Banking profitability is often measured in three ways:

- Return on Total Assets (RoA)

- Return on Risk-weighted Assets (RoRWA)

- Return on Book Value (RoE)

Why different ways for computing profitability?

Not all gains or losses are normally consider in computing profitability. They are only counted when realized, such as when the asset is sold.

Unless realized, gains and losses may be carried over as “Accumulated Other Comprehensive Income” or AOCI. These adjusted are captured on the balance sheet before computing “net retained earnings.”

AOCI filters for investment securities classified as “available for sale”, and reflects accumulated unrealized changes in the fair value of securities held for investment purposes.

Such unrealized gains and losses are not counted towards bank regulatory capital.

However, as part of the implementation of the Basel III capital accord, the AOCI filter is removed for the largest US banking organizations allowing fluctuations in securities market to flow through directly to regulatory capital.

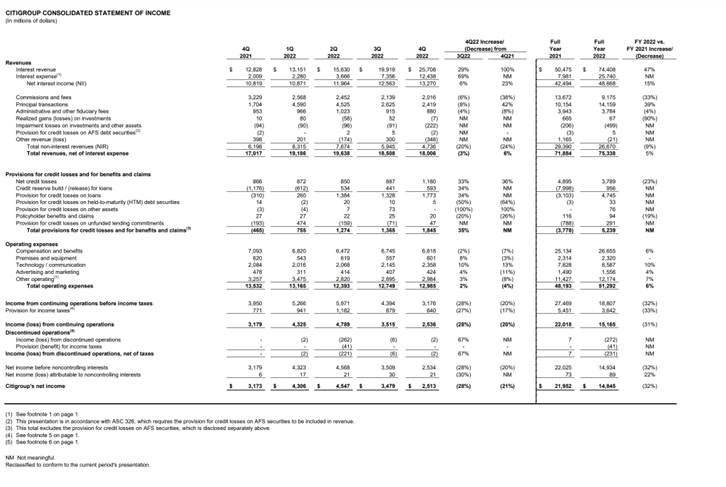

Consider Citi’s recent balance sheet above. For the quarter ending December 31, 2022, Citi has $47.062 billion of unrealized losses — reduced by $1.2 billion from the quarter ending September 2022.

Citi reported a net quarterly income on September 30, 2022 of $3.479 billion. Their December 30, 2022 net quarterly income was $2.513 billion.

Evidently, Citi recognized $1.2 billion of losses from AOCI.

At this rate, it will take Citi about a decade to rationalize to reduce their AOCI.

That’s assuming bank bond portfolios are not increasingly underwater as interest rates rise.

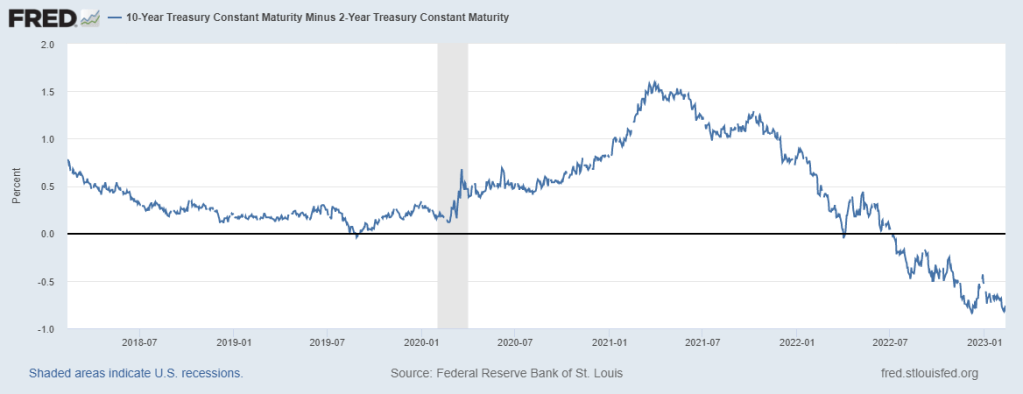

Consider the 2-10 spread – we’re seeing a definite trend repricing short-tenored assets.

S&P Global observes regulators are taking a closer look at AOCI (see https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/regulatory-focus-on-unrealized-losses-makes-liquidity-planning-key-for-banks-73761440).

One ratio regulators are starting to pay more attention to it since accumulated other comprehensive income, or AOCI, is not included in regulatory capital ratios, for any banks except global systemically important banks, therefore they do not capture the impact of underwater bond books, advisers said.

The majority of bonds that most banks hold are in available-for-sale, or AFS, portfolios, which must be marked to market on a quarterly basis. Changes in the values of the AFS portfolios are captured in AOCI. Higher interest rates have weighed on the value of bonds that banks own since they now carry below market rates. As a result, the vast majority of U.S. banks have recorded a surge in AOCI losses.

“Regulators have been clear that tangible equity is a loss-absorbing capital,” said Matt Resch, managing director and co-head of M&A and capital markets with PNC Financial Institutions Advisory Group. “If the credit cycle turns and there’s now an uptick in credit losses, it’s tangible equity that can absorb those losses. For banks that have seen a pretty significant impact to the tangible capital ratios, if now we end up having a turn of the credit cycle, it’s only going to exacerbate that problem.”

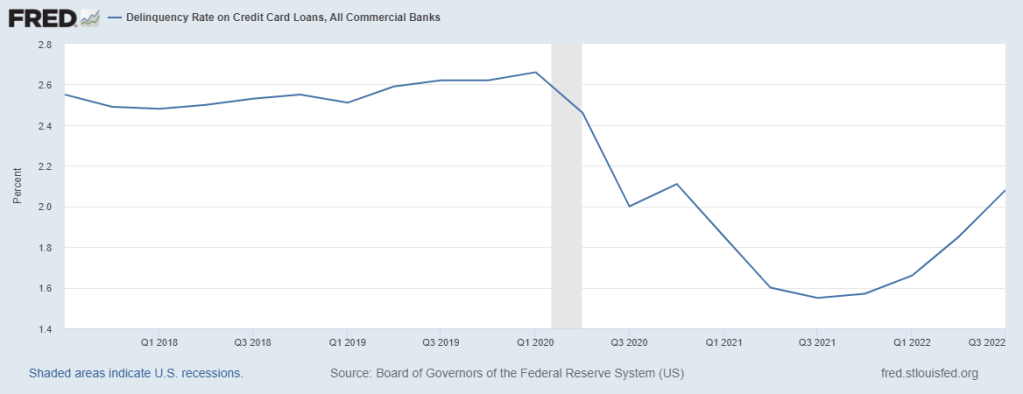

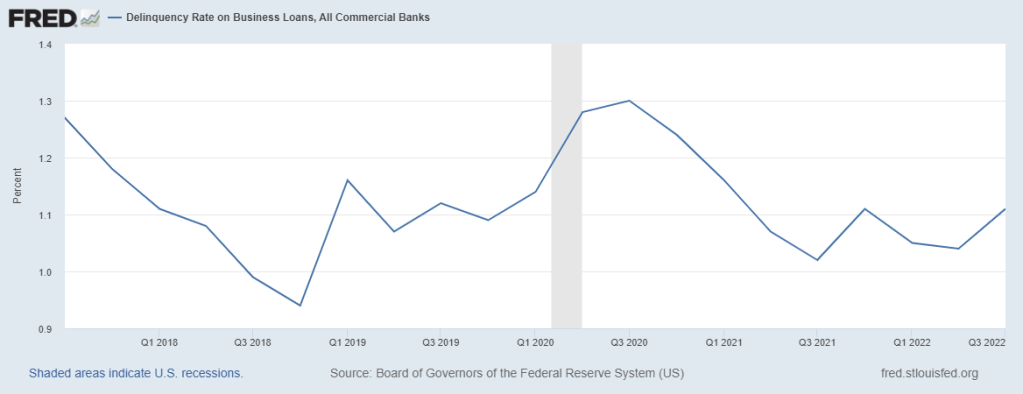

Upticking credit losses are already apparent.

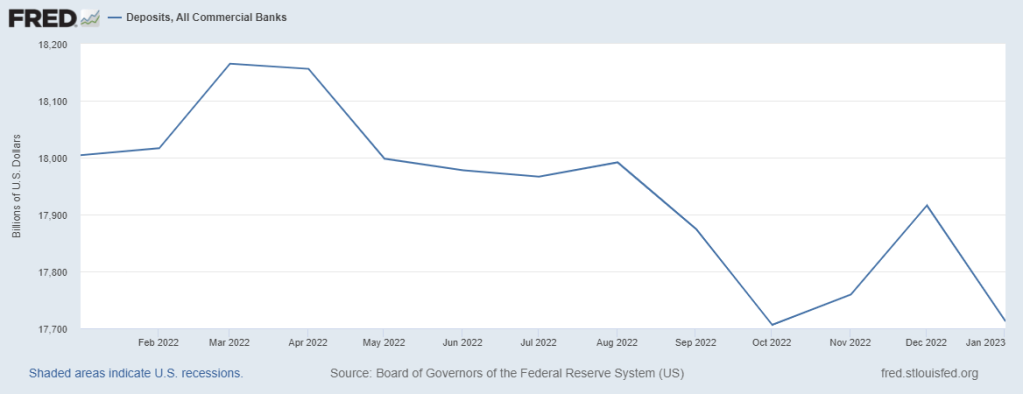

So are falling deposits.

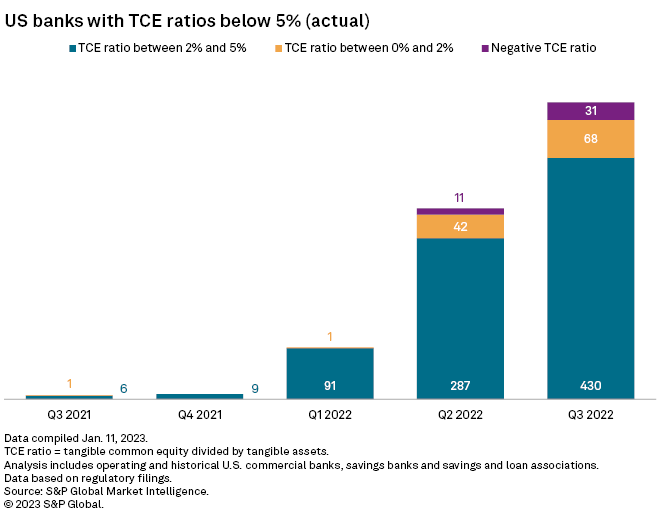

S&P Global reports banks with TCE ratios around 5% face problems, according to Donald Musso, president and CEO of FinPro Inc.

“Everybody that’s falling below certain metrics are getting calls and visits,” he said.

When a bank approaches 2%, 0% or negative TCE, “that’s when the real problem starts to occur,” Musso said, adding that regulators could start putting restrictions on banks through consent orders.

Going into CCAR 2023, expect liquidity and stress test to take closer looks at the AFS portfolio and AOCI trends.