According to Reuters, Beijing now wants a full accounting of everything going on at local developers.

“The government is monitoring everything now, unless you want to cheat, but they will be able to tell from your monthly figures,” said a senior executive at one of the developers in the pilot scheme.

Following concerns of too much developer leverage sparked by Evergrande’s liquidity crisis, Chinese media reported that the cap for the debt-to-assets ratio will be set at 70%, the cap for net debt to equity will be set at 100% and the developers should also have enough cash to match their short-term liabilities. While authorities have yet to announcement details of the implementation, the industry expects the rules to be applied sector-wide in the first half of next year.

According to analysts at ANZ, about one-fifth of real estate companies with China A-shares have leverage ratios exceeding the thresholds. They warn that a sharp reduction in leverage “could rattle credit markets and weigh heavily on the property sector”, a key driver behind China’s swift economic recovery from the coronavirus crisis.

SocGen China analyst Wei Yao wrote that “a new chapter of deleveraging has begun”:

“A succession of events in the past few weeks have pushed the debt risk of China’s real estate sector to the forefront. Markets were at one point deeply concerned about the default risk of Evergrande, China’s biggest property developer. And even worse–the risk of a systemic debt crisis that could follow. This situation, while still developing, has calmed somewhat. However, this is probably really only the beginning of a new deleveraging campaign.

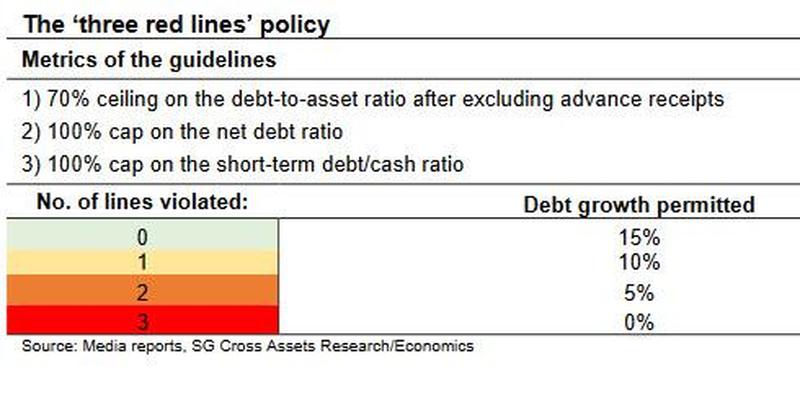

“It all started with the government’s proposal to contain developers’ leverage. On 20 August, the PBoC and the Ministry of Housing and Urban-Rural Development (MOHURD) held a meeting with key real estate companies where policymakers proposed the so-called “three red lines” framework for monitoring debt risk and reducing leverage in the sector. According to media reports, the “three red lines” were drawn up based on three financial metrics, including 1) the debt-to-asset ratio, 2) the net debt ratio,and 3) cash flows to short-term debt ratio.

“Future debt growth of real estate companies will be restricted in various degrees based on their current leverage as measured by these metrics (see the table below). In the harshest scenario, a developer will not be allowed to raise any more debt. Based on its current financial situation, Evergrande would in fact fall into this category.“