Goldman:

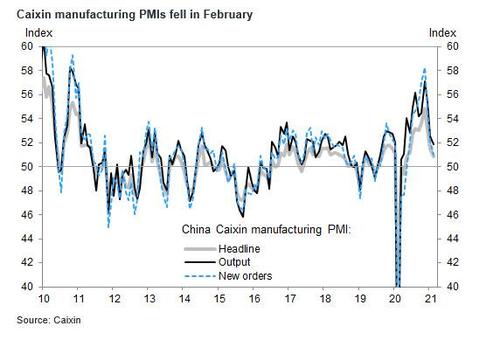

China’s Caixin manufacturing PMI fell to 50.9 in February from 51.5 in January, though still in expansionary territory. Most sub-indexes implied growth momentum moderated in the manufacturing sector. The production sub-index dropped to 51.9 in February from 52.5, and the new orders sub-index fell to 51.0 from 52.2. The new export order sub-index edged up only marginally to 47.5 from 47.4, still below 50 due to the resurgence of COVID-19 infections globally as highlighted by surveyed companies.

Surveyed companies remained cautious in hiring and the employment sub-index fell slightly to 48.1 from 49.6 in January. The raw materials inventory sub-index rose by 0.6pp to 48.8, but the finished goods inventory index edged down to 50.3 from 51.0. Stock shortages and travel restrictions continued to affect suppliers’ delivery in February. Price indicators suggest inflationary pressures moderated slightly but remained relatively high due to rising raw material prices and transportation costs according to the survey. The input price index fell slightly to 58.1 from 58.9 in January, and the output price index was 53.5, moderating from 54.9 in January. On future output, surveyed companies remained optimistic and expect “rising client demand globally once the pandemic comes to an end and planned product releases make debut”.

If that wasn’t enough, a former finance minister warned fiscal risks remain “extremely severe with risks and challenges”, with low revenue for five years ahead and no prospect of any spending cuts ahead, suggesting policy may need to be tightened at some point

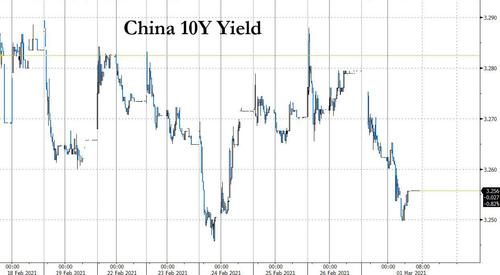

In kneejerk response, China’s 10-year government bond futures closed 0.3% higher, the most since Dec. 22, while In the cash bond market, the yield on 10-year sovereign notes dropped 2 bps to 3.26%, having barely budged in the past week and completely oblivious to the turmoil gripping the rest of the global bond market.

Investing in Chinese Stocks sees problems in Red Ponzi real estate: http://investinginchinesestocks.blogspot.com/

Very early, initial signal of a possible reversal in real estate: the 3x Bearish Real Estate ETF (DRV) broke its downtrend. Some other charts that look interesting in the real estate space. Some are failing at their initial pandemic gaps, some look relatively weak and could be starting meaningful breakdowns if they lose support (assuming a larger bearish move is underway in the market), while others are near pre-pandemic highs.

Check out some “playa”s:

“Investors may think the economic recovery in China has become less strong than expected, which could stoke risk-off sentiment in the short run and help bonds,” said Hao Zhou, senior emerging markets economist at Commerzbank AG in Singapore.

China’s economy is now fading and its credit impulse is set to shrink rapidly.

Not only will this affect reflation assets but also push yields lower. However, thanks to the 6-12 month diffusion lag of China’s credit impulse, we first have about 9 more months of higher yields and commodity prices before the hangover finally arrives.

{kind=link}