“This Is The Sharpest Turn In The Housing Market Since The 2008 Crash” As Mortgage Rates Soar Above 6%

THURSDAY, SEP 15, 2022 – 11:40 AM

And the hits just keep on coming for the US housing sector.

Three months after hitting the highest level in 14 years, on Thursday mortgage rates hit a fresh post-financial crisis high when they topped 6%, a jolt to home buyers who last year were paying less than half that.

The latest mortgage lender survey by Freddie Mac found that the average rate on a 30-year fixed mortgage climbed to 6.02% this week, up from 5.89% last week and 2.86% a year ago. The last time rates were this high was in the heart of the financial crisis in November 2008, when the U.S. was deep in recession.

The jump in mortgage rates – a welcome development by the US central bank which now wants to unleash a crippling recession on the US economy – is one of the most pronounced effects of the Federal Reserve’s campaign to curb inflation by lifting the cost of borrowing for consumers and businesses and crush demand for all levered purchases.

Already, it has ushered in a sea change in the housing market by adding hundreds of dollars or more to the monthly cost of a potential buyer’s mortgage payment, slowing what was a red-hot market not so long ago. Higher rates are forcing some would-be buyers to continue renting. Since the start of the year, the average mortgage payment has risen 38.5% to $2,306 from around $1,700 at the start of the year.

Other buyers are skimping elsewhere to make their mortgage payments.

Rising mortgage costs have been among the largest factors hampering affordability in the housing market recently. While home prices and rents have risen swiftly this year, rising mortgage costs have tipped the scales in favor of renting for many Americans.

The swift reversal in rates this year has brought tough times to the mortgage industry. Originations topped $4.4 trillion last year, but are expected to drop to just over half that in 2022, according to forecasts by the Mortgage Bankers Association, a trade group. Refinancings in particular have slowed down because higher rates erode the benefit for most homeowners. Refinancing activity is down more than 80% from a year ago, MBA said. Just 452,000 homeowners would be good candidates for a refinancing that lowers their rate by at least 0.75 percentage point, according to an analysis by Black Knight Inc., a mortgage technology and data provider. That is down from a peak of over 19 million in late 2020.

As the WSJ reports, would-be buyers like Desi Duncker and Victoria Lauture Duncker are waiting for the market to settle down before moving ahead. They and their daughter moved from Manhattan to Bloomfield, N.J., last year and rented while he introduced his family to the area, where he grew up.

They would like to buy but have been derailed by higher mortgage rates, rising home prices and a decline in the value of their investments, including bitcoin, Mr. Duncker said. Stocks and cryptocurrencies are down sharply this year, slowed in part by the Fed’s higher rates.

“Every possible factor that could have gone against buyers since January has happened,” Duncker said. He keeps a Google Doc with notes about buying and in June began noting that mortgage costs were becoming a problem. They might look to rent an apartment near the train station for now. He commutes into New York City for his job in finance at a tech company.

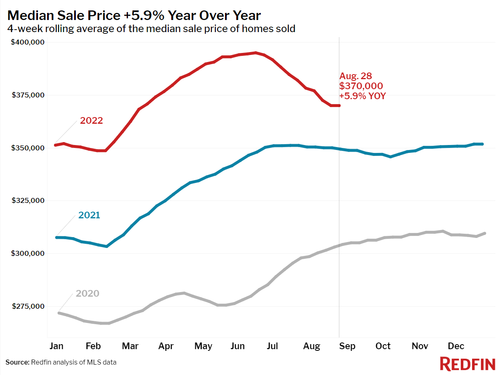

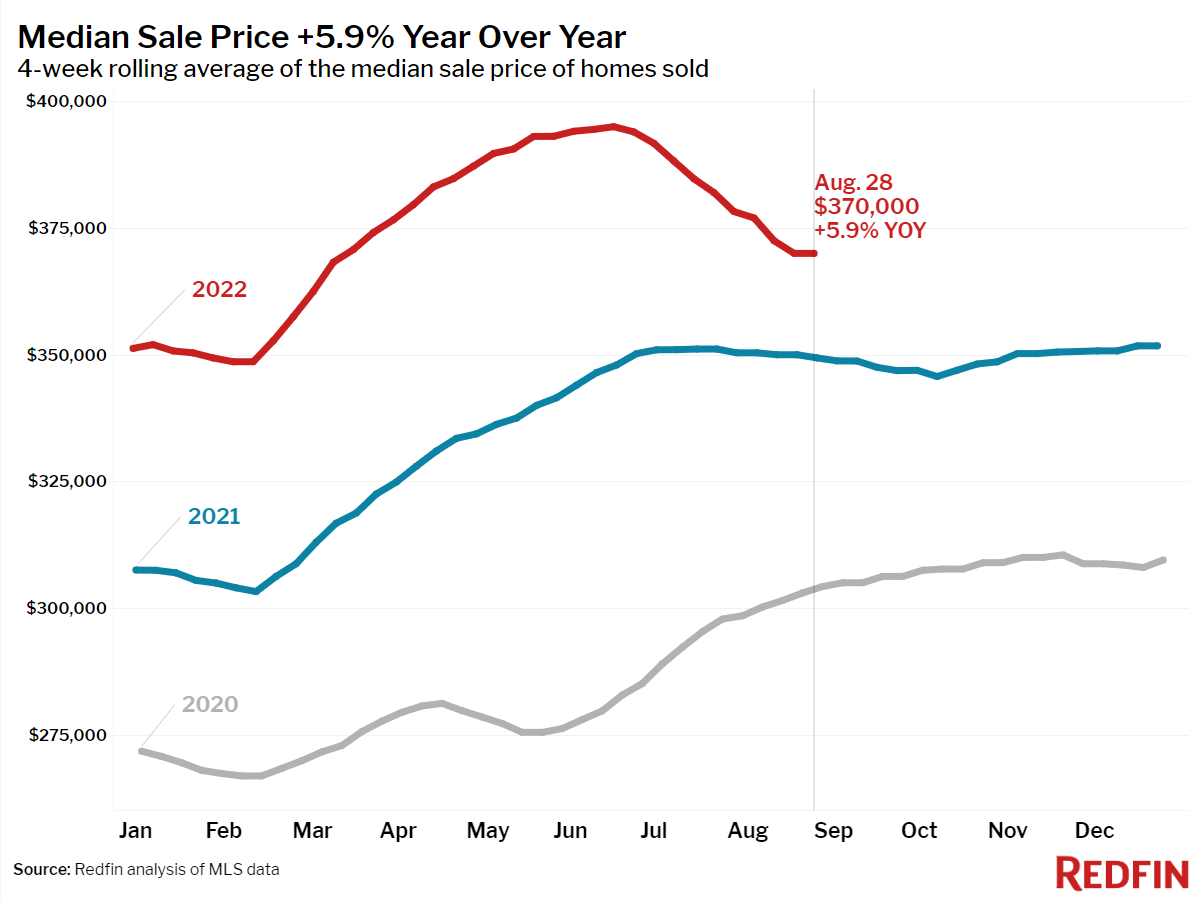

Meanwhile, despite the soaring mortgage rates, home prices continue to show large gains from a year ago, and as of July the median sales price for an existing was around $400,000 although it has dropped sharply since. Existing-home sales fell for six straight months through July, and the pace of price growth has decelerated.

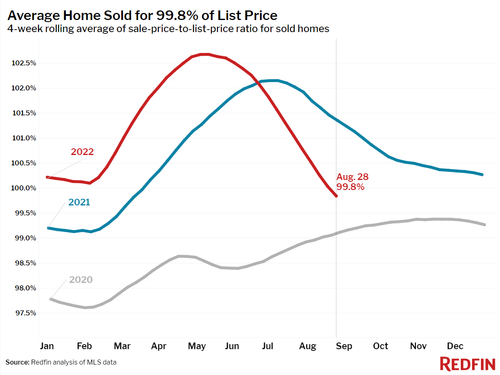

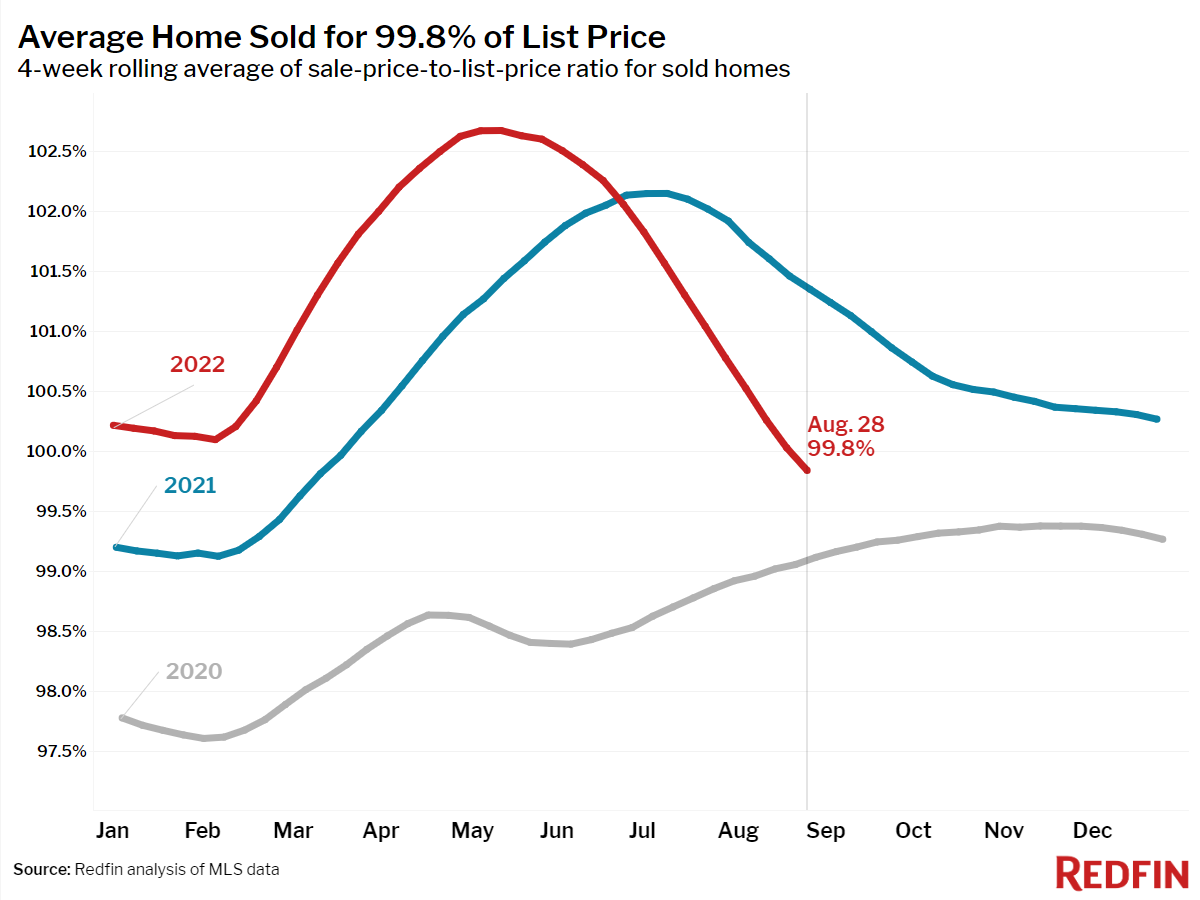

And signs are pointing to an even sharper slowdown: the good news – so to speak – is that the Fed’s dream of sparking a crash is about to come true: in the four weeks that ended Sept. 4, homes on average sold for 0.3% below their final list price, according to Redfin, a real-estate brokerage. For the year-and-a-half before that, homes were generally selling above list price. The firm also said that home-touring activity is down 38% from the beginning of the year.

“This is the sharpest turn in the housing market since the housing market crash in 2008,” said Daryl Fairweather, Redfin’s Chief Economist.

“We haven’t seen interest rates this high since 2008, 2007, so it is a big change from the housing market we’ve all gotten used to,” Fairweather said.

“Buyers just don’t have the 40% extra money to put towards housing every month,” Fairweather said. “A lot of homebuyers had to drop out and go to the rental market instead or choose not to buy that second home or investment property.” Redfin said larger cities like San Francisco and Los Angeles are seeing the greatest impacts from this.

“When you’re talking about a $1.5 million home, that’s an extra thousand dollars a month towards a mortgage payment.”

In New Orleans, the president of the Metropolitan Association of Relators David Favret said there’s more homes on the market in his area than in the last two years.

On the flip side, Redfin also said now is still a good time to buy if you qualify for a mortgage because you can always refinance when mortgage rates go back down.

“If you find a house that meets all your needs and you’re going to stay in it for at least 5 years, it’s still a great time to buy,” Fairweather said.

Finally, when asked if we could enter another housing financial crisis, Redfin – which is in the housing business after all – said it’s unlikely.

“People who own homes right now are in a good financial position generally,” Fairweather said. “The criteria for getting a mortgage is really high. It’s not like during the housing market crash when people were getting mortgages they had no business getting.”

Fairweather did say, however, that if we do enter another recession, homebuyers need to consider if they’ll still be able to afford their home if they unexpectedly lose their job. The answer here should be obvious, and is why we are about to see a housing crash that will match if not surpass the bursting of the first housing bubble.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Reblogged this on Calculus of Decay .

LikeLike