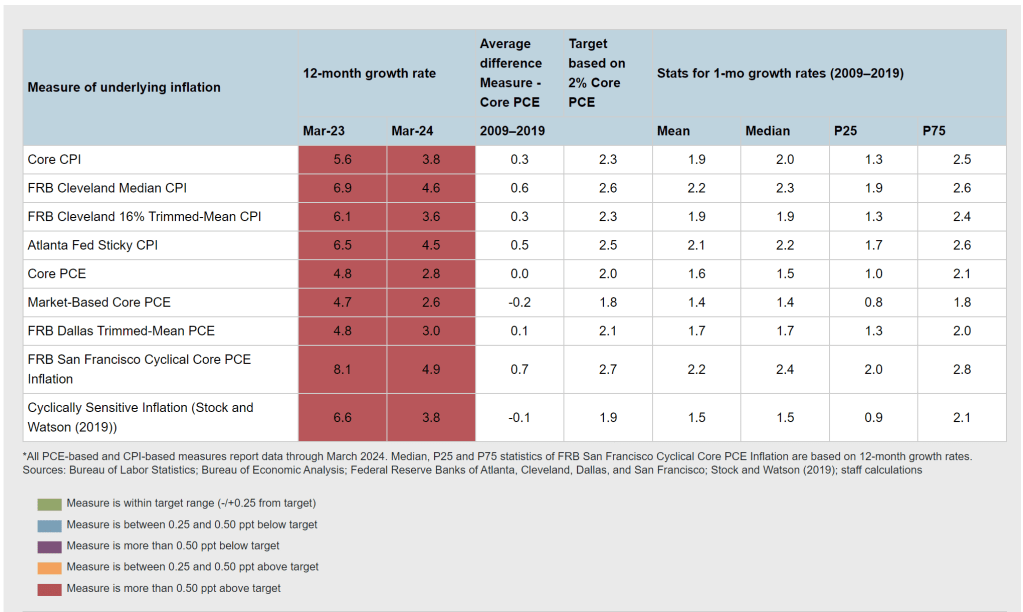

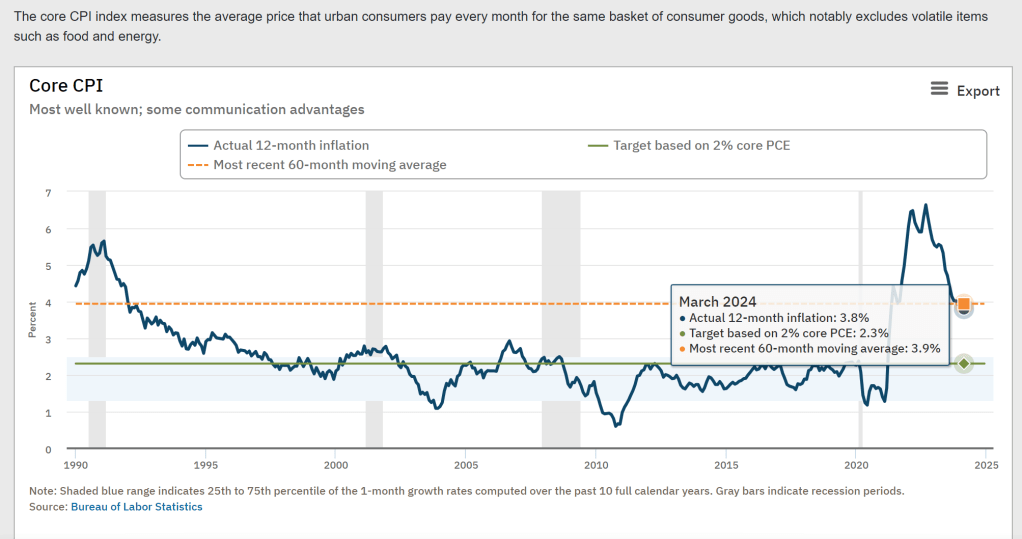

Atlanta Fed: https://www.atlantafed.org/research/inflationproject/underlying-inflation-dashboard?

Hard to like a Kennedy. If you have ever been in the proximity of a random Kennedy family member, the gut reaction is unforgettable as I’ve had the misfortune of experiencing over the years on several occasions.

Worse, when you throw in a Soros-supporting oligarch as his “Kamela”.

Don’t get me wrong, RFK Jr. has his points. For one thing, the reptiles in the Family have practically disowned him.

Enemy of my enemy, …., well, you get the drift.

Still, as an intellectual exercise, it’s worth weighing how this pair can play the 2024 election.

Conceivably, a hung election goes to the House where … the lunatic fascists in the Democrat faction of the Uniparty will crush RFK Jr.

Well, that said, here’s David Stockman doing the honors of Kennedy 2.0: https://davidstockman.substack.com/p/the-nicole-shanahan-announcement?publication_id=1246428&post_id=143036083

********

When John F. Kennedy chose his running mate in 1960, he was not in the ideological check-the-box business. He was in the race to win, and to do that he needed the 26 electoral votes of Texas and to retain as many of the 101 electoral votes in the rest of the historic “Solid South” as possible.

Needless to say, leading Democrat contenders for the VP nod like Senators Hubert Humphrey and Henry Jackson or Minnesota Governor Orville Freeman checked the liberal boxes with flying colors. But when it came to the electoral votes of Texas or Alabama, not so much.

As it happened, JFK choose Senate Leader Lyndon Johnson. The latter delivered his home state by hook and/or crook, and also helped JFK salvage much of the Solid South before it disappeared into today’s red state wall in 1968 and after. Still, Nixon won 43 electoral votes there, while independent Harry Byrd siphoned off another 15 votes in Alabama, Mississippi and Oklahoma.

That left JFK with just 43 electoral votes in the Solid South and an overall margin in the Electoral College that was therefore far closer than suggested by his 303 to 219 win over Nixon. In fact, had Texas gone to Nixon and another 9 electoral votes in the Solid South shifted to Nixon or Byrd, JFK would have been deprived of an Electoral College majority (269 votes), thereby likely forcing the election into the US House of Representatives for the first time since 1824.

Needless to say, in choosing his running mate RFK was in the same position his uncle had been in 64 years ago. He didn’t need to check any ideological boxes because his core platform was already crystal clear: Bobby Kennedy is the anti-Uniparty candidate who can liberate America’s constitutional democracy from the crony capitalist grip of the War Party, Wall Street, Big Pharma, Silicon Valley and the rest of the beltway bandits—all of whom have prospered mightily during decades of Forever Wars and unspeakable financial windfalls to the 1%, even as main street America has withered on the economic vine.

Yet while his platform is clear and solid, his route to victory as a third-party independent is murky, at best. And also, is far more complex than the strategy of salvaging the Solid South employed by JFK.

To wit, we see no practical route to an RFK victory via a standard majority of the votes in the Electoral College. But unlike 1960, the prospect of a hung jury in the Electoral College, and therefore election of the next President in the U.S. House of Representatives, is considerable, indeed.

Accordingly, RFK’s path to the White House needs to encompass three crucial objectives:

As it happens, we are not sure which policy boxes Nicole Shanahan checks, but we do think she might well be a brilliant choice when it comes to the three-step election strategy enumerated above. That’s because she’s young, idealistic, tech-savvy, a living embodiment of the American Dream, the spawn of a hard-scrabble immigrant family and a refugee from the Washington-based Democratic party that has lost its way.

Yes, we are not especially enamored with her bit about purifying the soil or the whackadoo district attorney in Los Angeles that she apparently supported under the banner of justice reform. But libertarians need remember that America’s jails are overflowing with victims of Washington’s idiotic War on Drugs and a whole array of other Nanny State crimes including crossing the border illegally because the Washington-prescribed legal quota for work permits for unskilled labor is laughably tiny (@ 4,500 per year).

So an ample and orderly Guest Worker program, justice reform and clearing out the jails of millions of nonviolent perpetrators of victimless crime is the very essence of shrinking Big Government and getting the state out of our lives. And that mission especially extends to the Deep State’s assault on free speech and suppression of dissent from UniParty orthodoxies.

There is no doubt that RFK is on the right side of all of these issues and that he will battle the real threat to “law and order” in America, which is the Democrat-driven weaponization of the machinery of justice and the horrible over-reach of the FBI, CIA and other Deep State institutions. And as far as we can tell, Nicole Shanahan is fully on board with that crucial agenda.

Still, RFK has to win the election first, and a re-run of the 2020 election results with just two changes tells you why his VP pick might help make that happen. These include—

The result would have been 264 electoral votes for Biden, 259 votes for Trump and 15 votes for the third-party candidate. All candidates having thus fallen short of the 270-vote requirement in the Electoral College, of course, the election would have gone to the U.S. House of representatives.

So the question recurs. Has the red state versus blue state fracture of the nation’s polity eased materially or even at all since 2020? Is it conceivable that all other things equal, RFK could capture Biden’s 22,256 vote margin of victory in Arizona and Georgia out of the 4.145 million Biden votes cast in these two states?

Actually, we’d put money on it. Biden’s razor thin margin was barely one-fifth of the 114,000 votes received in those two states by the hapless candidate of the Libertarian Party, Jo Jorgenson, and only 0.27% of the total 8.4 million votes cast for president in Arizona and Georgia

According to exit polls, Biden won overwhelming margins of 60% to 85% among young, independent, women, minority and Hispanic voters in these two lynch-pin states. These now sorely disillusioned Dem constituencies, of course, were tailor-made for RFK’s platform and appeal, and now Nicole Shanahan’s presence on the ticket adds a powerful reinforcement to that appeal.

The more compelling conclusion, therefore, is that it’s hard to see how Biden could possibly win Arizona and Georgia again in 2024 with the Kennedy/Shanahan ticket in the race and bearing down hard on Biden’s lopsided vote among traditional Dem constituencies in these (and other) states.

2020 Arizona Presidential Vote (11 Electoral Votes):

2020 Georgia Presidential Vote (16 Electoral Votes):

Indeed, pulling traditional Dem voters out of the Biden column in these battleground states is so crucial that the wealthy Ms. Shanahan might wish to purchase second homes in each of them and campaign there heavily for the duration! And that admonition might well extend to Wisconsin as well, where Biden won by just 20,000 votes out of the 3.2 million cast there in 2020.

Then again, if the race goes to the U. S. House RFK needs to be among the top three electoral vote getters according to the 12th Amendment, which means picking up at least a few electoral votes outright. As a matter of ultra fine-tuned targeting, there are actually two electoral votes in Maine and three in Nebraska that are awarded by Congressional district regardless of the statewide popular vote outcome.

Moreover, among these are the second district of Maine and the second district of Nebraska, which were divided nearly 50/50 on a red/ blue basis in the 2022 Congressional elections. So, possibly, some additional second homes for Nicole!

Another possibility is for the Kennedy/Shanahan ticket to pick-off 15 electoral votes on a whole state basis in New Hampshire, Nevada and New Mexico, or in other smaller states to be targeted by their campaign. The political math is not entirely prohibitive in any of these cases, either.

For instance, the message from the 2024 presidential primaries in New Hampshire was pretty straight forward. Of the state’s voting age population of 1,150,000, just 169,000 or 14.7% voted for Trump and only 134,000 or 11.7% voted for Nikki Haley. Then again, the great preponderant majority, 847,000 voters or 74%, voted in the democratic primary or didn’t vote at all, and some of these are presumably ripe for the taking in the general election.

The fact is, the Kennedy/Shanahan ticket can win legions of disillusioned voters from both the Dem and GOP columns in New Hampshire. They can also put a heavy effort into registering large numbers of previous non-voters who might be responsive to a truly formidable ticket and message in opposition to both wings of the UniParty status quo.

Assuming that the new RFK voter registrants might add say 2.5% to the state’s total, the turnout next November would be about 850,000. So the Kennedy/Shanahan ticket would likely need about 35% or 300,000 votes to win the state’s four electoral votes.

And there is no great mystery as to where these 300,000 voters might come from. That is to say, the 2020 Democrat primary proved in spades that Joe Biden is far from beloved in the Granite State.

In fact, the votes cast for Bernie Sanders (76,384), Pete Buttigieg (72,454), Amy Klobuchar (58,714) plus Elizabeth Warren, Tom Steyer, Tulsi Gabbard, Andrew Yang, Michael Bloomberg and Deval Patrick totaled 269,720. That was nearly eleven times more than the 24,944 primary election votes garnered by Joe Biden. And that was even before he had become today’s 81-year old semi-incapacitated “Joe Biden”.

Furthermore, with respect to the Republican side, it only needs be remembered that during the 2012 New Hampshire GOP primary, Ron Paul got 25% of the vote against the War Party’s trio of Mitt Romney, Jon Huntsman and Newt Gingrich. So there are a lot of libertarian-leaning, fiscally conservative Republicans in the state that are available, too.

After all, the 2024 GOP candidate defiled the constitution with his lockdowns and made a mockery of the Republican brand on fiscal matters by adding more to the public debt ($8 trillion) than did the first 43 US presidents combined during the initial 216 years of the nation’s history. These Ron Paul anti-war, anti-debt voters thus also need a home, and the Kennedy/Shanahan peace ticket could provide exactly that.

Indeed, in a state teeming with Bernie Sanders and Ron Paul voters and numerous variants in between not named Trump or Biden, the team of Bobby and Nicole should literally resemble kids in a candy store, overwhelmed with the tasty opportunities.

In the case of Nevada, the 2020 exits polls tell you all you need to know. Whereas Biden won the state by a slim 50% to 48% overall margin against Trump, Biden got huge margins among constituencies that are naturally in Bobby Kennedy’s wheelhouse, but also voters with whom Nicole Shanahan could, again, provide some extra punch. These big Biden margins included:

In 2024, all of these sub-groups would be up for grabs and the Kennedy/Shanahan ticket should be well positioned to capture them in droves.

Again, the likely total vote in the state during 2024 will be about 1.4 million, meaning that a 35% margin or 490,000 votes could win Nevada’s six electoral votes.

In the case of New Mexico’s five electoral votes, the math is similar. About 925,000 votes are likely to be cast in November, meaning that a 35% margin for Kennedy/Shanahan would total about 320,000 votes. The math to get there might consist of 30% of Trump’s 402,000 votes in 2020 and 40% of Biden’s 502,000 votes.

Could that many votes be peeled off?

On the Dem side, the 2020 exit polls again point the way. Among voters 44 years or younger, 60% voted for Biden versus his 54% overall margin.

Likewise, 62% of independents and 57% of women voters supported Biden. Of equal significance, among voters who believed the economy was in poor shape, 76% voted for Biden.

Moreover, when it comes to Shanahan’s side of the ticket, it is notable that 61% of those who believed we need sweeping reform of the criminal justice system voted for Biden. And that was along with an 89% Biden vote among those who opposed Trump’s border wall and a 90% vote among those who had a negative view of Donald Trump himself.

All of these voters obviously could be stripped away from the far less formidable “Joe Biden” of 2024.

At the same time, significant parts of the GOP grass roots electorate remain strong fiscal and economic conservatives in New Mexico, as well as in most other parts of red county America. Accordingly, they could be moved into the Kennedy/Shanahan column by the sharp contrast between Kennedy’s pro-balanced budget position and the spending and debt bacchanalia that occurred on Donald Trump’s watch during 2017 to 2020.

In all, the above review encompasses a minimum shift of just 1,100,000 voters to RFK in the five highlighted states out of about 160 million votes which will be cast in the nation as a whole in 2024. That’s about 0.7% of the electorate, and that’s surely doable under the dire circumstances that currently confront the nation and in the context of a Biden vs. Trump choice that 70% of voters deplore.

In fact, RFK’s platform of non-intervention abroad and fiscal retrenchment at home could appeal to millions of disillusioned GOP voters. At the same time, his forthright attacks on crony capitalism and the Fed’s coddling of Wall Street and the rich, his advocacy of a secure border with a wide gate and call for a revival of jobs and growth on main street would also resonate with anti-Trump Democrat constituencies.

This resulting shift in just five states would satisfy the first objective stipulated above and throw the election into the US House for the first time in 200 years. But, alas, that assumes the outcomes in the other 45 states plus DC would be the same.

Ironically, the potential fly in the ointment for RFK is not so much that some 2020 red states would go blue for Joe Biden, but that three purplish states–Wisconsin, Michigan and Pennsylvania—which Biden won by a hair in 2020 could flip back to Trump, who won them in 2016.

As it happened, Biden won Wisconsin by the aforementioned 20,000 votes or 0.6% of the 3.2 million cast. Likewise, his victory margin in Pennsylvania was just 81,000 or 1.2% and in Michigan he won by 159,000 or only 2.9%.

Along with the potential Arizona and Georgia shift to Trump owing to the Kennedy draw from Biden voters as described above, grabbing either Pennsylvania or Michigan in addition would put the Donald back above the 270 vote Electoral College threshold. And that’s even if New Hampshire, Nevada and New Mexico went for Kennedy/Shanahan.

The Kennedy/Shanahan campaign, therefore, must also resolutely chisel away at Trump’s support among economically conservative GOP voters in these three additional battleground states—thereby keeping them in the Biden column so that the 12th Amendment would then come into play.

As we have previously suggested, here are some of the high points RFK would need to emphasize in order to block any Trump gains in these additional battleground states:

Indeed, small government Republicans need to hear over and again from RFK a very important truth: Namely, that Donald J. Trump is a fake economic conservative who will only further impair the cause of constitutional liberty and capitalist prosperity if he is returned to the Oval Office.

Accordingly, there is only one possible way to arrest the flow of history into the very bad place it is now heading via the farce of Trump v. Biden, and from which there is likely no return. To wit, RFK must attract sufficient numbers of economic conservatives in the battleground states to help ensure gridlock in the Electoral College, and to then help him pull a rabbit out of the hat in the U.S. House of Representatives.

As it happens, this third strategic objective may not be quite as implausible as it sounds. If for the first time in exactly 200 years the selection of the President were to be thrown into the U. S. House, California and Wyoming would count as equals via the novel but constitutionally prescribed method of voting en bloc by state delegation.

The person having the greatest number of votes for President, shall be the President, if such number be a majority of the whole number of Electors appointed; and if no person have such majority, then from the persons having the highest numbers not exceeding three on the list of those voted for as President, the House of Representatives shall choose immediately, by ballot, the President. But in choosing the President, the votes shall be taken by states, the representation from each state having one vote; a quorum for this purpose shall consist of a member or members from two-thirds of the states, and a majority of all the states shall be necessary to a choice.

The above is the full extent of the 12th Amendment process, meaning that the battle for the requisite 26 states would be a wide-open political free-for-all as between the top three candidates—Biden, Trump and Kennedy. As mentioned above, within each of the 50 state delegations there is no requirement that House Members vote for the candidate who won their state or to even vote for the nominee of their own party.

At the present time the House of Representatives is nearly evenly divided between the parties—with 27 delegations having a GOP majority, 21 having a Dem majority and two evenly split. And among the 23 smaller states with U. S. House delegations of five or fewer Members, and which are likely to loom large in the contest, the breakdown is:

These configurations could obviously change depending upon the 2024 House elections, but given the extreme degree of red state/blue state gerrymandering after the 2020 Census, the current breakouts are not likely to change appreciably.

Consequently, as the candidate likely to have the fewest electoral votes going into the contest in the U.S. House, RFK’s only route to victory would be to leap above the current red versus blue partisan configurations and seek to coalesce ad hoc majorities among traditional Kennedy Democrats and GOP economic conservatives within the delegations of 26 target states.

Again, Nicole Shanahan should prove to be a valuable assist in keeping traditional Kennedy Democrats in the fold by helping to counter the brutal attacks of Kennedy family members who are on the DNC payroll, as well as the Washington Democrat apparatus facing the prospect of being firmly and finally defenestrated in the halls of power.

For instance, Michigan is currently split 7 to 6 on a blue/red basis. So to line-up the seven-vote margin that would be required to win the Michigan delegation, RFK would likely need to obtain several Dem votes from rustbelt and/or minority-represented districts in southeastern Michigan, perhaps matched up with several outstate GOP Members who are strong economic conservatives per the Gerald Ford/Robert Taft form of midwestern Republicanism that has long prevailed in the Grand Rapids and western areas of the state. Many of these counties in recent times elected solid economic conservatives such as Reps. Justin Amash and Bill Huizenga and back in the day, of course, were the bedrock of our own terms in the U.S. Congress.

While a tall order, we can think of no better combo to double-team the Michigan House delegation than Kennedy and Shanahan.

Likewise, Pennsylvania is currently split 9 to 8 on a blue/red basis, North Carolina is aligned 7 to 7 and the blue/red split in Virginia is 6 to 5. In all cases it would likely require a coalition of Kennedy Democrats from the urban areas and GOP independents from the hinterlands to win the state’s vote.

We would leave it to the RFK campaign, of course, to identify the reachable “Kennedy Democrats” in the most promising state delegations, but this much we can offer with respect to prying loose potential free agents among the red district delegations. In a word, the needed votes for Kennedy are not likely to be found among adherents of the present-day GOP ideological factions, who are mainly united not by philosophy but by the party’s Washington-based fundraising machine.

These non-economic “issue” based factions include hardcore right-to-lifers, culture warriors, law and order howlers and neocon warmongers. These are essentially all rightwing statists, devoted to stimulating government action aimed to set the world aright as they see it.

Needless to say, they are also careerists cogs in the Washington GOP’s fund-raising machine. They like UniParty rule as it is now practiced, even if it is ultimately leading the nation to hell in a hand-basket. So they are likely go off into a rant about young Ms. Shanahan’s leftwing history and connections, anyway.

Fine. At the end of the day, these faction-based Republicans are not likely to desert The Donald because he’s a rightwing statist, too. During four years in the Oval Office, he has already proved beyond a shadow of a doubt that what he is really about is aggrandizing his own Brobdingnagian ego by mobilizing presidential power on behalf of whatever scheme, phantasm or bugbear strikes his fancy at any given moment.

To the contrary, the overwhelming problem in America today is too much state, not too little effort by Washington to pursue monsters abroad or to root out ills that lie outside of the proper keen of the Federal government. So let wokedom in the local schools or crime in the big cities be handled by state and local governments as the framers of our federal form of government intended.

By “too much state” we are also referring, of course, to the nation’s mushrooming fiscal disaster and to the corporate-capture of state agencies, most especially the Federal Reserve and the national security apparatus.

These deformations were at one time anathema to the heartland GOP and they could resonant once again with a Kennedy/Shanahan campaign focused on an intelligent version of America First, which we have called Fortress America, and a sweeping fiscal retrenchment hinged upon bringing the Empire home.

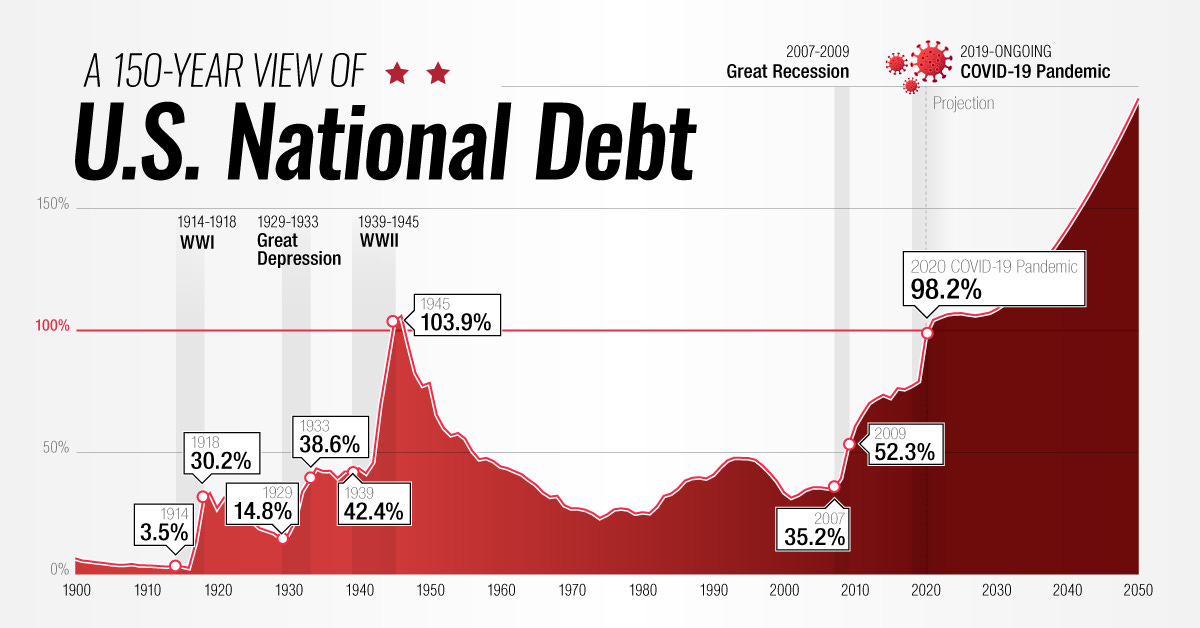

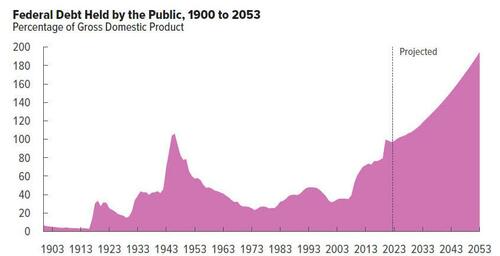

The fact is, the nation’s fiscal condition is no longer within the manageable historic lane where the old school GOP pilloried virtually every drop of red ink and the Dems said not to worry because deficits stimulated growth and were far below peak levels reached during WWII. The public debt thus ebbed and flowed in response to partisan policy maneuvers and the business cycle.

No more. The fiscal equation has gone completely bust and has been festering for decades, with public debt surging during economic downturns while being barely rectified, if at all, during periods of macro-economic recovery and expansion. Consequently, when the budgetary flimflam and Rosy Scenario economics are removed from the latest 10-year CBO budget projections, long-term spending levels are now pinned at 25% of GDP and rising, while Federal receipts are dug in at barely 17% of GDP on a permanent basis.

That computes to an 8% of GDP annual budget deficit versus what even the optimists at CBO say is a 4% rate of nominal GDP growth. That’s all that can be expected in an economy freighted down with $97 trillion of public and private debt, a bulging retired population heading toward 100 million pensioners and a native-born labor force that is actually shrinking owing to babies which weren’t born during recent decades.

The old saying, therefore, could not be more apt. To wit, when the growth of your outgo is 2X the growth of your income, the upkeep on your debt service payments will quickly become your downfall.

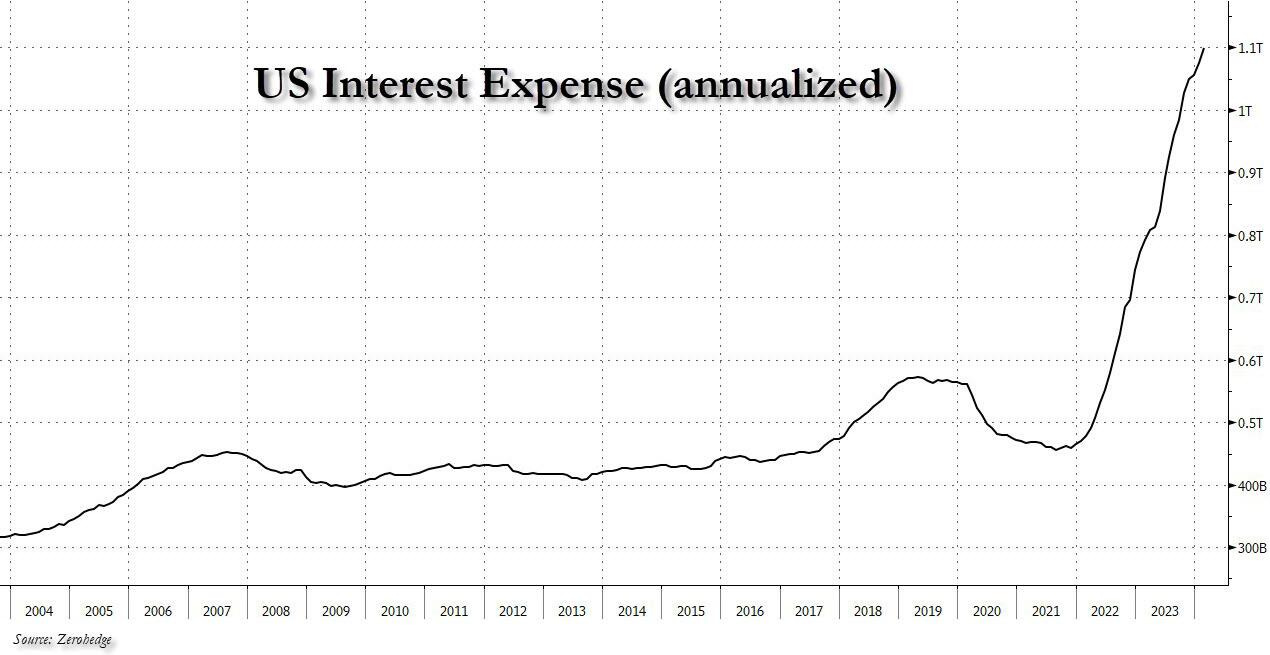

In fact, there is no doubt about it. A few years back Federal interest expense was $300 billion per year, but has already vaulted to nearly $1 trillion. But that’s on public debt which is $34 trillion and a weighted-average rate of interest that is still under 3.0%.

The fact is, even if a small amount of undue optimism is excised from the latest CBO projections, the public debt will exceed $60 trillion by the mid-2030s and the weighted average cost of Treasury bills, notes and bonds, which is already pushing toward 5.0%, is likely to be heading even higher. The Fed has simply printed itself into a hopeless inflationary corner and will be in no position to massively monetize the debt in the future, as it has done relentlessly since 1987.

In any event, the resulting math computes to $3 trillion of annual interest expense a few years down the road, thereby constituting a fiscal millstone that could bury the nation’s finances in a doomsday loop of self-feeding disaster. In fact, the impending struggle to contain exploding debt service expense will make historic partisan battles on fiscal matters look like petty squabbles by comparison.

And that’s why RFK—the only honest, informed and sentient candidate among the three—can hammer the fiscal issue with absolute intellectual rigor and integrity in his quest for the vote of 26 state delegations in the U.S. House.

That’s the issue that can powerfully connect with GOP economic conservatives. Above all other threats, there is now an interest expense time-bomb literally ticking toward ignition but RFK is the only one of the three which can credibly address it.

And this gets us to the larger War & Peace issue, where Robert Kennedy and Nicole Shanahan are united on a playbook wholly different from that of Biden and Trump. Only they can use this issue to break the fiscal logjam that now exists owing to the collapse of counter-vailing partisan positions that had kept the fiscal equation reasonably contained in the past.

That it to say, once upon a time the GOP was the party of lower Welfare State spending, the Dems were the champion of higher taxes mainly from the affluent, and both parties saw the Warfare State as an unavoidable necessity of the Cold War that needed to be minimized to the extent practical.

But when in the 1980s Ronald Reagan cut taxes deeply, the neocons fostered a drastic rise in the defense budget and Alan Greenspan installed the doctrine of “wealth effects” Keynesianism at the Fed, everything changed. The partisan policy differences that tended to contain the Federal deficit just plain vanished.

Instead, all three broad components of the fiscal equation became insurmountable partisan barricades. Yet no fiscal crisis immediately ensued because the Fed made chronic deficit finance temporarily easy by monetizing the US Treasury’s enormous emission of debt paper.

At the same time, the GOP turned tax increases into political poison while continuously chipping away at current revenue levels as a policy principle of first resort. The Dems, in turn, transformed Social Security, Medicare and other entitlements into the third-rail of American politics. And the disappearance of the Soviet Union in 1991 notwithstanding, the hawks and interventionists of both wings of the UniParty became the ferocious champions of a needlessly ballooning Warfare State.

The trigger for the latter was the massive Reagan defense build-up after 1981, which funded a huge increase in conventional military capacity. It was upon the latter that the Forever Wars of invasion and occupation were made possible in the 1990s and beyond.

As it happened, however, almost everything that was funded as the defense budget rose from $140 billion to $350 billion during the early 1980s had never really been needed to contain the rickety Soviet Empire, which collapsed under its own socialist weight by the end of the decade. These superfluous conventional warfare capabilities included the 600-ship Navy, thousands of new fixed wing and rotary aircraft, new generations of main battle tanks, armored personal carriers and other land warfare equipment, a vast expansion of air and sealift assets and a multitude of new conventional missiles and electronic warfare measures.

Needless to say, these capabilities were just what the generals needed to launch the first Gulf War and all the subsequent pointless Forever Wars which have ensued. And these interventions could be done with a ready-made force in being that required no massive current increase in defense spending, and therefore no Congressional debate about the purpose or wisdom of the serial interventions.

In the process the national security budget has grown to monstrous proportions. During the current fiscal year it will total $1.3 trillion, including $910 billion for defense functions, $74 billion for foreign security assistance and international operations and $320 billion for the deferred cost of the Forever Wars as reflected in mushrooming outlays for Veterans health care, disability and other benefits.

The fact is, economic conservatives should have no illusions whatsoever about Donald Trump’s ability to break the fiscal logjam. That’s because he is dug in on the pro-red ink side of each of the three fiscal barriers that have brought on the current disaster.

He will never be persuaded to slash the defense budget by hundreds of billions, which is the essential key to reining in America’s doomsday spending and borrowing machine. Trump is not only unduly enamored with military “strength” and pomp but notwithstanding his rhetoric about America First, his foreign policy amounts to randomly speaking loudly while waving a big military stick.

At the same time, he has also loudly insisted upon no cuts in Social Security or Medicare and a permanent extension of the $500 billion per year cost of the so-called Trump tax cuts of 2017. In a word, he would not challenge the Dems on the Welfare State, the GOP on the holy grail of low taxes and the the Deep State and its UniParty sponsors on the hideously bloated Warfare State.

Nor is this idle speculation. Donald Trump’s four years in the Oval Office established that he is reckless beyond measure on fiscal matters. During that period he added $8 trillion to the public debt, incurring deficits averaging 9.0% of GDP at a time when national income rose by only 3.6% per annum. That’s downright suicidal.

And given the now soaring cost of debt service—even as the money-printers at the Fed are being forced to normalize interest rates to combat inflation—there is simply no conceivable way forward fiscally under a renewed period of Trumpian fiscal chaos in the Oval Office.

Alas, when it comes to what should really matter to economic conservatives—a restoration of fiscal sobriety—Donald J. Trump is not even remotely fit for purpose.

Exactly 200 years ago was the last time that an insufficient majority in the Electoral College forced the presidential vote into the U.S. House of Representatives. The resulting winner of the 1824 election, John Quincy Adams, was notable not only for being the son of the second president and a Founding Father, but also because he had famously promulgated a few years earlier a doctrine which became the foundation of America’s long and prosperous run as a peaceful Republic during the next 93 years.

But it was not only the phrase “she goes NOT abroad, in search of monsters to destroy” that rings out across the subsequent two centuries. The entire framework in which Adams correctly depicted America’s proper role in the world is profoundly pertinent in 2024. That’s because the latter was destroyed by Woodrow Wilson’s foolish entry into WWI and the subsequent metastasis of John Quincy Adam’s peaceful Republic into a destructive global Empire that threatens to now bankrupt the nation and eviscerate American democracy.

That is to say, the time has long-passed to terminate the interminable Washington search for monsters to destroy abroad and to bring the Empire home. Yet the Uniparty in Washington is so beholden to the vast machinery of war and intervention that neither Trump nor Biden offers even the remotest prospect of embracing that urgent imperative.

By contrast, Robert F. Kennedy Jr. deeply understands that the very future of capitalist prosperity and democratic governance in America depends first and foremost on draining the Swamp on the Pentagon side of the Potomac.

So we come full circle. As a practical matter, the only route to that end is a hung jury in the Electoral College, thereby paving the way for an epochal deal in the U.S House of Representatives. That is, a grand bargain that would enable a Kennedy presidency to dismantle the Empire and return America’s cratering fiscal affairs to some semblance of sustainable order.

In that context, RFK’s 2024 anthem and policy remit might well resonate with the words spoken on Independence Day 1821 by John Quincy Adams

Let our answer be this: America, with the same voice which spoke herself into existence as a nation, proclaimed to mankind the inextinguishable rights of human nature, and the only lawful foundations of government. America, in the assembly of nations, since her admission among them, has invariably, though often fruitlessly, held forth to them the hand of honest friendship, of equal freedom, of generous reciprocity.

She has uniformly spoken among them, though often to heedless and often to disdainful ears, the language of equal liberty, of equal justice, and of equal rights.

She has, in the lapse of nearly half a century, without a single exception, respected the independence of other nations while asserting and maintaining her own.

She has abstained from interference in the concerns of others, even when conflict has been for principles to which she clings, as to the last vital drop that visits the heart.

She has seen that probably for centuries to come, all the contests of that Aceldama (field of blood) the European world, will be contests of inveterate power, and emerging right.

Wherever the standard of freedom and Independence has been or shall be unfurled, there will her heart, her benedictions and her prayers be.

But she goes not abroad, in search of monsters to destroy.

She is the well-wisher to the freedom and independence of all.

She is the champion and vindicator only of her own.

Needless to say, a radical change in conventional electoral math would be needed to achieve an RFK led administration that would enable America to finally return to “her practice” of nonintervention.

Yet as we have detailed above, the route to a history-changing “peace, liberty and prosperity” election of Robert F. Kennedy Jr. in the US House of Representatives might not be as forbidding as it seems. And certainly his bold choice of Nicole Shanahan as his running mate makes it all the more possible.

The warhawks in the Deep State are now beating the drums of war. They felt safe doing so before the Russian election.

Things have changed.

The election demonstrated the Russian population’s biggest complaint is their government is not doing what is necessary to bring Ukraine to heel.

At the same, the SAS-protected Zelensky regime is feeling cornered. Cornered people, in this case, backed by the UK, tend to lash out.

And Ukraine is lashing out.

Only this time, Russia is responding.

Here’s Mark to explain it all: https://meaninginhistory.substack.com/p/its-war

********************************************

MAR 22, 2024

Russia is taking the gloves off, and is saying so. The Special Military Operation is now a “War”, brought about by increasing NATO involvement and targeting of infrastructure in Russia. This is what the American Empire’s Deep State has been doing for decades, now. Supporting terrorists to effect regime change. That’s what we’ve done in the Middle East at Israel’s and the Neocons’ bidding, but they’ve bitten off more than they can chew this time. This, apparently, was what Jake Sullivan’s sudden, unannounced, trip to Kiev was about—to tell the Ukro-Nazis to stop acting like … Ukro-Nazis. Uh, you dance with the one you brung. The US took out the Nordstream pipeline, and now we’re telling the Ukro-Nazis to stop doing terrorism? This is probably driven by electoral politics—gas prices are very high and could get higher quickly. But Russia has escalatory dominance going forward.

Members of U.S. National Security Council and the White House have reportedly started to become Increasingly Frustrated by “Unauthorized Brazen Actions” taken by Ukraine against Russia, including their recent Campaign of Long-Range Drone Strikes having Targeted at least 25 Oil Refineries, Terminals, Depots and Storage Facilities across Western Russia; with some Biden Administration Officials believing these Strikes will cause a Spike in Global Oil Prices as well as Significant Escalation and Retaliation against Ukraine like was seen during tonight’s Large-Scale Missile Attack.

Members of U.S. National Security Council and the White House have reportedly started to become Increasingly Frustrated by “Unauthorized Brazen Actions” taken by Ukraine against Russia, including their recent Campaign of Long-Range Drone Strikes having Targeted at least 25 Oil… pic.twitter.com/Og43VS242v

— OSINTdefender (@sentdefender) March 22, 2024

Peskov is Putin’s press guy:

Russia is now in a state of war, everyone should understand this.–

Russia will continue to act so that Ukraine’s military potential cannot threaten the security of its citizens and territory.

Peskov

Looks like Russia has decided to make its own bingo card.

ayden @squatsons

So now that the U.S has officially asked Ukraine to stop striking Russian oil refineries does that mean what I was saying isn’t propaganda anymore?

Ukraine does not benefit from theses ill conceived strikes.

Russia has strategic reserves that cushion any loss of production.

Russia repairs the facilities quickly.

The supply of oil on the market is already low due to production cuts and this only heightens the prices of gas and oil. Russia wins either way and can out last the U.S. on the issue.

As we have very clearly read in their message to Kiev.

3:59 AM · Mar 22, 2024

— GEROMAN — time will tell – — @GeromanAT

The map of missile strikes on objects in the territory of Ukraine and the approximate flight routes of the used munitions, published by Ukraine, have attracted attention. The maneuvering routes of the Kh-101 missiles and “Harpy-2” drones stand out, designed to bypass known positional areas of Ukrainian air defense and strike targets from unexpected directions. Undoubtedly, the main target of the strikes was the Dnipro HPP, where hits were made on HES-1 and HES-2. According to Ukrainian energy officials, the support structure of HES-2 has been destroyed, crane beams are shattered, and machinery hall and electrical equipment are also damaged. (Military Informant TG)

Russian Market @runews

KREMLIN: ‘SPECIAL MILITARY OPERATION’ IN UKRAINE TURNED INTO A WAR AFTER THE WEST INCREASED ITS INVOLVEMENT

5:00 AM · Mar 22, 2024

Visegrad 24 is the organ of the Visegrad group of Central European countries, of which Poland is the largest member.

BREAKING: Russia strikes the DniproHES hydropower station in Zaporizhzhia. It’s the largest dam in Ukraine. When the retreating Soviet Red Army blew it up in 1941, the flooding killed 100 000 people. Russia is playing with fire

LogKa @LogKa11

Ukrainian Dnipro hydroelectric power station was permanently disabled and put out of service. The engine rooms, water locks and sluice areas are flooded and destroyed

Good luck with this. The Cyrillic here is pronounced “Inside”. ??

— GEROMAN — time will tell –  — @GeromanAT

#Инсайд

MI6 transmitted intelligence information to the Office of the President and the General Staff about a meeting in the Kremlin, at which the scenario of the destruction of the Ukrainian underground gas storage facility was considered as a response to constant UAV strikes on Russian refineries. British intelligence recommends strengthening air defense at underground gas storage facilities in order to preserve Ukraine’s gas storage capabilities.”

5:33 AM · Mar 22, 2024

SMO or War? What’s the diff? My legal guess is that the legal implications are huge. “War” implies that Russian forces will be authorized to act outside the boundaries of the Russian Federation and the former Ukraine, including in international airspace. To attack supply lines and support, intel, recon, targeting, etc. Any assets participating in war on Russia become legitimate targets.

Elijah J. Magnier @ejmalrai

This is a severe and significant announcement:

#Russia declared to be ‘in a state of war’ in Ukraine for the first time and no longer in a “Special Operation”. What is the difference?

The terminology used by a state when taking military action against another country can significantly impact the perception, legality, and impact of the conflict.

Special operation

Limited scope and duration: A “special operation” often implies a targeted, limited military engagement to achieve specific declared objectives. It suggests precision and a focused approach, potentially minimising the perception of broader aggression on wider territories.

Political and legal implications: Describing military action as a “special operation” may be intended to avoid formal declarations of war, which have severe political and legal consequences under domestic and international law.

Perception management: By using the term “special operation”, a state may seek to manage domestic and international perceptions by presenting the action as a necessary, controlled response to a specific threat rather than an outright act of war.

Operational secrecy: Such terminology may also be used to maintain operational confidentiality and limit the information available to the public and the international community.

State of war

Broad commitment: Declaring a “state of war” implies a full military commitment involving the total mobilisation of a nation’s armed forces and resources to the conflict. It suggests a long-term, large-scale commitment.

Legal and formal recognition: A formal declaration of war has significant legal implications, including activating specific laws and conventions relating to war. It also serves as an official recognition of a state of conflict between nations, which can affect diplomatic relations and international law.

Psychological impact: Declaring war can have a profound psychological impact on the populations of the countries involved. It could rally public support for the conflict and prepare the nation for the sacrifices that war entails.

International relations and alliances: A declared state of war can trigger alliances and provoke responses from other nations and international bodies such as the United Nations. It may have broader implications for global peace and security.

The transition from special operations to martial law

The transition from a ‘special operation’ to a ‘state of war’ after a period of time may reflect an escalation of the conflict, a change in strategic objectives, or an acknowledgement of the scale and impact of the conflict. This transition may also be driven by the need to legitimise ongoing military action, to mobilise additional resources, or to respond to international pressure. Such a shift indicates a significant change in the state’s approach to the conflict, with profound implications for its conduct, the legal framework governing its actions, and its relations with other states and international organisations.

Last edited

5:42 AM · Mar 22, 2024

— GEROMAN — time will tell –  — @GeromanAT

Sullivan to Zelensky:

It will be still a victory when only a part of “Ukraine” survives as a sovereign country

(give up ground)

Pentagon:

Ukraine must make difficulty decisions and retreat from some defensive lines (because we run out of money)

and now that:

US told Ukraine not to target oil infrastructure in Russia because that would rise prices.

(so what part of Ukraine has lost do some still not understand?)

Official RU MOD comment on the morning missile raid:

“Today, a massive strike was launched on energy facilities, the military-industrial complex, railway junctions, arsenals, locations of Ukrainian Armed Forces (UAF) units, and foreign mercenaries.

As a result of the strike, the functioning of industrial enterprises involved in the production and repair of weapons, military equipment, and ammunition was disrupted.

Additionally, foreign military equipment and ordnance delivered to Ukraine from NATO countries were destroyed, the redeployment of enemy reserves to the front line was disrupted, and UAF and mercenary units in areas of combat readiness restoration were hit.”

The head of NATO’s Military Committee, Bauer, stated that the alliance is ready for conflict with Russia.

*******

Next up – Russia will establish a war zone in the Black Sea and take out any NATO drones, such as the US MQ-9 Reapers feeding intel to Royal Navy “advisers” in Odessa planning sea-drone attacks.

Some decades ago, I was a commissioned officer in the US Navy nuclear propulsion program. Pulled a couple of WestPac-Indian Ocean deployments as a nuclear engineering officer — I’ve long been familiar with APAC military ops and remain so to this day.

Back then, we patrolled the perimeter — from the Gulf all the way up to the East China Sea.

Call this repost from Mark Wauck a “sentimental journey”.

Mark begins with Nuland and GEROMAN: https://open.substack.com/pub/meaninginhistory/p/out-of-the-frying-pan-into-the-fire?r=9ozk&utm_campaign=post&utm_medium=web

***************************************************

MAR 9, 2024

Civilized people have been celebrating the departure of a key Neocon, Victoria Nuland, from her position in the State Department. So far I’ve seen very little about who will replace Nuland. Today Geroman is claiming that Nuland will be replaced by a “China hawk”. The idea is that the Zhou regime is “pivoting to China” while trying to keep the war on Russia going by means of rhetoric and spending. Here’s what Geroman is saying—with some extra comments:

— GEROMAN — time will tell – 👀 — @GeromanAT

Nuland was taken out for a reason – the new guy is a China hawk – Europe is now in full panic mode because they know that the war US=NATO has caused is now a European problem – good luck producing shells without cheap energy and basically zero own resources.

US used NATO to cut EU off cheap Russian energy – fertilizer – and other important resources.

To be a vassal of US regime comes with a price tag

Macron is afraid – like most of those “Western Leaders” in Europe – because US is shifting focus on China now – and the Russia / Ukraine project has failed epically – and now those idiots just learned that it is on them now to save the day.

Spoiler alert: NATO lost its dirty war… x.com/JBrowsing2023/…

1:45 PM · Mar 8, 2024

JuliusXXVI @JuliusXXVI

Tbh Nuland’s replacement just happened to be down the list next in line. But he has a history of acting as the clean-up guy of failed US policies, if pattern is same that’s what he’ll do this time. US isn’t even sending money anymore so project is over, they have no more policies

— GEROMAN — time will tell –  — @GeromanAT

they could have chosen anyone but picked him – and yes – he is for the cleanup – but also a China hawk

You’ll notice that nobody is actually named. What I’ve read is that John Bass (also here) will be the interim replacement for Nuland, but Julianne Smith is being prepped to be the permanent replacement. Bass has a somewhat controversial record for aggressively interfering in the affairs of the countries he’s been stationed in, but I didn’t pick up any specific “China hawk” references.

There are some reasons to take Geroman’s thesis seriously, despite the increasingly bellicose anti-Russian rhetoric from Zhou and the collective West. For example, the US has closed a deal for basing in three Pacific island nations. This is not actually a sudden policy move—it was made possible long ago and the activation of this plan has been in the works for a while:

Five months behind schedule, the US Senate on Friday approved promised economic assistance for three allied Pacific island nations to blunt China’s influence in the strategically vital region.

The delayed funding for the Marshall Islands, Micronesia and Palau under the Compacts of Free Association (Cofa) found its way through a US$460 billion appropriations package passed by the Senate hours before a midnight Friday deadline to narrowly avert a federal government shutdown.

…

First signed in the 1980s, the Cofa agreements provide the United States exclusive military access to strategic swathes of the western Pacific in exchange for economic help.

I wasn’t able to come up with a map that singled out these specific islands, but these two maps will give you an idea of what’s going on:

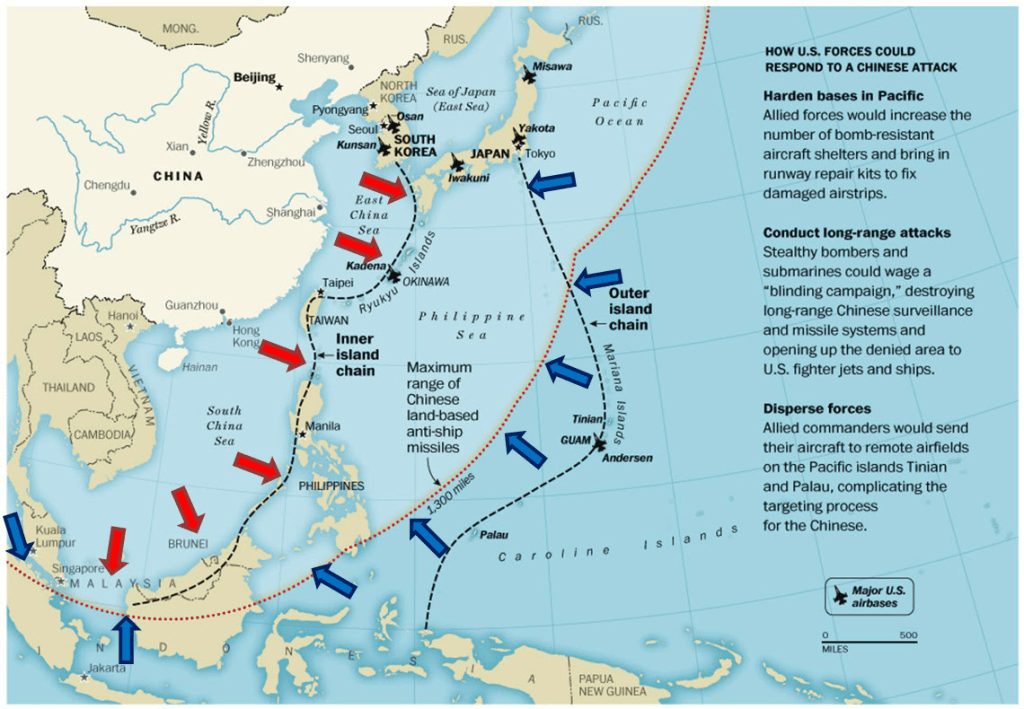

Basically, the US concept is to—optimally—blockade China inside the First Island Chain utilizing US bases and “allied” nations, stretching from Japan and Korea, Taiwan, the Philippines, and down to Malaysia. That first military chain of bases will be backed up by the Second and Third Island Chains further out in the Pacific. The need for the second and third island chains is dictated—as I understand it—by two factors. The first is to protect the US supply chain across the thousands of miles of the Pacific Ocean. The second is to intimidate Pacific island nations—the Solomon Islands come to mind—who might see their interests best served by establishing cordial relations with China. Predictably, China—which is heavily dependent on foreign trade and energy—isn’t inclined to sit back and allow the American Empire to establish a stranglehold over its economy, to be utilized at the pleasure of the US.

[Comment: here is the punch line]

In other words, the American Empire is attempting to solve what is a fundamentally a trade and commerce problem caused by misguided US polices … by military force and intimidation. [Empasis added] For the imperial mindset, every geopolitical issue has a military solution. Why not change the US policies that led to this, instead of blaming China? The ruling oligarchy of the American Empire—which enriched itself by outsourcing American industry—has simply too much money at stake. In essence, our ruling class wants to have its cake—obscene profits from our financialized economy—and eat it too—keep China in industrial servitude as the provider of inexpensive “stuff” that the US no longer makes. The interests of Americans, who are being gradually crushed by what the ruling class has done, are not a consideration for the ruling class. Nor is the increasingly obvious demoralization and decline of American society a consideration, since the ruling class feels secure in its own enclaves. This is what lies behind the American Empire’s pretty nakedly imperialistic adventures: enrichment of the ruling class through the projection of military force to control the world’s resources and trade routes. Virtually every military adventure you can name ultimately fits into this framework. And this is what accounts for the rise of BRICS.

[Comment: got it? No? Then read that paragraph again very slowly.]

Yesterday I briefly outlined my disagreement with Professor John Mearsheimer. Mearsheimer is of the view that the US should be on good terms with Russia—so that we can crush China without hinderance from stupid wars in Europe. In this view Russia would foolishly assume that, having crushed China, the American Empire would never pivot once again to crush Russia and loot it for its treasure chest of resources. YMMV, but I don’t think the Russians are that stupid—not even close. They’ve seen enough of our act. They get it that we can’t be trusted. Here’s what I wrote yesterday:

One thing I want to make clear. I don’t really agree with Mearsheimer regarding China. He characterizes China as a “peer competitor”. To the extent that China actually is such a competitor, however, I think that’s more due to America’s folly in pursuing the impossibility of becoming now and future World Hegemon. China has many problems that are at the core of its national existence. If America retrenches in the direction of pursuing its own limited national interests, China will end up not being anything like a “peer competitor.”

For that reason I also would take issue with the idea that America should regard China as a “threat”, as an “adversary”, or that “containing China [is] America’s principal mission.” I can certainly agree that it’s foolish to push Russia into the arms of China. However, to the extent that China is perceived as a threat, I would maintain—as commenter Cassander did earlier today—that that is mostly do to the cynical and self interested policies of our ruling class in pursuing their own enrichment. Framing this issue as The China Threat simply diverts attention from the real issues and their real solutions.

Not long ago I heard Mearsheimer present his “optimistic” take on China US relations. He maintained that, by 2075, the US would be much more “powerful” than China. Why? Because, he said, the US population is growing while China’s is contracting. I was stunned at this statement, failing, as it did, to account for how America’s population is growing and the quality of the human capital that is causing that growth by walking across our borders.

[Comment: I had the same reaction to John as Mark did. And I hasten to add, I casually knew John a long time ago who gave me very good advice at the time. Always remember him fondly for it. So when John drifts off into his take on US-PRC relations, it’s like … WTF?]

Now, none of this is to say that the US should abandon all national security concerns with regard to China. However, I would suggest that national security for America begins at home. We are surrounded by thousands of miles of ocean. Rather than pursuing the impossible goal of projecting military might around the globe, we would be far better off scaling our objectives back to manageable proportions. That, and securing our home front against rampant foreign interests that are distorting our entire constitutional order. This is our true weakness. We need to build back the moral character of America if we want to influence the rest of the world, rather than relying on purely military force. Unfortunately, this sensible approach is opposed by our dominant ruling oligarchy. I’m not optimistic that the American people will be able to summon up the character to reclaim their country. Only a serious reverse on the foreign war and economic front may accomplish the needed turnaround.

Pivoting back, as it were, to our Euroweenie vassals, you have just shake your head at the stupidity they’re exhibiting. The UK continues to back attacks on Russia, Macron is drawing supposed “redlines” for Russia, and Poland’s new government, ignoring public opinion, is engaged in mindless provocation against its powerful neighbor. Read what Radek Sikorski (Mr. Anne Applebaum) said recently—presuming that Poland has total “asymmetric escalation” dominance over Russia, by keeping Russia guessing. Not kidding. Putin and Shoigu most be having a good laugh:

“In Korea in the 50s there was a coalition of UN countries that fought against aggression. So it can’t be said that this is something unthinkable. So I appreciate the recent French initiative. Because there are good intentions behind it, namely, for the president of Russia to ask himself what our next step will be, so that he is not sure that we will not do anything creative, and therefore could not freely plan his scenarios. This ability of asymmetric escalation should also be on our side.”

What comes through loud and clear is that the Globalist oligarchy gives not a fig for the subject population. Big Serge offered a humorous thread on this subject, with reference to Macron, but the same goes for the rest of these goofballs:

The problem with bluffing is getting called.

Nothing about this threat even makes sense. If you think that Ukraine is worth fighting a war with Russia, you wouldn’t set some weird redline where you pledge to intervene *after* Ukraine has been defeated.

The French Army has eight combat capable brigades (2 armored, 2 mech, 2 light armored, 1 mountain, 1 airborne). French force quality is fine, but this is an expeditionary force that’s not built to slug it out in Eastern Europe.

One is reminded of Bismarck’s famous quip that if the tiny peacetime British Army invaded Germany he would “simply have them arrested”. Given immensely negative reaction from the rest of NATO to Macron’s trial balloon, it’s hard to see France trying to go it alone here.

The balance of things is that Macron is trying to make it look like he’s taking a tough stance on Russia, knowing that the veto from Germany and America will prevent him from actually having to follow through. He can then say “I tried, but the Germans are cowards”.

Threatening to enter the war if Russia gets to Odessa is basically like saying “you better not beat up my little brother, if you knock him unconscious I’m going to hit you.” You wouldn’t wait until your kid brother has already been pulverized to step in.

[Comment: Game-set-match]

It’s standard practice in nuclear ballistic missile submarine fleets throughout the world to periodically demonstrate you can actually launch a warbird successfully.

“Success” is defined as the warhead lands within the down-range target area.

Another measure of success is you don’t destroy your boat trying to light one off.

The Royal Navy dodged “yet-another” bullet the other day in one of its recent Trident missile tests — they seem to repeat their failures regularly.

Even back in my day, the Royal Navy was a sketchy operation.

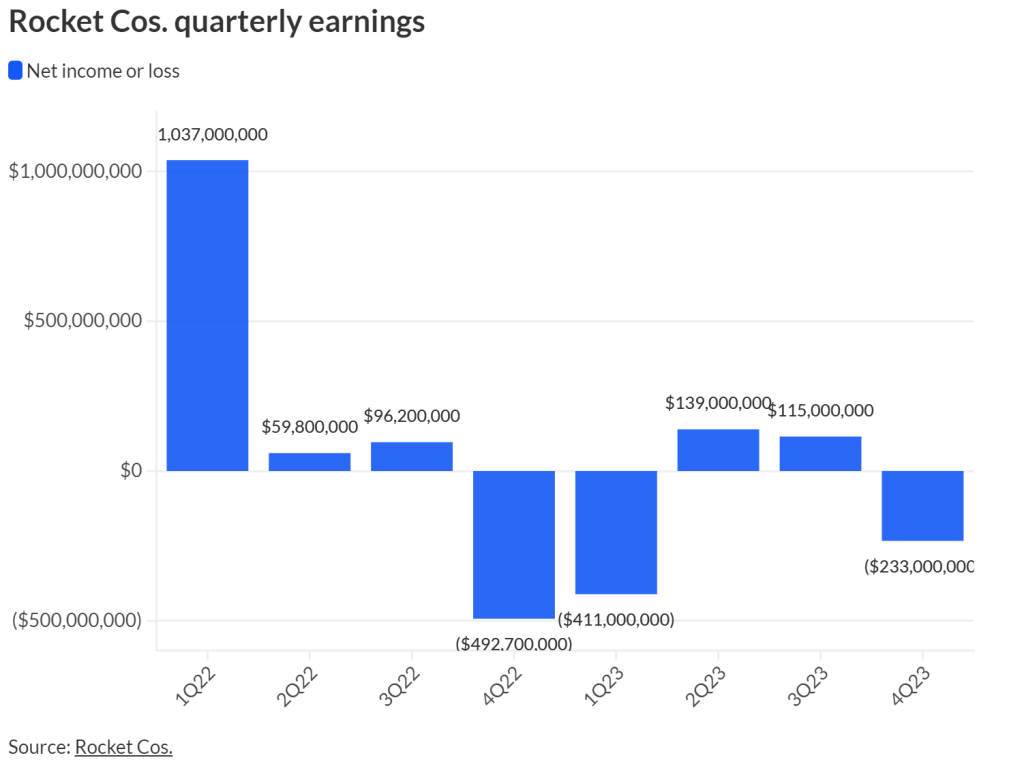

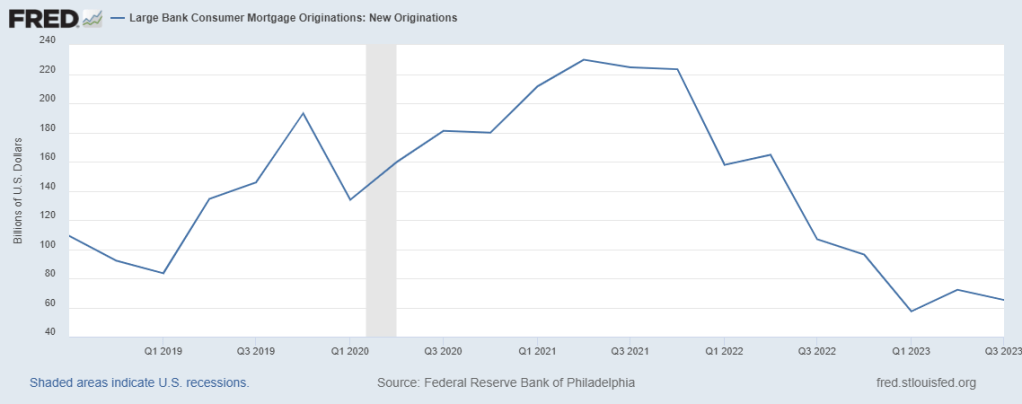

Seems the mortgage business is getting pretty sketchy. We can check out Rocket recent results

National Mortgage News reports Rocket had a bad Q4: https://www.nationalmortgagenews.com/news/rocket-companies-posts-233-million-net-loss-in-q4

By Andrew MartinezFebruary 22, 2024, 7:07 p.m. EST

Rocket Cos. lost $233 million in the final months of 2023, sending its full-year mark deep into the red.

Executives for the Detroit-based giant Thursday touted the firm’s artificial intelligence bona fides and cost-cuttiing amid its step back in quarterly and annual performance. The company, which had predicted a difficult period, saw net income fall from $114.9 million in the third quarter, but improved on its $492.6 million net loss to close 2022.

The fourth quarter of 2023 pushed Rocket’s net loss for the year to $390 million, also a major step back from the $699.9 million profit it reported amid the market’s downswing at the end of 2022. Rocket posted adjusted net revenue of $885 million in the fourth quarter – a figure above guidance that Chief Financial Officer and Treasurer Brian Brown attributed to stronger origination metrics.

“We delivered these achievements in what was one of the worst quarters for mortgage origination in recent history,” he said in a conference call Thursday evening.

Rocket Mortgage counted total origination volume of $17.2 billion between last October and December, down 22% quarterly and 9% less than the same time in 2022. Over 2023, originations hit $78.7 billion, a steep decline from the $133 billion in volume in 2022.

Origination volume in the direct-to-consumer channel of $10.36 billion and in Rocket’s partner network, including Rocket Pro TPO, of $8.46 billion were down quarterly and year-over-year as well. Each channel also saw steep dips in volume compared to the same period last year.

Brown and CEO Varun Krishna in Thursday’s call emphasized Rocket’s cost-cutting, with annual expenses falling from $5 billion in 2022 to $4.2 billion in 2023. The business said it cut its project list by more than 80%, slashing or pivoting efforts including Rocket Auto and Rocket Solar for solar upgrade loans.

Rocket’s prominent AI focus is apparently giving it an edge in originations. In December, its underwriters didn’t have to intervene in nearly two-thirds of income verifications, a fivefold improvement compared to a year-and-a-half earlier, the company said.

“AI is something that you have to have a right to win. and a right to win means you have to have the assets,” said Krishna. “Because of those ingredients that we have at scale, It’s why we expect to be a benefactor.”

The lender’s gain on sale margin of 268 basis points was down from the third quarter’s 276 bps, but up from the 217 bps at the same time in 2022. Brown told an investor it was hard to say when the company would reach the 300 bps GOS margin of years past, but capacity exiting the market will help.

“Now we’re starting to actually see it flow through in terms of pricing competitiveness,” said Brown of industry capacity reductions.

Rocket held $6.4 billion of mortgage servicing rights at the end of the year, a number that’s dipped slightly over the past five quarters. The company is actively bidding on MSRs, and Brown said the supply isn’t great amid aggressive bids by other industry players.

The CFO also expressed confidence in Rocket regarding recent comments by Treasury Secretary Janet Yellen suggesting a nonbank lender could fail amid market stress. Rocket’s balance sheet and liquidity of $9 billion are among, if not, the strongest in the industry.

“It’s something we’ll pay close attention to, but in a lot of cases, new regulations like this could actually increase our competitive advantage and sometimes even increase the moat around this business,” he said.

****************************************

To put Rocket in context, consider some market trends.

The 30-year fixed rate mortgage is up 2x since 2021. And not going anywhere until Powell cuts rates which seems like “not for a while.”

Originations?

When I reported to my boat way back when, Rocket Man was on our sound track. I’m not an Elton fan but the line still resonates from standing a lot of otherwise quiet backwatches.

“All the science I don’t understand, it’s just my job 5 days a week.”

Mark Wauck: https://open.substack.com/pub/meaninginhistory/p/ukraine-update-7b7?r=9ozk&utm_campaign=post&utm_medium=web

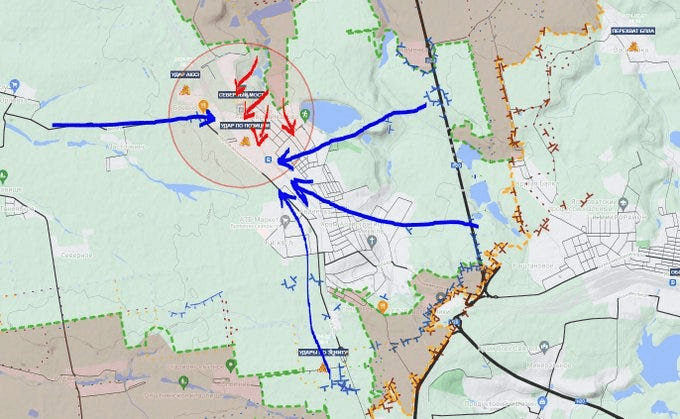

Today looks like it’s time for a small update on the fighting in Ukraine. Avdeevka is perhaps the most fortified Ukrainian stronghold. It’s the fortress city from which the Ukrainians have used artillery to inflict civilian casualties on Donetsk City. This is a big victory for Russia and could signal further breakthroughs. There is heavy activity all along the front, from south to north—constant Russian pressure forcing Ukraine to commit what reserves they have.

— GEROMAN — time will tell – — @GeromanAT

The Battle for Avdeevka is lost for Ukrainians – but the battle is not over yet. AFU will either try to fight its way out of the city – or hold on to the last man to gain time for a better line of defense further in the West. One is clear – Russian forces won’t make it easy for AFU – no matter what they will try. Artillery and aviation is working – RF is pinning down AFU on the outskirts – making it harder to leave post – and moving deeper into the center to split the cake for good.

both – Ukrainian and Russian sources report Russians are dropping an insane number of FABs on the remaining AFU positions in Avdeevka – more than 40 counted in the last hours – while RF have now basically FULL fire control on the remaining supply route – looks like AFU will be wiped out there in the next 48h – or they will call VOLGA

FABs are gravity bombs that come in many sizes, but these are the very heavy variety for use against deeply fortified positions. The US provides such bombs to Israel for use against Palestinian civilians.

VOLGA is the surrender hotline the Russians have set up for Ukrainian troops to use.

Military Summary @MilitarySummary

Information is coming from different sectors of the front about multiple breakthroughs by the Russian Armed Forces along the entire line of combat contact. There is an operational crisis, and if the Ukrainian Armed Forces cannot stabilize the situation, the crisis could instantly develop into a strategic one.

In the near future, American journalist Tucker Carlson will publish an interview with Putin. This is expected to be another blow to a weakened Biden and Zelensky, who has almost lost all hope.

— GEROMAN — time will tell – — @GeromanAT

and we saw how it works in the last 24h. Russia broke through on several locations. AFU is in a real operational crisis. And this tactics (to attack everywhere – even if just a little) – is also used all along the lines. AFU had to shift reserves to keep Avdeevka open – Russia attacked towards Terny – and Kupyansk – AFU is shifting forces to the north – RF is advancing in Marinka and south of Avdeevka. So – again – we won’t see any “big arrows” in the coming months – there is no need for that at all. And the idiotic assumption by “Western Experts” – that Russia “will take Kupyansk as a gift for Putin to win the elections” is another sign of desperation in the NATO camp – they create another “time line” – “Russia will take this or that unit 24th of Feb – or until elections” – this is another attempt to create a virtual victory for the losers club. Russian military doctrine has nothing to do with “we have to take that to show the West” – for Russia this war is like all others – take out the enemy – and try to avoid idiotic losses just for political reasons. But I’m sure the idiots in the NATO camp won’t understand this at all. All their military decisions were based on idiotic assumptions and PR.

Big Serge @witte_sergei

Avdiivka is collapsing in real time. Incredible. Russia is bombarding the remaining corridors, and it looks like the Ukrainian evacuation order was real, as well.

4:58 PM · Feb 7, 2024

I agree with Danny Davis’ assessment today that it’s questionable whether Ukraine can avoid collapse before the November US elections.

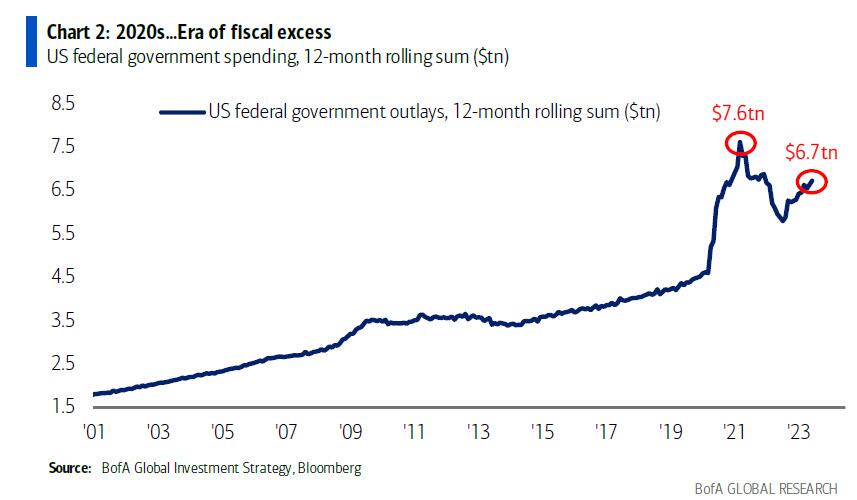

Remember when we showed that the “stealth” secret sauce behind Bidenomics was nothing more than a massive, multi-trillion debt-fueled spending spree, which led to the biggest peactime, non-crisis budget deficit in US history, with the total deficit for fiscal 2023 ending just over $2 trillion, or double the prior year, something which BofA’s Michael Hartnett called the “era of fiscal excess”?

Well, we have news for you: if 2023 was bad, 2024 – an election year of course – is shaping up to be far worse.

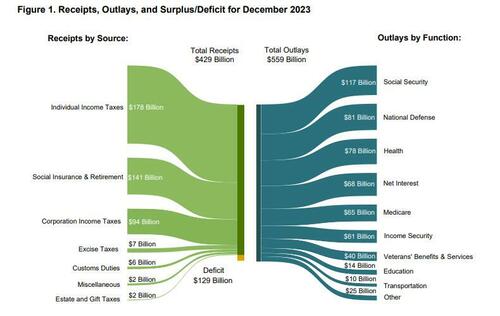

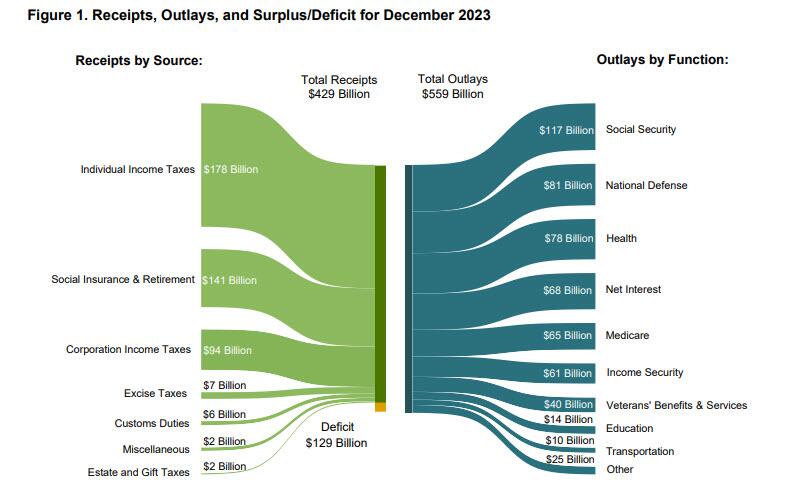

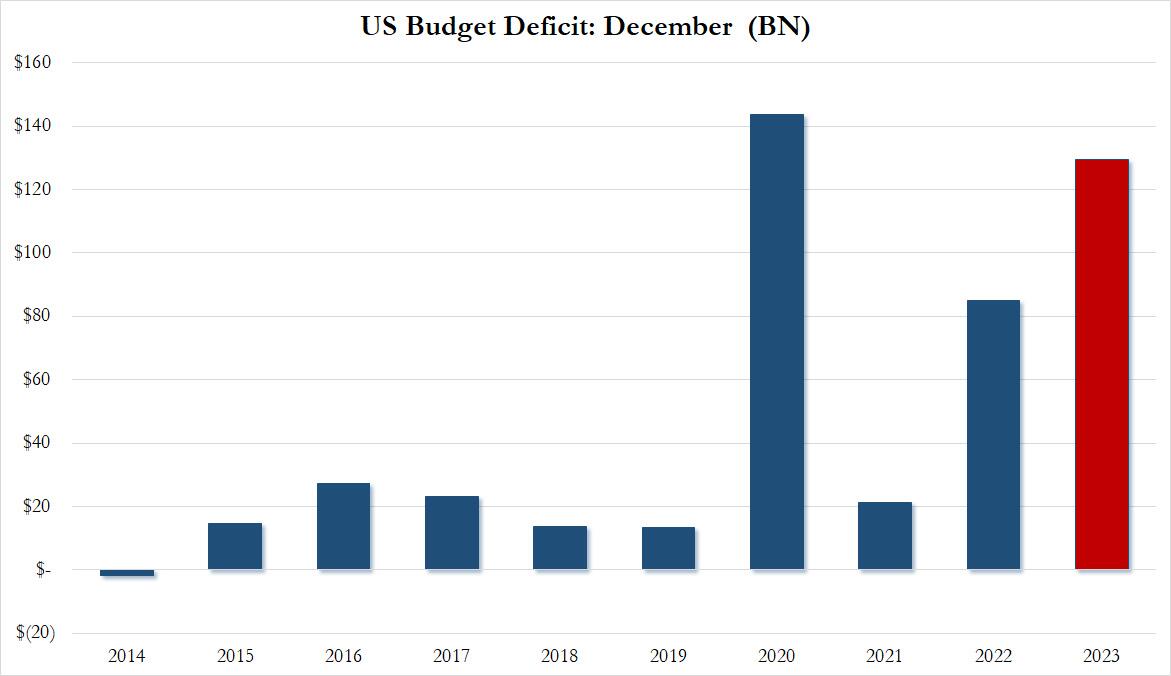

Moments ago the US Treasury reported the budget deficit picture for December and it will come as no surprise to anyone that the US has continued to spend like a drunken sailor, or rather, even more. As shown in the chart below, in the month of December, the US collected $429 billion through various taxes, while total outlays hit $559 billion…

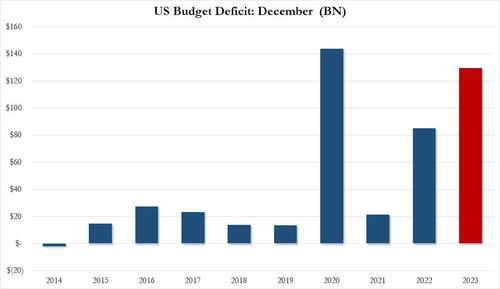

… resulting in a December deficit of $129.4 billion.

This may not sound like a lot, but December is actually one of those months when the US deficit is relatively tame, or used to be.

As shown in the next chart, traditionally the December deficit was barely in the $10-20BN range… until 2020 when it exploded to an all time high of $140BN. And while it dropped sharply in 2021, it rebounded dramatically in 2022, and rose to just shy of the December crisis high last month!

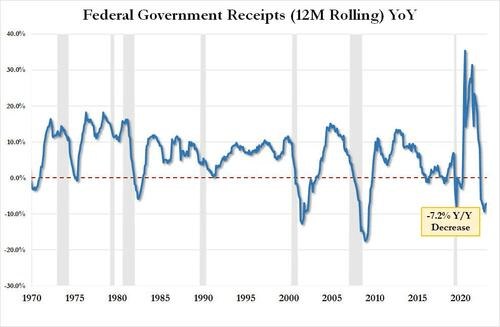

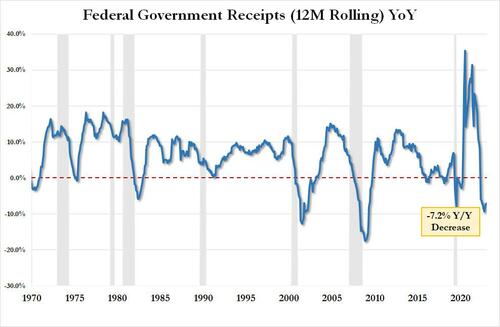

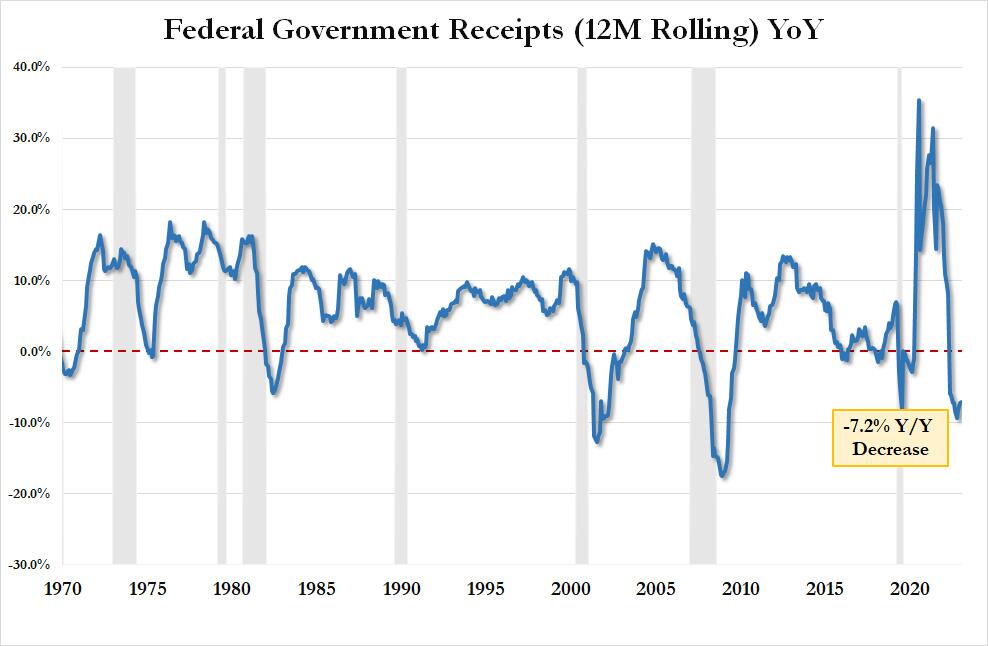

Here is some more context: tax receipts of $429.3BN in December were down 5.6% from the $454.9BN in December 2022 and down a whopping 11.8% from December 2021. On an LTM basis, US total tax receipts were $4.521TN, or down 7.2% YoY. This is now the 9th consecutive YoY decline in LTM tax receipts, something that historically has only taken place when the US was in a recession. As an aside, the “smart economists” were certain that the collapse in tax receipts would reverse after November when the postponed California taxes would be collected. Well, November has come and gone and the big picture is just as ugly.

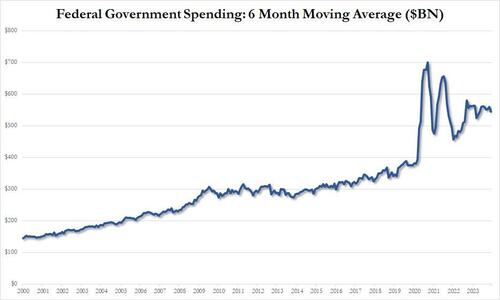

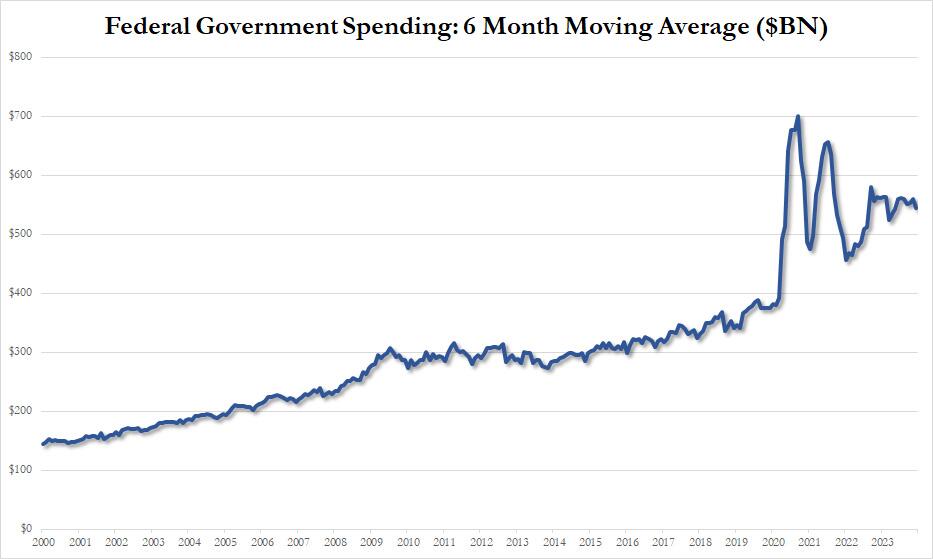

Looking at outlays, unlike tax receipts, there is danger of a decline… ever; and indeed in December the US spent a total of $559 billion, up 3.5% from the $540BN spent a year ago, and up even more from the $508BN in 2021. On a 6 month moving average basis, we are rapidly approaching the exponential phase even when accounting for the spending burst in 2020 and 2021.

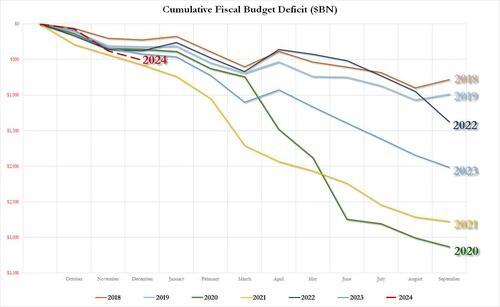

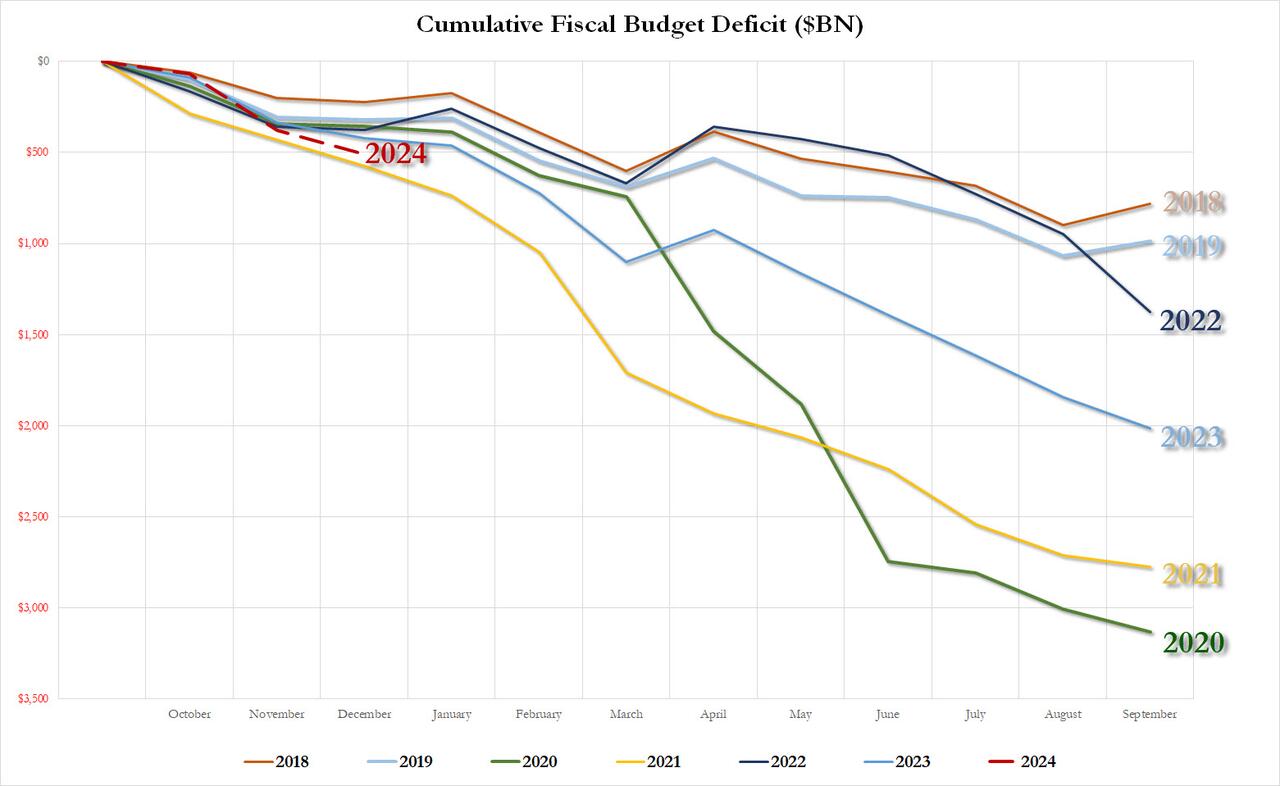

Putting it all together, we get the scariest chart of all: the YTD budget deficit three months into fiscal 2024 is already $509 billion, which would be the biggest deficit in US history after one quarter with the exception of the covid outlier year of 2021 when the US injected multiple trillions in stimmies.

As for the final, and most shocking, data point, the December budget deficit of $129.4 billion was more than $40BN higher than the $87.5BN median estimate, and was more than 50% higher compared to the $85BN December deficit in fiscal 2022.

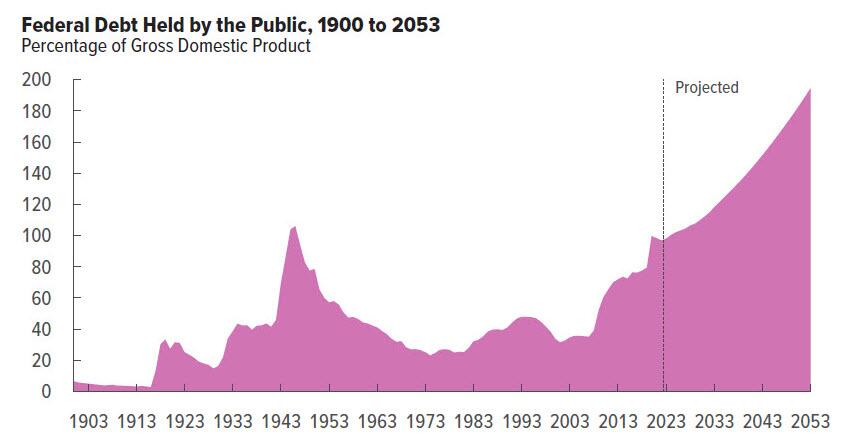

Needless to say, this is completely unsustainable and assures fiscal collapse for the US, not if, but when. Then again, we already knew this thanks to the CBO which was kind enough to chart the endgame:

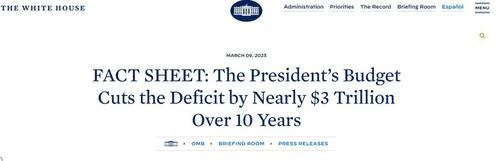

What is funniest about all this is that the US is on an accelerating path to ruin less than one year after the imposter in the White House published this laughable propaganda.

We can’t wait to see what really happens to the budget deficit over the next 10 years. Spoiler alert: there won’t be a happy ending.

One of the more interesting bloggers regarding the NATO-Russia Proxy War. He leverages Simplicius of Cilicia, a Greek Neoplatonic philosopher and polymath who wrote commentaries on Aristotle and Plato. He provides in depth geopolitical and conflict analysis, with a dash of the sardonic. You can support himby pledging here or tipping at: http://www.buymeacoffee.com/Simplicius.

************

This past July, one of the most remarkable articles of the entire Ukrainian war flew under the radar. I’ve had it sitting on my tab for weeks now, but could never quite fit the information in. It is so eye-opening, and dispels so many narratives in the West, that I thought it deserving of its own writeup; particularly because it has flown so under the radar for whatever reason, causing most people to miss its many juicy revelations.

The article is the following from Newsweek:

Its age does not detract from its significance as the information therein is more pertinent than ever—which is precisely why I chose to do an exposé on it now.

The reason is, as the Ukrainian war presently enters a new watershed phase characterized by the slow-acceptance of Ukraine’s now de facto losing position, a proverbial windmill of narratives is churned out from the pro-UA side seeking to somehow reconcile the various cognitive dissonances created by their inability to understand how it is possible that the mighty NATO bloc could be losing to Russia.

This results in their proposing increasingly convoluted theories as to why the US may be “deliberately sabotaging” Ukraine’s otherwise guaranteed “victory”. For instance, a common coping narrative you might hear these days is that the US “fears” Ukraine winning a total and ‘decisive’ victory over Russia because this would cause Russia to “fracture” into many small feudal states, which could precipitate an existential crisis as the warlords of the new states would vie for the now unaccounted for nuclear weapons, etc. Though it is obviously preposterous, this is the type of narrative being floated on pro-UA thinkspaces to try and explain away the US’s perceived weakness and ‘cowardice’ in the face of Russia’s growing dominance.

They simply cannot understand how it is possible that the US would not stand up to the putatively “weak” Russia. In their mind, addled by two years of propaganda characterizing Russia as a totally dysfunctional failed state with an unimaginably weak military, it’s simply impossible to reconcile these two quotients. So the only logical inference is that it is an intentional act by the US—the only remaining question being why the US would intentionally condition Ukraine’s loss.

But the article dispels such fantasies and reveals some of the real reasons behind US’s seemingly perplexing posture.

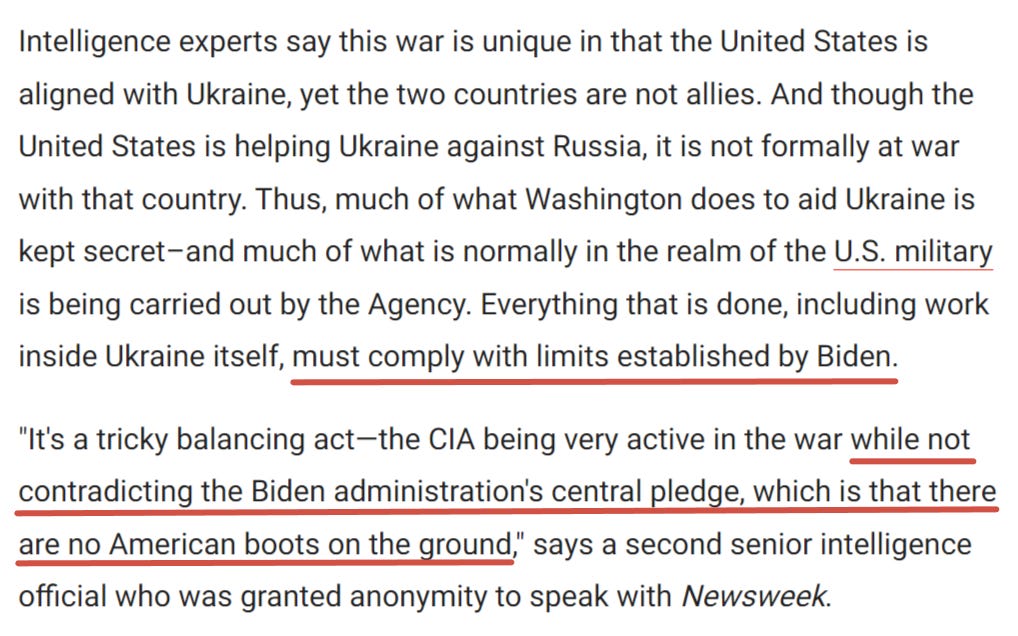

Firstly, the article revolves around—as per usual—the statements of an anonymous “senior intelligence official” from the Biden administration, who is “directly involved in Ukraine policy planning,” and notes that the topics discussed therein are ‘highly classified matters’.

The first significant offering is the following:

That the Ukraine war is a clandestine war, with its own set of clandestine rules, and that one of the CIA’s chief roles is to prevent the war from spiraling too much out of control. This will come into heavier play later.

The senior official goes on to clarify the latter position:

“Don’t underestimate the Biden administration’s priority to keep Americans out of harm’s way and reassure Russia that it doesn’t need to escalate,” the senior intelligence officer says. “Is the CIA on the ground inside Ukraine?” he asks rhetorically. “Yes, but it’s also not nefarious.”

What he reveals there is likewise significant: the Biden administration has an absolute priority in reassuring Russia to keep Russia from escalating too much. Why would that be? The answer is the broader theme of my entire article.

In fact, Newsweek states that the article is the culmination of three long months of intense trail-following and digging into the CIA’s covert operations in Ukraine.

Again, they highlight the chief operative pillars:

The second official says that while some in the Agency want to speak more openly about its renewed significance, that is not likely to happen. “The corporate CIA worries that too much bravado about its role could provoke Putin,” the intelligence official says.

You can see the common theme of the constant prudential tip-toeing around Russia’s redlines so as not to excessively provoke Putin.

They go on to express that the CIA is keen to distance itself from any of Ukraine’s more provocative actions, like the Nordstream attack, or strikes on Russian territory.

But the key portion of the article, which comes next, is the admission that Biden dispatched CIA director Burns to Russia on the eve of the invasion in late 2021. They had been watching Russia’s troop buildups, and in essence sent Burns to deliver a final warning of consequences should Russia proceed with an invasion. Though Putin ended up “snubbing” the CIA head by staying in a Sochi resort and refusing to meet him in person, he did take his secure phone call from Sochi.

What comes next is the heart of the entire article and is one of the most significant and remarkable admissions of the entire war. It is a must read:

Read that several times to comprehend the gravity of it, as this one statement alone single handedly explains and encapsulates the entire dynamic of the war.

Once again I’m forced to be the bearer of the news that not all is as it seems on the surface. Russia isn’t the 10 foot giant some have built it up to be, nor is it a dwarf. Likewise, the US isn’t some uncompromisingly all-powerful entity that does what it wants at all times with zero qualms or concern for repercussions.

This may be a difficult point for some to swallow; after all, how is it possible in actual practice that the US could be fearful of Russia’s reprisal? After all, the US has its vaunted fleets that sail unchallenged through every sea; just the US’s naval air wing alone, believe it or not, makes up the second largest airforce in the entire world. That’s right, just the Navy, which itself pales in comparison to the Airforce, has more planes than the entire Russian airforce. What could such an imposing powerhouse possibly fear from little ol’ Russia?

It stems from the misunderstanding of the actual logistical nuances of the US’s force projection capabilities in the European theater. The people confused by these revelations are those who easily fell prey to a very generalized and caricaturized image of the US military’s operations therein. They’ve developed a blanket image of US forces being able to operate all over Europe, instantly bringing to bear endless stealth craft, unlimited unstoppable missiles, hundreds of thousands of troops, etc.

But that’s far from reality. The US is direly overstretched; its most critical bases in Europe—the ones actually capable of fielding the types of platforms that could actually do anything against Russia, are highly vulnerable. The US has further learned from the Ukrainian conflict that its most advanced air defense is virtually helpless against Russia’s top missiles. Reuters recently told us that Ukraine alone has 1/3 of all the air defense of the entire European continent, and yet Russia has no trouble penetrating it.

This is not to swing the pendulum too far to the other side and lay unrealistic claim to Russia being able to easily and instantly wipe out all of NATO—no, it’s simply to temper ideas about what US and NATO could realistically do to Russia. At the end of the day, a war between the two could very well be a stalemate but it would come at massive costs to the US/NATO, which is precisely the point that pro-UA supporters have made themselves blind to.

But the internal players—the CIA and policy makers—certainly understand this. Which is why they have openly made clear in the above article that a stringent set of ‘rules of the game’ have been laid out between the counterparties. Russia has obviously made it clear that it is willing to strike NATO assets that are assisting Ukraine if things are pushed too far. The US likewise now understands that Russia indisputably has the capability to do so. Thus they have shaken hands and agreed to limit the trampling of each other’s red lines. Russia will allow the US certain clandestine operations within the purview of the gentleman’s agreement, and the US in turn will venture to keep its rabid dog on a short leash and within the narrow bounds of the playpen.