Is JPM Solvent? If not, what about Citi? Is anyone solvent?

An available-for-sale security (AFS) is a debt or equity security purchased with the intent of selling before it reaches maturity or holding it for a long period should it not have a maturity date.

Accounting standards require companies classify any investments in debt or equity securities when they are purchased in one of the following categories:

- held-to-maturity,

- held-for-trading, or

- available-for-sale.

Available-for-sale securities are reported at fair value; changes in value between accounting periods are included in accumulated other comprehensive income in the equity section of the balance sheet.

As interest rates have risen in response to Federal Reserve policies, the AFS securities have seen significant unrealized losses on their bond portfolios.

The change in bond portfolios has disrupted the bank M&A market and inflicted pressures on large commercial banks.

Generally accepted accounting principles (GAAP) require unrealized losses (or unrealized gain in a different environment) on AFS securities to be reflected on the balance sheet as accumulated other comprehensive income (AOCI).

AOCI losses have been dramatically rising over the past year.

Rising interest rate increases, coupled with soft loan demand and desire for yields, leave banks holding large investment portfolios.

These securities are often weighted down by longer maturities, which means significant, unrealized, losses. These unrealized losses have suppressed bank M&A activity.

The question is to what extent is the rising AOCI impacting large bank solvency.

Here’s R. Chris Whalen to run the numbers coming using the Q3 results: https://www.theinstitutionalriskanalyst.com/post/is-jpmorgan-chase-insolvent

********

Is JPMorgan Chase Insolvent?

November 28, 2022 | Watching the Buy Side Pivot Platoon rev up for a new surge of asset allocation into large cap bank stocks, we remind readers of The Institutional Risk Analyst that US depositories currently are not particularly cheap, in nominal or real terms. In fact, in a stressed scenario, the liabilities of banks exceed the value of the assets by over $1 trillion, the classic definition of insolvency.

Once you adjust reported book value for the asset price inflation & now deflation of the QE/QT roller coaster ride, it is fair to ask: Just where is the value? If we told you that the capitalization of the industry was negative by over $1 trillion at the end of Q2 2022, would you still buy bank stocks for your clients? Let’s have a look at industry paragon JPMorgan Chase (JPM) just for giggles, but first we’ll start off with the industry view.

At the end of Q2 2022, the US banking industry had $2.2 trillion in total capital. That is, book equity. But much of total capital is not tangible, which is why regulators use Tier 1 Capital as the base measure for solvency. The legal definition of Tier 1 Capital, which excludes many items we discuss below, is found at 12 CFR Part 324 of the federal banking regulations.

Specifically, the law:

“requires that several items be fully deducted from common equity tier 1 capital, such as goodwill, deferred tax assets (DTAs) that arise from net operating loss and tax credit carry-forwards, other intangible assets (except for mortgage servicing assets (MSAs)), certain DTAs arising from temporary differences (temporary difference DTAs), gains on sale of securitization exposures, and certain investments in another financial institution’s capital instruments. Additionally, management must adjust for unrealized gains or losses on certain cash flow hedges.”

12 CFR Part 324

Of note, when adopted in 2015, CFR Part 324 allowed all non-advanced approach institutions (aka “little banks”) to make a permanent, one-time opt-out election, enabling them to calculate regulatory capital without AOCI. At the time, accumulated other comprehensive income was a minor entry on bank balance sheets and income statements, minor as in the footnotes. In the age of QE, however, AOCI is now a much bigger deal, but still is dwarfed by how QE has caused unrealized losses on bank balance sheets.

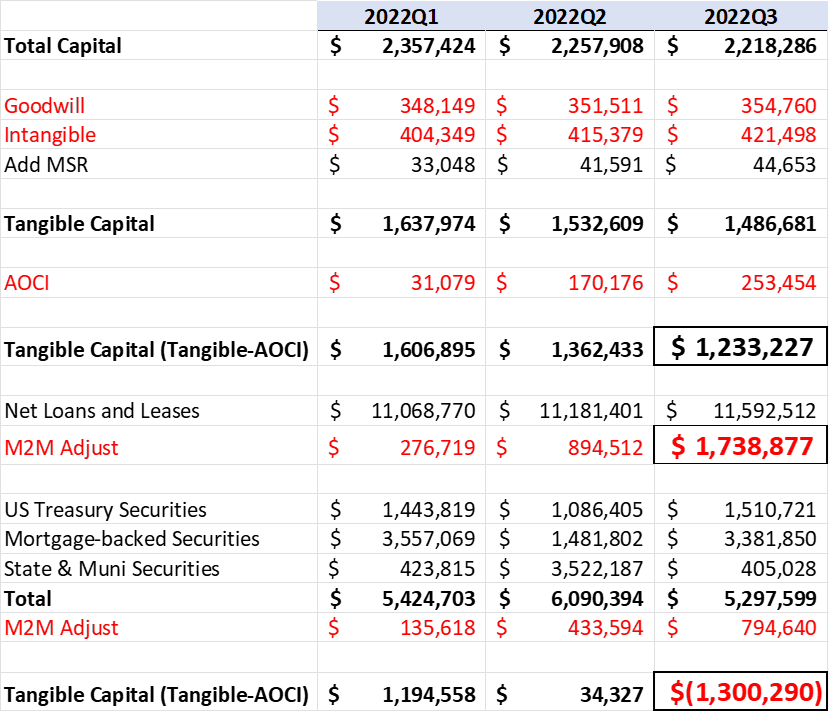

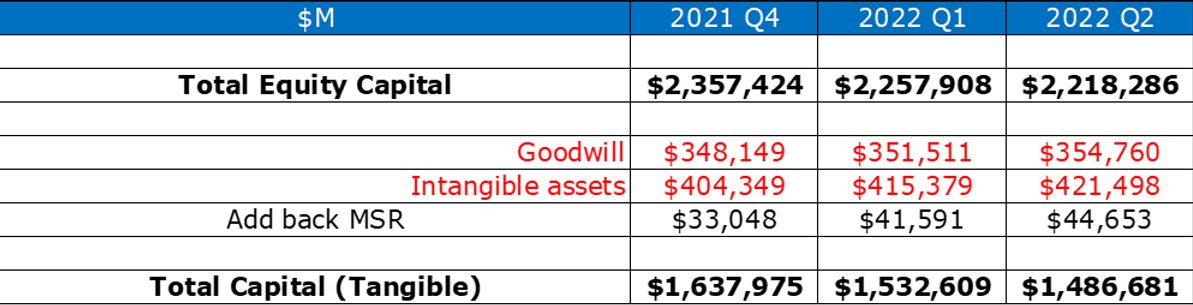

So, let’s begin the fun with the fire-sale calculation we perform using the aggregate data from the FDIC. We start with total capital, the broadest definition of bank equity. We then subtract the goodwill and all of the intangibles, but add back in the mortgage servicing assets just to be nice. Once you see the result of the analysis, you’ll understand why we say “nice” regards adding back the MSRs.

U.S. Banking Industry

Source: FDIC

Notice that tangible capital dropped by several hundred billion in three quarters since Q4 2021. As we’ve noted earlier, the large banks led by JPM plateaued in Q3 2022 in terms of AOCI, mostly through sales of assets and transfers into portfolio to be “held to maturity.” But the risk remains. MSR prices have likewise softened since June. Regulators refer to “assets” rather than rights because sometimes mortgage servicing can become a liability, particularly in the government market.

Thanks to QE and now QT, all sorts of assets have become negative return propositions for banks and nonbanks alike. If the coupon pays less than the funding costs, you’re losing money. Just ask Jerome Powell about the return on the Fed’s SOMA portfolio. Below we take the analysis through adding the net gain or loss reported in AOCI.

U.S. Banking Industry

Source: FDIC

So just subtracting the basics for Tier 1 capital leverage, including taking out the AOCI, we have almost cut Q2 2022 industry capital in half. And we have not even arrived at the fun part, which involves estimating the mark-to-market losses on loans and securities held in portfolio caused by the rapid increase in interest rates by the FOMC.

Even if the bank holds these low-coupon assets created during 2020-2021 in portfolio to maturity, cash flow losses and poor returns could eventually force a sale. This is why people who prattle on about how well capitalized are US banks are just showing their ignorance.

The table below shows our conservative M2M adjustment for the last three quarters on the almost $12 trillion in total loans and leases owned by banks. We adjust Q4 2021 by 2.5%, Q1 2022 by 8% of total loans and leases, and 15% of total loans and leases in Q2 2022 to approximate the low-end of M2M losses due to the rapid increase in interest rates in 2022.

U.S. Banking Industry

Source: FDIC

As you can see, the industry is already insolvent in Q2 2022 with the adjustment to the loan portfolio, which may be significantly underwater by next year. GAAP allows owners of assets held to maturity to ignore mark-to-market losses so long as they have the capacity and the intent to do so.

So, do you sell the 2% and 3% coupon loans and securities at a loss and buy some 8% and 9% loans coupons? Yes you do, eventually. This is how M2M becomes available for sale (AFS) “gradually, then suddenly” to recall Ernest Hemingway’s 1926 novel, The Sun Also Rises.

The final part of the analysis is to apply the adjustments above to the $5 trillion bank securities portfolio. The result is another $700 billion in potential M2M losses as of the end of Q2 2022 and a picture of the US banking industry that is a good bit less positive than the conventional wisdom.

U.S. Banking Industry

Source: FDIC

The value of the FDIC data is that they track all of the AOCI even if the banks do not need to add or subtract the balance from regulatory capital. The fact that the US banking industry had $1.3 trillion more in potential M2M losses that capital at Q2 2022 should put to rest any doubts that QE was too much funny money for too long. Notice that none of the economics reporters who cover the Fed ever ask about the impact of QE on the banking system.

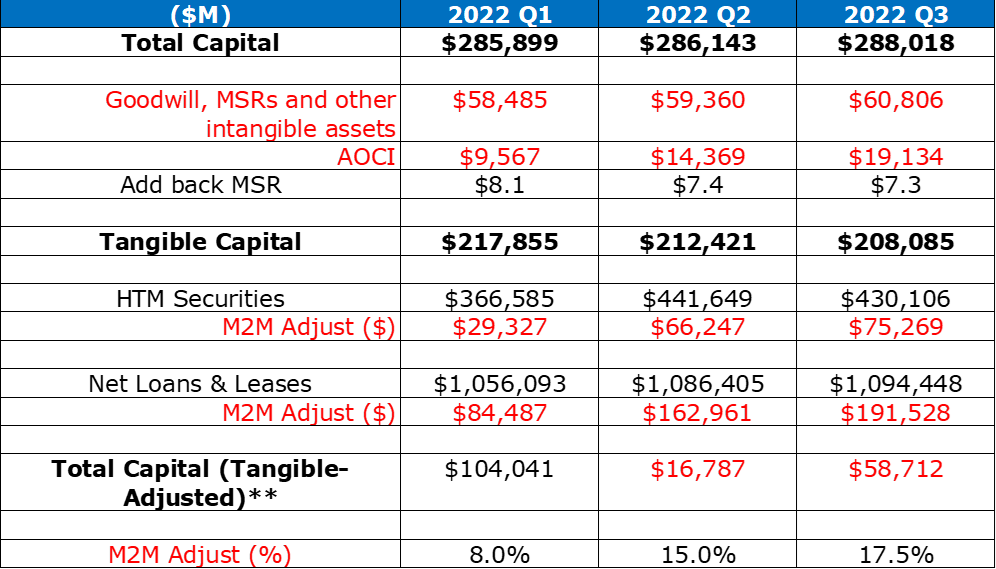

So now if we turn to JPM, which is one of the better managed banks in the US, the results are better than the industry as a whole but the bank still had a negative capital position at the end of Q2 2022 to the tune of -$16 billion in capital. The capital deficit increased to -$58 billion when we increased the M2M adjustment to 17.5% haircut in our stressed scenario.

JPMorgan Chase

Source: FDIC, Edgar

Don’t hold your breath waiting for Fed Chairman Jerome Powell to address the issue of bank solvency at the next FOMC press conference. First QE and now QT has injected such excessive levels of volatility into the prices of assets — all assets — that the value of capital has been compromised. Suffice to say that if the FOMC continues to raise interest rates above current levels, then we think that the issue of bank solvency may be front-and-center by next summer.

*****

They say the first rule of holes is if you find yourself in one, stop digging.

With that in mind, here’s Chris this morning regarding current TBA bids:

Reblogged this on Calculus of Decay .

LikeLike