterization of Netanyahu as a “deep, dark, son of a bitch” who is ultimately responsible for instigating most of our forever wars certainly places Trump out on a limb with regard to the The Israel Lobby.

As so often with Trump, we’ll need to wait and see. Nevertheless, this is definitely grist for the speculative mill.

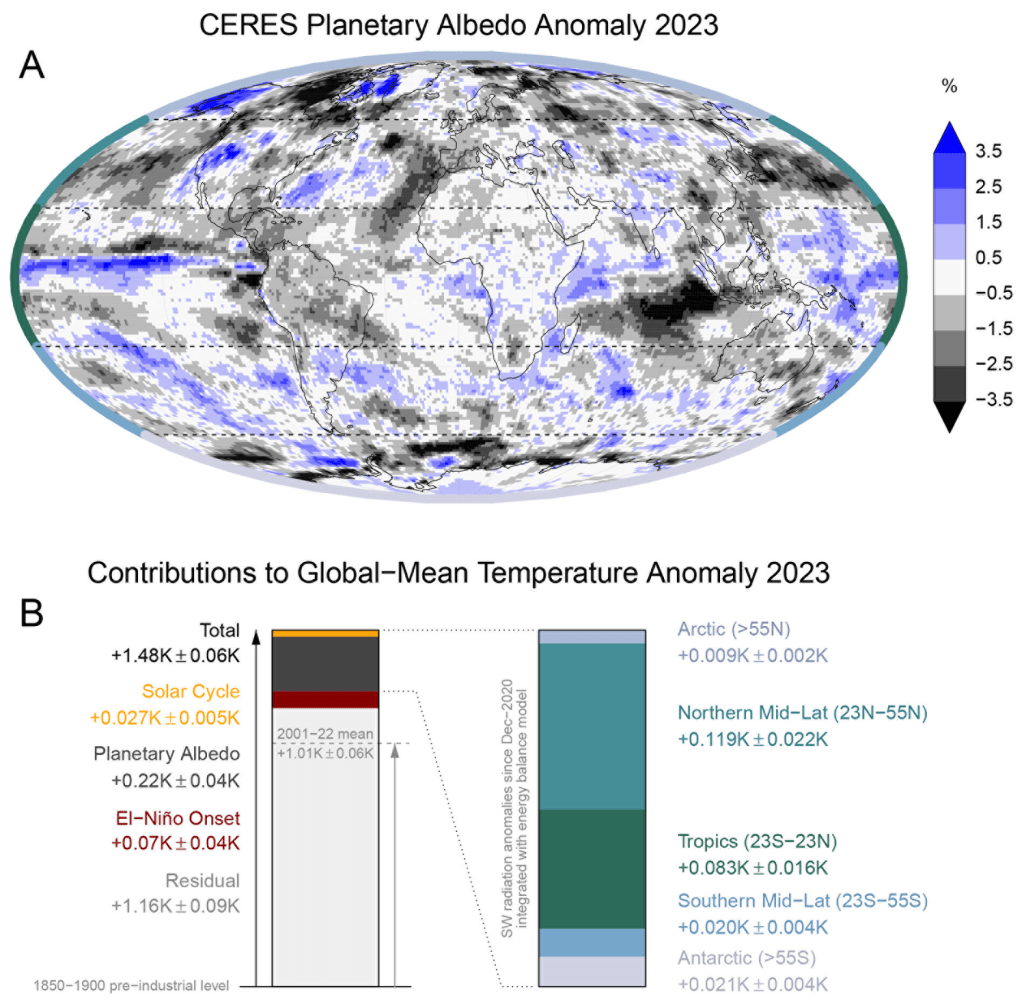

Citation: Helge F. Goessling et al., Recent global temperature surge intensified by record-low planetary albedo. Science 0, eadq7280DOI:10.1126/science.adq7280

Abstract:

In 2023, the global mean temperature soared to almost 1.5K above the pre-industrial level, surpassing the previous record by about 0.17K. Previous best-guess estimates of known drivers including anthropogenic warming and the El Niño onset fall short by about 0.2K in explaining the temperature rise. Utilizing satellite and reanalysis data, we identify a record-low planetary albedo as the primary factor bridging this gap. The decline is apparently caused largely by a reduced low-cloud cover in the northern mid-latitudes and tropics, in continuation of a multi-annual trend. Further exploring the low-cloud trend and understanding how much of it is due to internal variability, reduced aerosol concentrations, or a possibly emerging low-cloud feedback will be crucial for assessing the current and expected future warming.