US debt is currently ~$29 trillion – up ~$6 trillion in 2 years.

All signs are Joe “10% for the Big Guy” intneds to double that rate this year even as supply chains are incapable of handing the modest economic growth to date.

No surprise, the 14% inflation we’re seeing (yes – it’s 14%) is where the dough is flowing.

That is, the ~$1 trillion/year yield suppression QE purchases by the Fed.

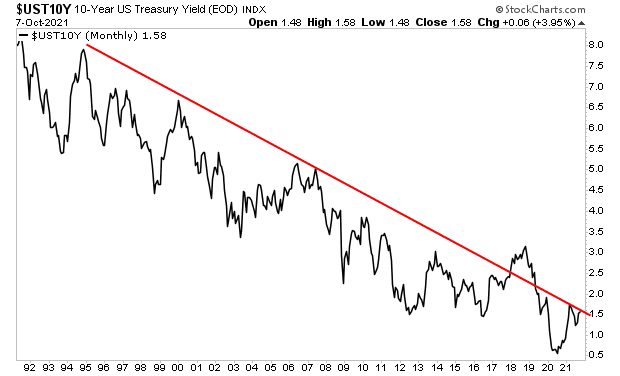

In 2018, rates broke to the upside and were doused.

However, this time, we have a constrained supply chain, Europe spinning out, Russia’s worsening food inflation and the prospect for the world’s largest wheat exporter to cap exports, and China running at low speed.

Commodity futures? Well, cotton’s price surge comes amid new concerns about the quantity and quality of the crops in top producers India and the US as harvest approaches. A pop in cotton import demand by China also undergirds the bullish tone.

Check out TLT (iShares 20 Plus Year Treasury Bond ETF) crumbling away as the world realizes lending money to a failing nation isn’t a great idea.

Higher interest rates, higher inflation, and a plunging Fed reputation?

The trend’s your friend until it ends.

And with rates, it might be end game.

Just remember who is “in charge” and where he is laser-focused: