Two weeks ago, when amid reports that the former CEO of Alameda Capital (which as a reminder was ground zero of the FTX implosion after it blew up $8 billion in FTX client funds on trades gone horribly wrong), Caroline Ellison, was spotted in New York just after retaining Clinton superlawyer, Jamie Gorelick of Wilmer Hale, which as readers may recall was the former No. 2 ranking member in the Clinton Justice Department, and in a recent interview, she referred to current AG Merrick Garland as her “wingman”, we asked if Caroline had rolled on Sam Bankman-Fried, who was also her former lover.

Fast forward to today when we just got confirmation that Caroline Ellison has fucked Bankman-Fried one final time by indeed rolling on him, and “turning states” in the criminal prosecution of the corpulent “Hairy Plotter“, who commingled and stole the client money in his FTX exchange to fund a series of terrible crypto bets at his personal hedge fund Alameda, fund tens of millions in donations to democrats and buy up prestigious real estate for himself and his “altruistic” progressive lawyer parents.

According to a Manhattan Federal prosecutor, two of FTX founder Sam Bankman-Fried’s closest associates have pleaded guilty to fraud and agreed to co-operate with US authorities investigating the collapse of the bankrupt cryptocurrency exchange. In other words, they took a plea deal to avoid even more prison time in exchange for serving SBF on a silver platter to the Feds.

Damian Williams, the US attorney for the Southern District of New York, announced the guilty pleas and criminal charges against Caroline Ellison and Zixiao “Gary” Wang, the low profile co-founder of FTX, in a short video statement. His office had brought eight charges against Bankman-Fried last week.

Statement of U.S. Attorney Damian Williams on U.S. v. Samuel Bankman-Fried, Caroline Ellison, and Gary Wang pic.twitter.com/u1y4cs3Koz

Ellison pleaded guilty to seven counts, including wire and securities fraud and conspiracy to commit money laundering, which carry a maximum sentence of 110 years in prison, while Wang pleaded guilty to four counts of fraud, with a maximum 50-year sentence.

The documents said prosecutors would not oppose bail requests from both defendants under certain conditions, including posting a bond and handing in their travel documents, as they awaited formal sentencing.

Concurrently, the Securities and Exchange Commission and the Commodity Futures Trading Commission also filed civil lawsuits against the 28-year-old Ellison and 29-year-old Wang, accusing them of fraud.

“As part of their deception, we allege that Caroline Ellison and Sam Bankman-Fried schemed to manipulate the price of FTT, an exchange crypto security token that was integral to FTX, to prop up the value of their house of cards,” said SEC chair Gary Gensler. Furthermore, as CEO of the FTX trading affiliate, Ellison “used FTX’s customer assets to pay Alameda’s debts” and diverted billions of dollars of depositors’ money to the company to fill a hole caused by a crypto market crash in May, the SEC’s complaint alleges.

The CFTC said Wang had a hand in creating some of the algorithms that underpinned FTX, which allowed Alameda “to maintain an essentially unlimited line of credit” on the exchange, giving it an “unfair advantage” over regular depositors. “These critical code features and structural exceptions allowed Alameda to secretly and recklessly siphon FTX customer assets from the FTX platform.”

Both defendants are co-operating with the SEC, the agency said. The CFTC said they were not contesting their liability. Which means that SBF is looking at a lot of prison time, unless he too can throw someone even more important and powerful under the bus…

Sam better have someone much bigger to rat on or he is facing about 120 years in FPMITAP. Also, he better get someone to fix his prison cam https://t.co/Krw5u2psZD

… although if that is the case, he probably will be Epsteined within hours of arriving at MDC Brooklyn, singe MCC New York where Epstein “killed himself”, has been closed since August 2021 due to deteriorating conditions.

While Ellison’s superlawyers have yet to make a statement, a lawyer for Wang, Ilan Graff, said: “Gary has accepted responsibility for his actions and takes seriously his obligations as a co-operating witness.”

Last week, the DOJ filed charges against Bankman-Fried and accused him of orchestrating “one of the biggest financial frauds in American history” by misappropriating customer assets from FTX to Alameda Research. He was arrested in the Bahamas, where he lives. He is also facing parallel civil cases from the SEC and CFTC.

Williams reiterated his call for others who worked with Bankman-Fried to come forward. “If you participated in misconduct at FTX or Alameda, now is the time to get ahead of it,” he said. “We are moving quickly and our patience is not eternal.” One of them is former Alameda CEO Sam Trabucco, best known for quietly bailing on Sam just as everyone was about to blow up and fleeing on his multi-million dollar new yacht.

The announcement from Williams comes just after a plane carrying Bankman-Fried took off from the Bahamas, where he waived his right to challenge extradition to the US. He is due to appear in a Manhattan court as soon as Thursday, where his bail request will be considered, although in light of Caroline’s plea, it is safe to say it won’t be granted.

The details in the SEC’s complaint have been laid out nicely by the following twitter account…

We just discovered Caroline Ellison and Gary Wang turned on @SBF_FTX, rattling him out to the Feds. The SEC’s civil (non-criminal) complaint is built on their participation and gives us our first “insider’s account” of the FTX disaster.

… and the full complaint can be found below (link here)

We just discovered Caroline Ellison and Gary Wang turned on @SBF_FTX, rattling him out to the Feds. The SEC’s civil (non-criminal) complaint is built on their participation and gives us our first “insider’s account” of the FTX disaster.

Where it began I can’t begin to know when But then I know it’s growing strong Was in the spring And spring became the summer Who’d have believed you’d come along

Hands, touchin’ hands Reachin’ out, touchin’ me, touchin’ you

Sweet Caroline Good times never seemed so good I’ve been inclined To believe they never would

Moscow has data confirming US’, Poland’s involvement in terror attacks in Russia — agency

According to the specialists’ assessments, a number of facts “confirm the direct involvement of the US and Poland in the massive military-logistical support of the Kiev regime, in preparation and implementation of joint terror attacks on the Russian Federation territory”

MOSCOW, December 16. /TASS/. Data from intercepted drones confirm the involvement of the US and Poland in preparation of terror attacks on the Russian territory, a source in Russian security agencies told TASS Friday.

“Relevant agencies of the Russian Federation analyzed electronic components of the intercepted unmanned aerial vehicles, used by Ukraine for attacks on Russian infrastructure objects – in particular, in Sevastopol, in Crimea, in Kursk, Belgorod and Voronezh Regions,” the agency said.

According to the specialists’ assessments, a number of facts “confirm the direct involvement of the US and Poland in the massive military-logistical support of the Kiev regime, in preparation and implementation of joint terror attacks on the Russian Federation territory.”

The agency noted that “the avionics and drone control stations were produced by US’ Spektreworks, a company that performed the initial tuning and check of the drones at the Scottsdale airport in Arizona.”

In addition, the relevant agencies pointed out that “the final assembly and flight trials of these drones were carried out on the Polish territory, near the Rzeszow airport, used by the US and NATO as the main supply node for Ukrainian armed forces.”

“The installation of payload, flight mission and the launch itself were carried out near Odessa and Krivoy Rog,” the statement says.

Xi Jinping has made an offer difficult for the Arabian Peninsula to ignore: China will be guaranteed buyers of your oil and gas, but we will pay in yuan.

It would be so tempting to qualify Chinese President Xi Jinping landing in Riyadh a week ago, welcomed with royal pomp and circumstance, as Xi of Arabia proclaiming the dawn of the petroyuan era.

But it’s more complicated than that. As much as the seismic shift implied by the petroyuan move applies, Chinese diplomacy is way too sophisticated to engage in direct confrontation, especially with a wounded, ferocious Empire. So there’s way more going here than meets the (Eurasian) eye.

Xi of Arabia’s announcement was a prodigy of finesse: it was packaged as the internationalization of the yuan. From now on, Xi said, China will use the yuan for oil trade, through the Shanghai Petroleum and National Gas Exchange, and invited the Persian Gulf monarchies to get on board. Nearly 80 percent of trade in the global oil market continues to be priced in US dollars.

Ostensibly, Xi of Arabia, and his large Chinese delegation of officials and business leaders, met with the leaders of the Gulf Cooperation Council (GCC) to promote increased trade. Beijing promised to “import crude oil in a consistent manner and in large quantities from the GCC.” And the same goes for natural gas.

China has been the largest importer of crude on the planet for five years now – half of it from the Arabian peninsula, and more than a quarter from Saudi Arabia. So it’s no wonder that the prelude for Xi of Arabia’s lavish welcome in Riyadh was a special op-ed expanding the trading scope, and praising increased strategic/commercial partnerships across the GCC, complete with “5G communications, new energy, space and digital economy.”

Foreign Minister Wang Yi doubled down on the “strategic choice” of China and wider Arabia. Over $30 billion in trade deals were duly signed – quite a few significantly connected to China’s ambitious Belt and Road Initiative (BRI) projects.

And that brings us to the two key connections established by Xi of Arabia: the BRI and the Shanghai Cooperation Organization (SCO).

The Silk Roads of Arabia

BRI will get a serious boost by Beijing in 2023, with the return of the Belt and Road Forum. The first two bi-annual forums took place in 2017 and 2019. Nothing happened in 2021 because of China’s strict zero-Covid policy, now abandoned for all practical purposes.

The year 2023 is pregnant with meaning as BRI was first launched 10 years ago by Xi, first in Central Asia (Astana) and then Southeast Asia (Jakarta).

BRI not only embodies a complex, multi-track trans-Eurasian trade/connectivity drive but it is the overarching Chinese foreign policy concept at least until the mid-21st century. So the 2023 forum is expected to bring to the forefront a series of new and redesigned projects adapted to a post-Covid and debt-distressed world, and most of all to the loaded Atlanticism vs. Eurasianism geopolitical and geoeconomic sphere.

Also significantly, Xi of Arabia in December followed Xi of Samarkand in September – his first post-Covid overseas trip, for the SCO summit in which Iran officially joined as a full member. China and Iran in 2021 clinched a 25-year strategic partnership deal worth a potential $400 billion in investments. That’s the other node of China’s two-pronged West Asia strategy.

The nine permanent SCO members now represent 40 percent of the world’s population. One of their key decisions in Samarkand was to increase bilateral trade, and overall trade, in their own currencies.

And that further connects us to what has happening in Bishkek, Kyrgyzstan, in full synchronicity with Riyadh: the meeting of the Supreme Eurasia Economic Council, the policy implementation arm of the Eurasia Economic Union (EAEU).

Russian President Vladimir Putin, in Kyrgyzstan, could not have been more straightforward: “The work has accelerated in the transition to national currencies in mutual settlements… The process of creating a common payment infrastructure and integrating national systems for the transmission of financial information has begun.”

The next Supreme Eurasian Economic Council will take place in Russia in May 2023, ahead of the Belt and Road Forum. Take them together and we have the lineaments of the geoeconomic road map ahead: the drive towards the petroyuan proceeding in parallel to the drive towards a “common paying infrastructure” and most of all, a new alternative currency bypassing the US dollar.

That’s exactly what the head of the EAEU’s macroeconomic policy, Sergey Glazyev, has been designing, side by side with Chinese specialists.

Total Financial War

The move towards the petroyuan will be fraught with immense peril.

In every serious geoeconomic gaming scenario, it’s a given that an enfeebled petrodollar translates as the end of the imperial free lunch in effect for over five decades.

Concisely, in 1971, then-US President Richard “Tricky Dick” Nixon pulled the US from the gold standard; three years later, after the 1973 oil shock, Washington approached the Saudi oil minister, notorious Sheikh Yamani, with the proverbial offer-you-can’t-refuse: we buy your oil in US dollars and in return you buy our Treasury bonds, lots of weapons, and recycle whatever’s left in our banks.

Cue to Washington now suddenly able to dispense helicopter money – backed by nothing – ad infinitum, and the US dollar as the ultimate hegemonic weapon, complete with an array of sanctions over 30 nations who dare to disobey the unilaterally imposed “rules-based international order.”

Impulsively rocking this imperial boat is anathema. So Beijing and the GCC will adopt the petroyuan slowly but surely, and certainly with zero fanfare. The heart of the matter, once again, is their mutual exposure to the Western financial casino.

In the Chinese case, what to do, for instance, with those whopping $1 trillion in US Treasury bonds. In the Saudi case, it’s hard to think about “strategic autonomy” – such as what’s enjoyed by Iran – when the petrodollar is a staple of the Western financial system. The menu of possible imperial reactions includes everything from a soft coup/ regime change to Shock and Awe over Riyadh – followed by regime change.

Yet what the Chinese – and the Russians – are aiming at goes way beyond a Saudi (and Emirati) predicament. Beijing and Moscow have clearly identified how everything – the oil market, global commodities markets – is tied to the role of the US dollar as reserve currency.

And that’s exactly what the EAEU discussions; the SCO discussions; from now on the BRICS+ discussions; and Beijing’s two-pronged strategy across West Asia are focused to undermine.

Beijing and Moscow, within the BRICS framework, and further on within the SCO and the EAEU, have been closely coordinating their strategy since the first sanctions on Russia post-Maidan 2014, and the de facto trade war against China unleashed in 2018.

Now, after the February 2022 Special Military Operation launched by Moscow in Ukraine and NATO has devolved into, for all practical purposes, war against Russia, we have stepped beyond Hybrid War territory and are deep into Total Financial War.

SWIFTly drifting away

The whole Global South absorbed the “lesson” of the collective (institutional) west freezing, as in stealing, the foreign reserves of a G20 member, on top of it a nuclear superpower. If that happened to Russia, it could happen to anyone. There are no “rules” anymore.

Russia since 2014 has been improving its SPFS payment system, in parallel with China’s CIPS, both bypassing the western-led SWIFT banking messaging system, and increasingly used by Central Banks across Central Asia, Iran and India. All across Eurasia, more people are ditching Visa and Mastercard and using UnionPay and/or Mir cards, not to mention Alipay and WeChat Pay, both extremely popular across Southeast Asia.

Of course the petrodollar – and the US dollar, still representing under 60 percent of global foreign exchange reserves – will not ride into oblivion overnight. Xi of Arabia is just the latest chapter in a seismic shift now driven by a select group in the Global South, and not by the former “hyperpower.”

Trading in their own currencies and a new, global alternative currency is right at the top of the priorities of that long list of nations – from South America to Northern Africa and West Asia – eager to join BRICS+ or the SCO, and in quite a few cases, both.

The stakes could not be higher. And it’s all about subjugation or exercising full sovereignty. So let’s leave the last essential words to the foremost diplomat of our troubled times, Russia’s Sergey Lavrov, at the international interparty conference Eurasian Choice as a Basis for Strengthening Sovereignty:

“The main reason for today’s growing tensions is the stubborn striving of the collective West to maintain a historically diminishing domination in the international arena by any means it can… It is impossible to impede the strengthening of the independent centers of economic growth, financial might and political influence. They are emerging on our common continent of Eurasia, in Latin America, the Middle East and Africa.”

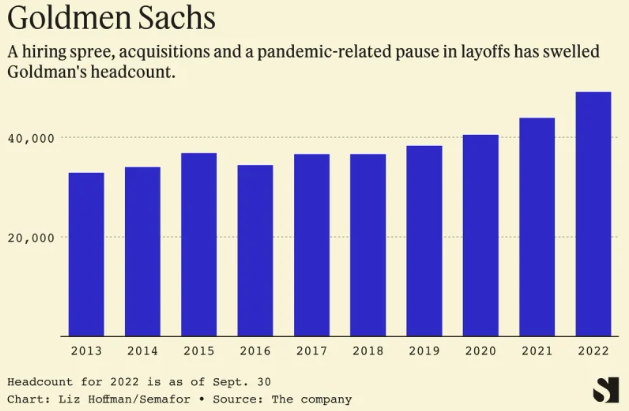

Make no question about it – despite what the “data” shows and what the Fed says – the job market is, in fact, softening.

We’ve spent the last two weeks writing about how Wall Street firms are going to be cutting their bonus pools significantly, with higher rates throwing a wet blanket over dealmaking and earnings for many firms.

Now, it looks as though the layoffs on Wall Street are hitting high gear. Not one to be last or least decisive to act, Goldman Sachs announced this week that it is going to lay off as many as 4,000 of its employees, according to Semafor and Reuters on Friday morning.

Other Wall Street firms like Citigroup have also announced some cutbacks in staffing, but none as meaningful as Goldman’s cuts. The company’s managers are being “asked to identify low performers for what could be a cut of up to 8% to its workforce early next year”, the Semafor report said this morning.

The move is meaningful even when compared to Goldman’s usual lightening of its workforce, which includes between 2% and 5% of employees either being laid off or receiving no bonuses as part of efforts to trim the business.

Reuters reported Friday morning that Goldman’s headcount, even after the layoffs, will still remain above pre-pandemic levels.

Goldman didn’t partake in its routine cuts in 2020 and 2021 due to the pandemic – and then the ensuing boom that followed.

“…the firm has clearly overspent and over-hired, acting more like a tech company being cheered on by venture capitalists than a Wall Street bank bearing the scars of past crises of overexuberance. [CEO David] Solomon is now moving to stem those losses,” wrote Semafor’s Liz Hoffman.

Recall, just days ago we noted that Goldman was curtailing originating unsecured consumer loans. The move marks a noticeable pivot from the bank’s previous plans of trying to get closer to retail banking, which they were doing through their Marcus offering, which provided services like personal loans and high yield savings, similar to combining the features of lenders like Sofi and Upstart with the savings products from companies like Capital One.

But that experiment looks to be on its last legs. Goldman hasn’t officially commented on the report yet but the bank has been in the midst of cost cutting measures for several months. As we noted then, Goldman was one of the first banks to announce layoffs this season.

Recall, in 2018, we explained how Goldman Sachs had switched from betting against Subprime (Residential Mortgage Backed Securities and their various synthetic and “squared” derivatives) to betting with Subprime (hoping to profit off America’s sub-660 FICO population by lending to it).

The Economist has interviewed the three Ukrainian leaders who manage the war in Ukraine. It summarizes them in an interpretive writeup. I will use that to extract the important points.

The writeup is of course full of propaganda but one can still glean some information from it.

The first interview (transcript) was with Volodymyr Zelensky, Ukraine’s president, who is saying nothing new that would be of interest:

“People do not want to compromise on territory,” he says, warning that allowing the conflict to be “frozen” with any Ukrainian land in Russian hands would simply embolden Mr Putin. “And that is why it is very important…to go to our borders from 1991.”

Zelensky wants Crimea back. Good luck achieving that impossibility one might say.

The second interview is with General Valery Zaluzhny, Commander-in-Chief of the Armed Forces of Ukraine. The third interview is with Colonel-General Oleksandr Syrsky, the head of Ukraine’s ground forces.

All three men emphasised that the outcome of the war hinges on the next few months. They are convinced that Russia is readying another big offensive, to begin as soon as January.

The author writes that “Ukraine enjoyed a triumphant autumn.” One wonders how many thousand Ukrainian soldiers have died for that triumph that was in reality a well controlled Russian retreat to shorten its frontlines.

But neither General Zaluzhny nor General Syrsky sounds triumphant. One reason is the escalating air war. Russia has been pounding Ukraine’s power stations and grid with drones and missiles almost every week since October, causing long and frequent blackouts. Though Russia is running short of precision-guided missiles, in recent weeks it is thought to have offered Iran fighter jets and helicopters in exchange for thousands of drones and, perhaps, ballistic missiles.

“It seems to me we are on the edge,” warns General Zaluzhny. More big attacks could completely disable the grid. “That is when soldiers’ wives and children start freezing,” he says. “What kind of mood will the fighters be in? Without water, light and heat, can we talk about preparing reserves to keep fighting?”

When it is cold and dark morale indeed becomes a problem. It is not the only one.

A second challenge is the fighting currently under way in Donbas, most notably around the town of Bakhmut. General Syrsky, who arrives at the interview in eastern Ukraine in fatigues, his face puffy from sleep deprivation, says that Russia’s tactics there have changed under the command of Sergei Surovikin, who took charge in October. The Wagner group, a mercenary outfit that is better equipped than Russia’s regular army, fights in the first echelon. Troops from the Russian republic of Chechnya and other regulars are in the rear. But whereas these forces once fought separately, today they co-operate in detachments of 900 soldiers or more, moving largely on foot.

Bakhmut is not an especially strategic location. Although it lies on the road to Slovyansk and Kramatorsk, two biggish cities (see map), Ukraine has several more defensive lines to fall back on in that direction. What is more, Russia lacks the manpower to exploit a breakthrough. The point of its relentless onslaught on Bakhmut, the generals believe, is to pin down or “fix” Ukrainian units so that they cannot be used to bolster offensives in Luhansk province to the north. “Now the enemy is trying to seize the initiative from us,” says General Syrsky. “He is trying to force us to go completely on the defensive.”

If Bakhmut is not a strategic location why is the Ukrainian army sending more and more troops into it? Russia is using Bakhmut not only to “fix” Ukrainian units. It is using it to eliminate them with up to 500 Ukrainian soldiers killed or wounded per day. The real fixing operation is happening elsewhere.

Ukraine also faces a renewed threat from Belarus, which began big military exercises in the summer and more recently updated its draft register. On December 3rd Sergei Shoigu, Russia’s defence minister, visited Minsk, the Belarusian capital, to discuss military co-operation. Western officials say that Belarus has probably given too much material support to Russian units to enter the fray itself, but the aim of this activity is probably to fix Ukrainian forces in the north, in case Kyiv is attacked again, and so prevent them from being used in any new offensive.

General Zaluzhny has a quite realistic view on what is coming:

“Russian mobilisation has worked,” says General Zaluzhny. “A tsar tells them to go to war, and they go to war.” General Syrsky agrees: “The enemy shouldn’t be discounted. They are not weak…and they have very great potential in terms of manpower.” He gives the example of how Russian recruits, equipped only with small arms, successfully slowed down Ukrainian attacks in Kreminna and Svatove in Luhansk province—though the autumn mud helped. Mobilisation has also allowed Russia to rotate its forces on and off the front lines more frequently, he says, allowing them to rest and recuperate. “In this regard, they have an advantage.”

But the main reason Russia has dragooned so many young men, the generals believe, is to go back on the offensive for the first time since its bid to overrun Donbas fizzled out in the summer. “Just as in [the second world war]…somewhere beyond the Urals they are preparing new resources,” says General Zaluzhny, referring to the Soviet decision to move the defence industry east, beyond the range of Nazi bombers. “They are 100% being prepared.” A major Russian attack could come “in February, at best in March and at worst at the end of January”, he says. And it could come anywhere, he warns: in Donbas, where Mr Putin is eager to capture the remainder of Donetsk province; in the south, towards the city of Dnipro; even towards Kyiv itself. In fact a fresh assault on the capital is inevitable, he reckons: “I have no doubt they will have another go at Kyiv.”

The general is building and holding back reserves which is problematic for the front lines:

The temptation is to send in reserves. A wiser strategy is to hold them back. … “May the soldiers in the trenches forgive me,” says General Zaluzhny. “It’s more important to focus on the accumulation of resources right now for the more protracted and heavier battles that may begin next year.”

Ukraine has enough men under arms—more than 700,000 in uniform, in one form or another, of whom more than 200,000 are trained for combat. But materiel is in short supply. Ammunition is crucial, says General Syrsky. “Artillery plays a decisive role in this war,” he notes. “Therefore, everything really depends on the amount of supplies, and this determines the success of the battle in many cases.” General Zaluzhny, who is raising a new army corps, reels off a wishlist. “I know that I can beat this enemy,” he says. “But I need resources. I need 300 tanks, 600-700 IFVs [infantry fighting vehicles], 500 Howitzers.” The incremental arsenal he is seeking is bigger than the total armoured forces of most European armies.

Does Zaluzhny really believe that he could get that force? I don’t think so.

The Economist points out that donors of weapons have run out of pretty much everything:

On December 6th America’s Congress agreed in principle to let the Pentagon buy 864,000 rounds of 155mm artillery shells, more than 12,000 GPS-guided Excalibur shells and 106,000 GPS-guided GMLRS rockets for HIMARS—theoretically enough to sustain Ukraine’s most intense rate of fire for five months non-stop. But this will be produced over a number of years, not in time for a spring offensive.

Russia has similar problems. It will run out of “fully serviceable” munitions early next year, says an American official, forcing it to use badly maintained stocks and suppliers like North Korea. Its shell shortages are “critical”, said Admiral Tony Radakin, Britain’s defence chief, on September 14th.

The last part is of course as valid as the claim that Russia is ‘running out of missiles’.

But even while lacking armored forces and ammunition Ukraine still dreams of big attacks:

“With this kind of resource I can’t conduct new big operations, even though we are working on one right now,” says General Zaluzhny.

The writer discusses various options where Ukraine could attack but finds that it does not really have a good one. The big victory over Russia will not be coming:

In private, however, Ukrainian and Western officials admit there may be other outcomes. “We can and should take a lot more territory,” General Zaluzhny insists. But he obliquely acknowledges the possibility that Russian advances might prove stronger than expected, or Ukrainian ones weaker, by saying, “It is not yet time to appeal to Ukrainian soldiers in the way that Mannerheim appealed to Finnish soldiers.” He is referring to a speech which Finland’s top general delivered to troops in 1940 after a harsh peace deal which ceded land to the Soviet Union.

So how many soldiers will still have to die before Zaluzhny is willing to give his Mannerheim speech (vid)? He does not say.

He will probably have to hold his speech sooner than he thinks because the Ukrainian economy has broken down. GDP decreased by 33% this year and, as attacks on the electrical net continue, it will shrink by another 5 or 10% next year. Inflation is above 20%, unemployment above 30%. The big metal and mining industries had to shut down as they depend on uninterrupted electricity supplies. Meanwhile donors are unwilling to hand to Ukraine the budget it claims to need.

It seems possible that the pending bankruptcy of Ukraine may indeed end the war earlier than any military action.

Xi Jinping’s Visit to Saudi Arabia and the overthrow of Atlanticism

The historic China-Arab Summit currently underway in Riyadh symbolizes the emerging Eurasianism in the Persian Gulf.

As Atlanticists continue their commitment to a future shaped by energy scarcity, food scarcity, and war with their nuclear-capable neighbors, most states in the Persian Gulf that have long been trusted allies of the west have quickly come to realize that their interests are best assured by cooperating with Eurasian states like China and Russia who don’t think in those zero-sum terms.

With Chinese President Xi Jinping’s long-awaited three-day visit to Saudi Arabia, a powerful shift by the Persian Gulf’s most strategic Arab state toward the multipolar alliance is being consolidated. Depending on which side of the ideological fence you sit on, this consolidation is being viewed closely with great hope or rage.

Xi’s visit stands in stark contrast to US President Joe Biden’s underwhelming ‘fist bump’ meeting this summer, which saw the self-professed leader of the free world falling asleep at a conference table and demanding more Saudi oil production while offering nothing durable in return.

In contrast, Xi’s arrival was greeted by a multi-cannon salute and Saudi jets painting the red and yellow colors of China’s flag in the skies over Riyadh. Beijing’s delegation of political and business elites, in the following days, will continue to meet with Saudi counterparts to strike long-term strategic deals in cultural, economic and scientific domains.

The visit will culminate in the first ever China-Arab Summit on Friday, 9 December, where Xi will meet with 30 heads of state. The Chinese foreign ministry described this as “an epoch-making milestone in the history of the development of China-Arab relations.”

While $30 billion in deals will be signed between Beijing and Riyadh, something much bigger is at play which too few have come to properly appreciate.

Riyadh’s steps toward the BRI since 2016

Xi Jinping last visited the kingdom in 2016, to advance Riyadh’s participation in China’s newly unveiled Belt and Road Initiative (BRI). A January 2016 policy report by the Chinese government to all Arab states reads:

“In the process of jointly pursuing the Silk Road Economic Belt and the 21st Century Maritime Silk Road initiative, China is willing to coordinate development strategies with Arab states, put into play each other’s advantages and potentials, promote international production capacity cooperation and enhance cooperation in the fields of infrastructure construction, trade and investment facilitation, nuclear power, space satellite, new energy, agriculture and finance, so as to achieve common progress and development and benefit our two peoples.”

It was only three months later that Crown Prince Mohammed bin Salman (MbS) inaugurated Saudi Vision 2030 which firmly outlined a new foreign policy agenda much more compatible with China’s “peaceful development” spirit.

After decades serving as an Atlanticist client state with no viable manufacturing prospects or autonomy beyond its role in supporting western-managed terror operations, Saudi Vision 2030 demonstrated the first signs of creative thinking in years, with an outlook toward a post-oil age.

On the energy front, China Energy Corp is building a sprawling 2.6 GW solar power station in Saudi Arabia, and Chinese nuclear developers are helping Riyadh develop its vast uranium resources while also mastering all branches of the nuclear fuel cycle.

In 2016, both nations signed an MoU to build fourth generation gas-cooled nuclear reactors. This follows the UAE’s recent leap into the 21st century with 2.7 GW of energy now constructed.

By early 2017, Riyadh had firmly bought its ticket on the New Silk Road with a $65 billion agreement integrating the Saudi Vision 2030 and BRI with a focus on petrochemical integration, engineering, refining, procurement, construction, carbon capture, and upstream/downstream development.

In the new post-American epoch, signs of this spirit of cooperation and bridge building have increasingly come to be felt, even while its effects have been forcibly restrained – as millions of Yemenis suffering under seven years of war can testify.

Unlike the Atlanticist fixation on Green New Deals which threaten to annihilate industry and farming, Riyadh’s post-oil outlook is much more synergistic with China’s idea of “sustained growth” that demands nuclear power, continued hydrocarbons, and robust agro-industrial development.

China’s trade with Saudi Arabia rose to $87.3 billion in 2021, which saw a 39 percent increase over 2020, while US-Saudi trade has collapsed from $76 billion in 2012 to only $29 billion in 2021.

Some of this Beijing-Riyadh trade may now be conducted in the Chinese Yuan, which will only undermine the US-Saudi relationship further.

In the first 10 months of 2022, China’s imports from Saudi Arabia were $57 billion and exports to the kingdom rose to $30.3 billion. China is additionally building 5G systems and cultivating a vast technology hub with a focus on selling electronic goods, all while helping Saudi Arabia build up an indigenous manufacturing sector.

A trend of Harmonization

Despite the continued chaos in Yemen, and economic devastation in Lebanon, Syria, and Iraq, Beijing’s subtle trend has nonetheless been one of healing with Saudi Arabia – and regional power Turkiye.

Saudi Arabia and Turkiye have often acted as rivals, and front two distinct foreign agendas with broad regional ambitions that overlap on many fronts. But despite this competitive past, higher necessities have induced both nations to harmonize their foreign policy outlooks with a new “look east” focus.

This was expressed during the Saudi crown prince’s visit to Ankara in June 2022 where the two heads of state called for “a new era of cooperation” with a focus on political, economic, military and cultural cooperation outlined in a joint communique.

Only days after MbS’s return from Turkiye, then-Iraqi Prime Minister Mustafa al-Kadhimi visited Jeddah to promote regional stability stating in a press release “they changed points of view on a number of issues that would contribute to supporting and strengthening regional security and stability.”

Iraq and Saudi Arabia had only re-established diplomatic ties in November 2020 due to Saddam Hussein’s invasion of Kuwait 30 years earlier.

Between 2021-2022, Iraq had worked hard to host bilateral talks between Saudi Arabia and Iran with five rounds of talks held and Kadhimi stating his belief that “reconciliation is near.” Tehran-Riyadh diplomatic ties were cut in the aftermath of the 2016 execution of outspoken Saudi Shiite cleric Nimr al-Nimr, prompting the storming of the Saudi embassy in Tehran by angry protestors.

In March 2022, MbS stated that Iran and Saudi Arabia “were neighbors forever” and stated that it is “better for both of us to working it out and to look for ways in which we can co-exist.”

By August 23, 2022, the UAE and Kuwait created a new milestone by restarting diplomatic relations with Iran. And although nearly every Persian Gulf state (plus Turkiye) had devoted years to supporting regime change in Syria, a new reality has imposed itself with all Arab parties veering toward the Chinese BRI model of regional integration and economic development.

The Key Role of Iran

Not only is Iran a key player in the Greater Eurasian Partnership serving as a strategic hub for the southern route of China’s BRI, but it is also a keystone of the Russia-Iran-India-led International North South Transportation Corridor (INSTC) which has become a major force synergizing with the BRI.

Iraq and Iran themselves are in the final stages of building the long-awaited Shalamcheh-Basra railway which will unite the two nations by rail for the first time in decades while also offering a potential extension to the already existent 1500 km railway through Iraq to Syria’s border.

The climate for cooperation was undoubtedly made possible by the presence of Chinese economic diplomacy which established a 25 year, $400 billion energy and security deal with Iran – but also Russia, whose similar but smaller $25 billion, twenty-year deal with Tehran may easily expand to $40 billion in Russian investments in Iran’s vast oil and natural gas fields in the coming years.

Saudi Arabia and Russia’s relationship with OPEC+ demonstrated its potency this summer when Riyadh won the ire of Washington by not only denying Biden’s requests for increased oil production, but cutting overall oil production and driving up global prices of oil. Saudi Arabia benefited by vastly increased imports of discounted Russian oil which were then sold to a desperate Europe.

Furthermore, Saudi plans to join the global hub of multipolarity itself, BRICS+ (alongside Turkiye, Egypt, and Algeria), in addition to recently becoming a full-fledged Shanghai Cooperation Organization (SCO) dialogue partner, have placed its destiny ever deeper into the growing Multipolar Alliance.

With the increased potential for stability and harmonization of interests across various power blocs, an atmosphere more conducive to long-term economic investments is finally presenting itself to Chinese investors who had long looked upon conflict-ridden West Asia with justifiable trepidation.

In August 2022, the Saudi state oil company Aramco and China’s Petroleum and Chemical Corporation Ltd signed an MOU expanding on the aforementioned $65 billion cooperation deal of 2017, which involves the construction of Fujian Refining and Petrochemical Company (FREP) and Sinopec Senmei Petroleum Company (SSPC) in Fujian, China, and Yanbu Aramco Sinopec Refining Company (YASREF) in Saudi Arabia.

Rail and interconnectivity

Perhaps most exciting are prospects for interconnectivity that play directly into the development corridors tied to the BRI. In Saudi Arabia, this train has moved steadily apace with the 450 km high speed Haramain Railway built by China Railway Construction Company connecting Mecca to Medina completed in 2018.

Photo Credit: The Cradle

Discussions are well underway to extend this line to the 2400 km North South Railway from Riyadh to Al Haditha completed in 2015. Meanwhile, 460 km of rail connecting all Gulf Cooperation Council (GCC) members is currently under construction, which is driving reforms in engineering, trade schools, and manufacturing hubs across the Arabian Peninsula.

In 2021, all GCC states gave their full support to a $200 billion Persian Gulf-Red Sea high speed railway dubbed “The Saudi Landbridge,” which also dovetails another $500 billion megaproject with vast Chinese investments, dubbed the futuristic NEOM mega-city on the Red Sea.

The Eurasianists stand to gain

It can only be hoped that this new chemistry of harmonization and win-win cooperation may soon provide a key to ending the fires of conflict in Yemen and other regional states.

Further, with Russia and China both helping to broker diplomatic backchannels, and with Iran playing an active role within this process, perhaps negotiations for reconstruction can begin in this war-torn zone of conflict.

It is not an extreme stretch of the imagination to see the new Persian Gulf-Red Sea rail project extending north into Egypt and south into Yemen.

Looking at a map of the region, one can imagine the reactivation of the “Bridge of the Horn of Africa” first unveiled in 2009, that would have extended rail across the 25 km Bab el Mandeb strait connecting pipelines and rail lines into Djibouti and East Africa, more broadly.

While a western-manipulated Arab Spring derailed that concept in 2011, and the Saudi war against Yemen drove it further under ground since 2015, perhaps this new spirit of inter-civilizational cooperation under a new economic architecture liberated from the Atlanticist-dominated dollar system may provide just what it takes to revive the idea once again.

For the first time, a gunfire erupted directly between Russian mercenaries (PMC Wagner) and NATO mercenaries (American PMC Mozart) who were on patrol in Bakhmut. Suddenly they came across a group of Russian soldiers in a heavily fortified trench system supported by T-90 tanks.

Russian media sources on December 8, 2022, indicating a full confrontation was recorded in the outskirts of the city, instead of strengthening the Ukrainian defenses PMC Mozart troops were ambushed and made the choice to withdraw in armed clashes.

EU crude imports from Russia are set to plunge after the import ban of seaborne crude oil on December 5th.

Oil production growth in the U.S. is flattening for a number of reasons.

U.S. crude exports to the EU can only replace a small portion of Russian/OPEC crude.

OPEC+ yesterday decided to leave its production quotas where they are, at 2 million bpd lower than they were in October, which is an effective cut of 1 million bpd of production. Three days earlier, the European Union reached an agreement to set a price cap on Russian crude oil at $60 per barrel—lower than market prices but not as low as some EU members, such as Poland and Estonia, would have liked the cap to be.

Russia responded by reiterating that it will not sell oil to countries enforcing a price cap. According to Reuters, a decree to that effect is already being prepared.

Amid all this, U.S. oil production growth is slowing down. The shale revolution, as we knew it until a few years ago, is no longer in full-growth mode. And it may never return to it.

On the face of it, all looks good. U.S. output has rebounded from a low of 9.7 million bpd, which was recorded in May 2020, to 12.3 million bpd this September, Reuters’ John Kemp wrote last week, noting that this year’s high was still below the pre-pandemic record of 13 million bpd, hit in late 2019.

What’s more, oil production in the country was not rising steadily. For two of the last seven months, it has actually declined, according to EIA data. And the rate of growth when it grew was half the growth rate recorded during the boom years in U.S. shale.

There are numerous reasons for this slowdown, driven, like output growth, by the shale patch. In many parts of the patch, for instance, drillers are running out of so-called sweet spots—low-cost acreage that has driven much of the shale boom.

Yet oil companies are also rearranging their priorities under an administration that is much less favorable to their industry than previous ones. Returning cash to shareholders has become priority number one, replacing production growth.

There have also been lingering problems from the pandemic lockdowns, such as shortages of things like frac sand and steel tubing, as well as a labor shortage. On top of all that, the industry has had to deal with the same inflation that has hit all other industries, pushing costs up by some 20 percent.

All this means that as it curbs its own supply of Russian oil with the price cap and its oil embargo on the commodity, the European Union cannot really rely on higher oil imports from the United States as it has relied on stronger gas imports.

The outlook is not very encouraging, either. According to a Reuters report from last week, spending in the shale oil industry in the U.S. is far from what it was during the boom years.

The report cited numbers for research and engineering spending at Schlumberger, for instance, now renamed SLB, which fell to 2.3 percent of revenues in the nine months to September.

It also said another large player in the industry, Helmerich & Payne, only planned to increase its R&D spend by $1 million for next year this year’s level, and cited Morgan Stanley analysts as saying that spending on new production was “modest at best”.

“Shale can’t come back to become a swing producer,” said the former head of Parsley Energy, Bryan Sheffield, echoing a very similar statement by Hess Corp.’s John Hess that he made last month.

“Shale was thought of as a swing producer, the Saudis and the OPEC have waited this out. Now, really OPEC is back in the driver’s seat where they are the swing producer,” Hess said at an investor conference.

He was quoted in a Reuters report that also cited other industry executives complaining about lower-than-expected well productivity and a substantially revised production growth forecast for 2021 by the EIA.

Hess went even further, warning that some companies in the shale patch only had a decade or so of life left in them and that “A lot of companies have already hit the wall,” missing their production and investment targets.

Meanwhile, the EU has become the biggest export market for U.S. crude oil, taking in more than Asia since the start of the year, Bloomberg reported in July, in a repeat of the redirection of natural gas flows.

But with U.S. oil output growth on the wane, if OPEC is back in the driving seat, that’s even worse news for Europe than the production growth slowdown in the United States. OPEC has signaled repeatedly in recent months that it has its own agenda, and it is not the same as the EU’s agenda.

On the contrary, the two agendas are very much at odds with the EU’s transition plans and OPEC’s plans to continue marketing hydrocarbons for as long as possible. In the immediate term, however, the two groups’ interests are aligned: the EU will need more oil from OPEC, and OPEC will probably be only too happy to supply it. At market prices, of course.

{kind=link}

{kind=link}