NY Times: https://www.nytimes.com/2023/05/04/opinion/silicon-valley-bank-first-republic-financial-crisis.html

In an NY Times OpEd, Professor Amit Seru (Stanford) write: “A damaging combination of fast-rising interest rates, major changes in work patterns, and the potential of a recession could prompt a credit crunch not seen since the 2008 financial crisis.”

Could?

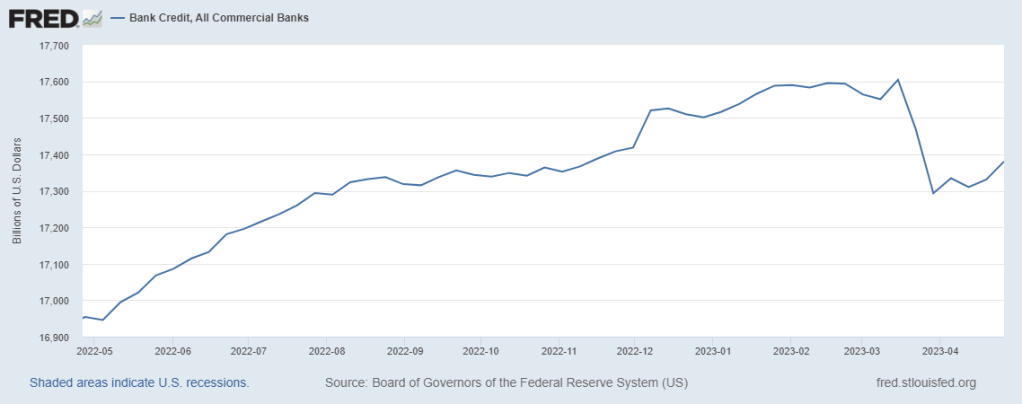

Well, we can see deposits draining over the past year.

Credit is down YoY

Professor Seru:

“Just in the past few months, Silicon Valley Bank, Signature Bank and First Republic Bank have failed. Their combined assets surpassed those held by the 25 banks (when adjusted for inflation) that collapsed at the height of the financial crisis. While some experts and policymakers believe that the resolution of First Republic Bank on Monday indicates the turbulence in the industry is coming to an end, I believe this may be premature. On Thursday, shares of PacWest and Western Alliance are falling as investors’ fears spread. Adverse conditions have significantly weakened the ability of many banks to withstand another credit shock — and it’s clear that a big one may already be on its way.

“Rapidly rising interest rates create perilous conditions for banks because of a basic principle: The longer the duration of an investment, the more sensitive it is to changes in interest rates. When interest rates rise, the assets that banks hold to generate a return on their investment fall in value. And because the banks’ liabilities — like its deposits, which customers can withdraw at any time — usually are shorter in duration, they fall by less. Thus, increases in interest rates can deplete a bank’s equity and risk leaving it with more liabilities than assets. So it’s no surprise that the US banking system’s market value of assets is around $2 trillion lower than suggested by their book value. When the entire set of approximately 4,800 banks in the United States is examined, the decline in the value of equity is most prominent for midsize and smaller banks, reflecting their heavier bets on long-term assets.“

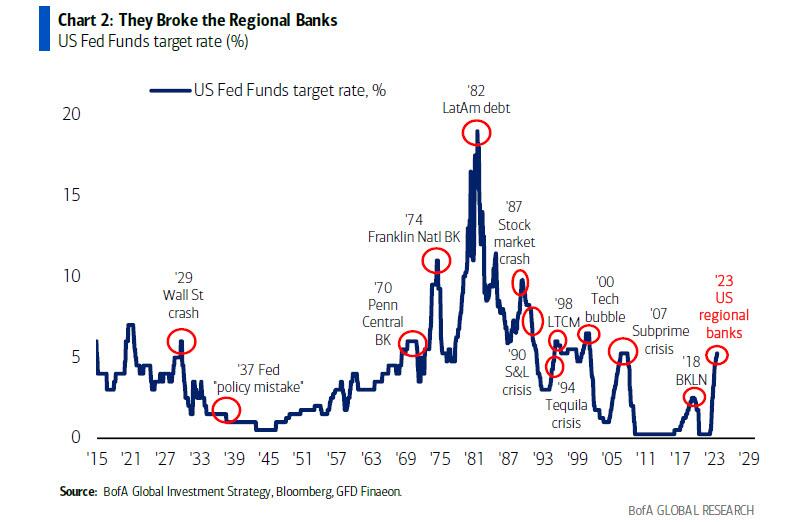

Here’s ZeroHedge:

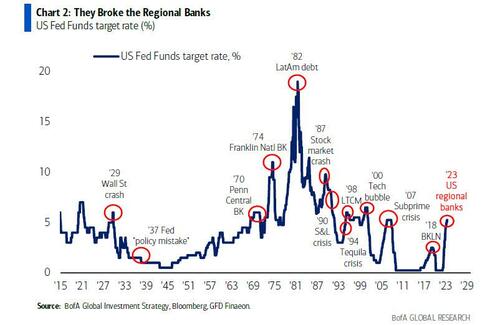

Our latest note, featuring BofA strategist Michael Hartnett highlights that “every Fed tightening cycle ends in crisis“, in this case US regional banks.

Finally, the apocalyptic warning about the US banking system comes as JPMorgan CEO Jamie Dimon claims that “the system is very, very sound.”

Are they?

NBER: https://www.nber.org/digest/20235/feds-monetary-tightening-and-risk-levels-us-banks

“Between March 7, 2022, and March 6, 2023, the Federal Reserve increased the federal funds rate by nearly 4.5 percentage points. This led to a $2.2 trillion aggregate decline in the market value of long-term bank assets such as government bonds, mortgages, and corporate loans. These decreases are not fully reflected in banks’ book values. In Monetary Tightening and US Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs? (NBER Working Paper 31048) Erica Xuewei Jiang, Gregor Matvos, Tomasz Piskorski, and Amit Seru show how such declines in asset values can increase bank insolvency risk due to runs by uninsured depositors, as illustrated most dramatically by the failure of Silicon Valley Bank (SVB).”

“The researchers collect data on bank asset holdings, including bond maturities, for all 4,844 FDIC-insured banks from their regulatory filings from the first quarter of 2022 onward. They estimate banks’ market values of assets by using data on traded indexes in real estate and US Treasury securities. They find that by the first quarter of 2023, the increase in interest rates had resulted in a 9 percent decline in the marked-to-market value of the median bank’s assets. The worst 5 percent of banks had declines of about 20 percent. These marked-to-market losses are similar in magnitude to the total book equity of the US banking system. Only about 6 percent of aggregate assets in the US banking system are hedged by interest rate swaps, too little to offset most of the market value losses.

“The researchers show that uninsured leverage, a bank’s uninsured debt-to-assets ratio, is the key to understanding whether these declines in asset values could lead to insolvency through “solvency runs.” Unlike insured depositors, uninsured depositors stand to lose a part of their deposits if their bank fails, potentially giving them incentives to run. If the insured depositors are sticky and are content with low deposit rates, a bank’s survival depends on market beliefs about the share of uninsured depositors who will withdraw their funds following a decline in the market value of bank assets. When interest rate increases and the associated decline in the market value of the banks’ assets are small, there is no risk of a run and banks can survive any withdrawals by the uninsured depositors. However, for larger increases in interest rates, there can be equilibrium outcomes in which uninsured depositors run and make banks insolvent. Banks with smaller initial capitalization and higher uninsured leverage are more likely to experience such outcomes, which increases their fragility to uninsured depositor runs. Such banks can remain solvent only if a relatively small share of the uninsured depositors is expected to withdraw; otherwise, there will be a run.”

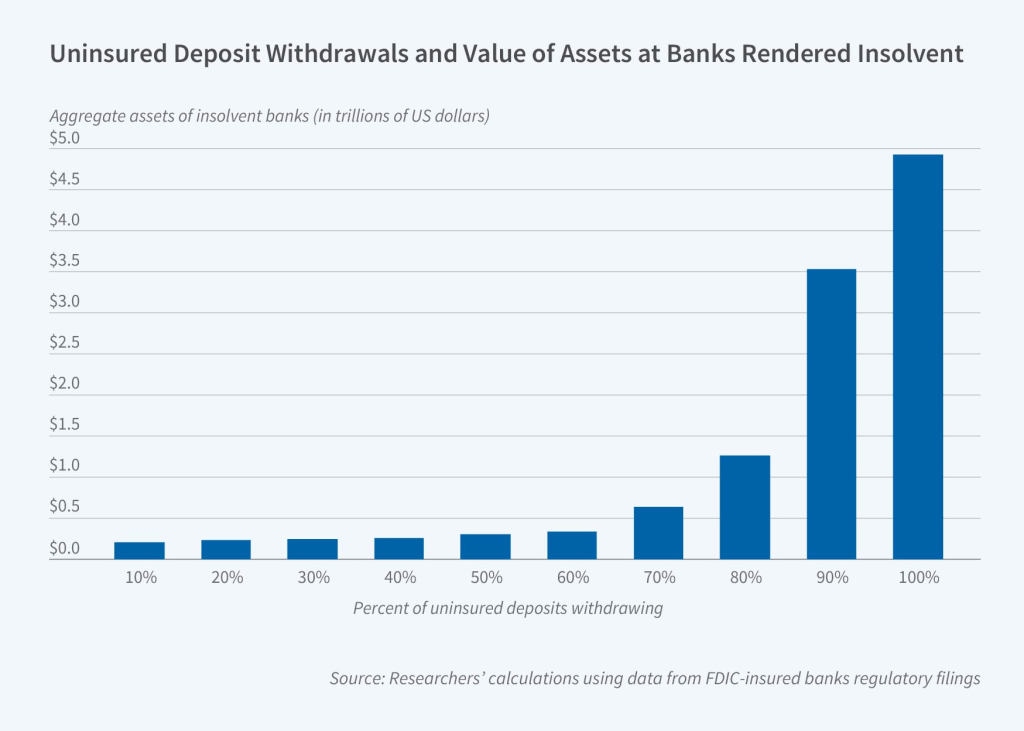

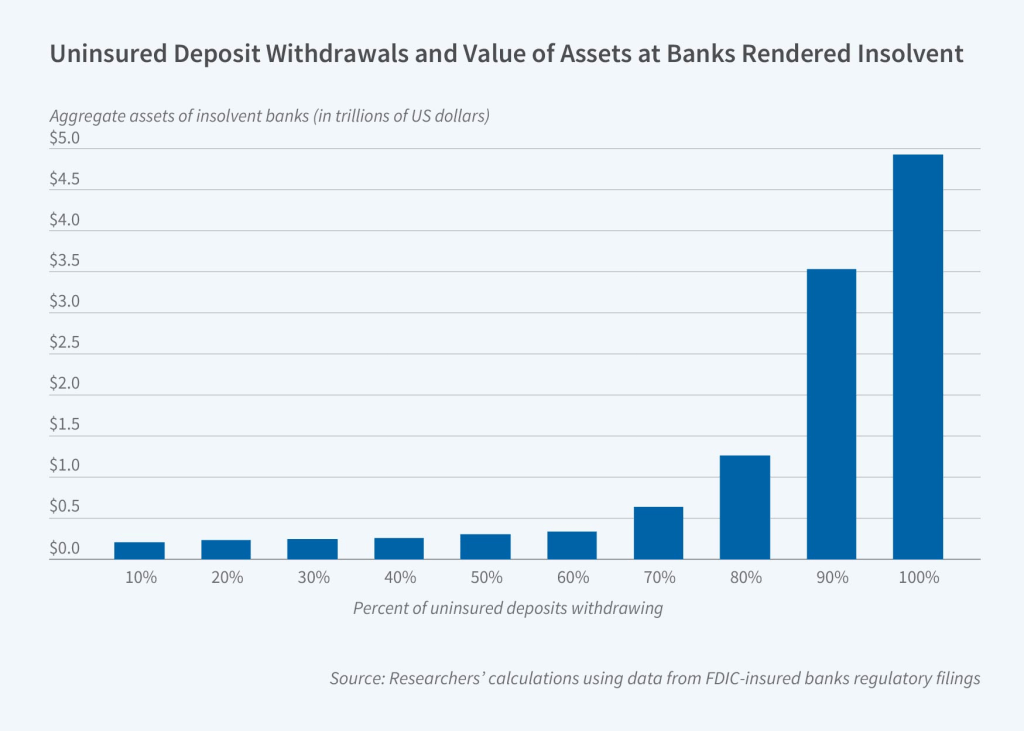

Uninsured deposits account for about half of all bank deposits and close to $9 trillion of aggregate bank funding. The researchers estimate banks’ vulnerability to self-fulfilling solvency runs across a wide range of possible beliefs regarding the share of uninsured depositors who may withdraw their money. Prior to the recent rise of interest rates, even if all uninsured depositors withdrew their money, the insured deposit coverage ratio for all banks would have been positive. Banks were not very vulnerable to uninsured depositor runs. After monetary tightening raised rates, however, withdrawal by half of uninsured depositors would turn into a self-fulfilling run for 186 banks with total assets of about $300 billion.

The researchers also study the geographical distribution of exposure to bank failure risk using data on the counties in which each bank has branches. They compute the share of deposits in each county that are held at banks that would not have sufficient mark-to-market assets to cover their deposits if half of their uninsured deposits were withdrawn. Counties with a greater share of residents from minority populations, with lower median income, and with a higher percentage of individuals without a college degree are more exposed to bank insolvency risk. Finally, the researchers show that a recent decline in banks’ asset values also eroded their ability to withstand adverse credit events — focusing on commercial real estate loans.

{kind=link}

One thought on “Are Banks Solvent?”