Got it?

Whether it’s Bailey Bros Savings & Loan or Silicon Valley Bank, the fastest way to trigger a bank run is when the word gets out you are illiquid.

The duration gap is a financial and accounting term used to measure their risk due to changes in the interest rate. This is one of the mismatches that can occur and are known as asset–liability mismatches.

Another way to define Duration Gap is the difference in the price sensitivity of interest-yielding assets and the price sensitivity of liabilities (of the organization) to a change in market interest rates (yields).

Risk management 101.

You can get a gap a lot of ways — your credit losses can rise (the GFC scenario), your unrealized losses can rise from interest rate hikes (the current banking sector scenario).

The Lehman death scenario – funding long-term liabilities with short-term assets.

The duration gap measures how well matched are the timings of cash inflows (from assets) and cash outflows (from liabilities).

When the duration of assets is larger than the duration of liabilities, the duration gap is positive. In this situation, if interest rates rise, assets will lose more value than liabilities, thus reducing the value of the firm’s equity. If interest rates fall, assets will gain more value than liabilities, thus increasing the value of the firm’s equity.

Conversely, when the duration of assets is less than the duration of liabilities, the duration gap is negative. If interest rates rise, liabilities will lose more value than assets, thus increasing the value of the firm’s equity. If interest rates decline, liabilities will gain more value than assets, thus decreasing the value of the firm’s equity.

By duration matching, that is creating a zero duration gap, the firm becomes immunized against interest rate risk. Duration has a double-facet view. It can be beneficial or harmful depending on where interest rates are headed.

Some of the limitations of duration gap management include the following:

- the difficulty in finding assets and liabilities of the same duration

- some assets and liabilities may have patterns of cash flows that are not well defined

- customer prepayments may distort the expected cash flows in duration

- customer defaults may distort the expected cash flows in duration

- convexity can cause problems.

Let’s try an example.

When the duration gap is zero, the firm is immunized only if the size of the liabilities equals the size of the assets. In this example with a two-year loan of one million and a one-year asset of two millions, the firm is still exposed to rollover risk after one year when the remaining year of the two-year loan has to be financed.

Got it now?

So, what’s going on?

A lot of stuff like this as Lew Ranieri just posted (Lew of the South Ozone Park, Queens Ranieri’s — not to be confused with the Greenwich Ranieri’s).

And as Lew observes, that’s NOT the first floor.

And this

And Signature Bank just announced they’re closed by state authority.

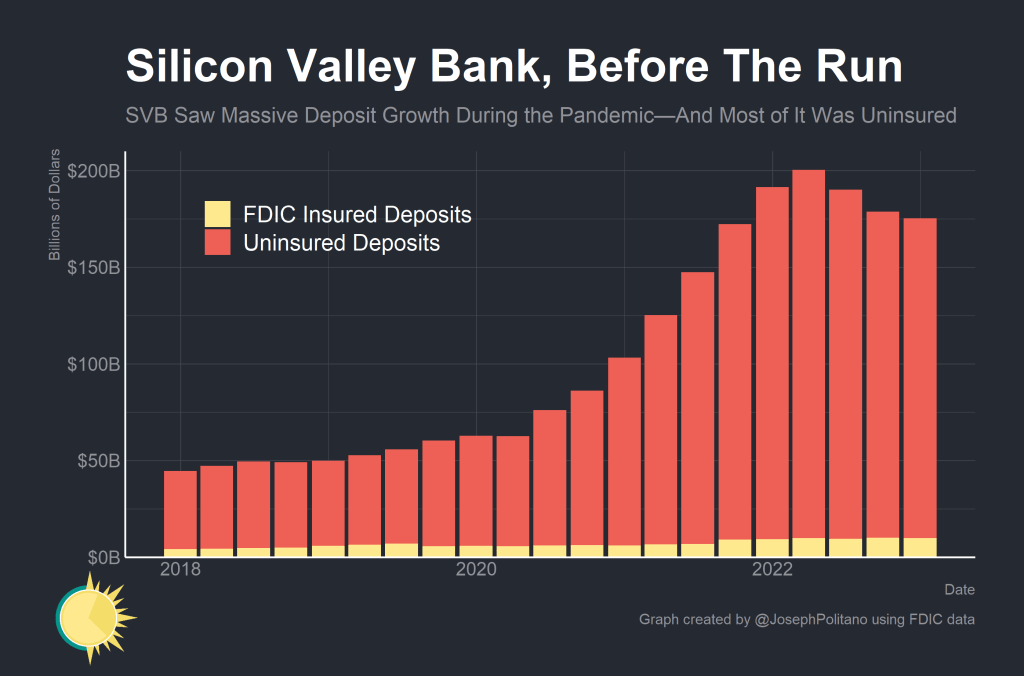

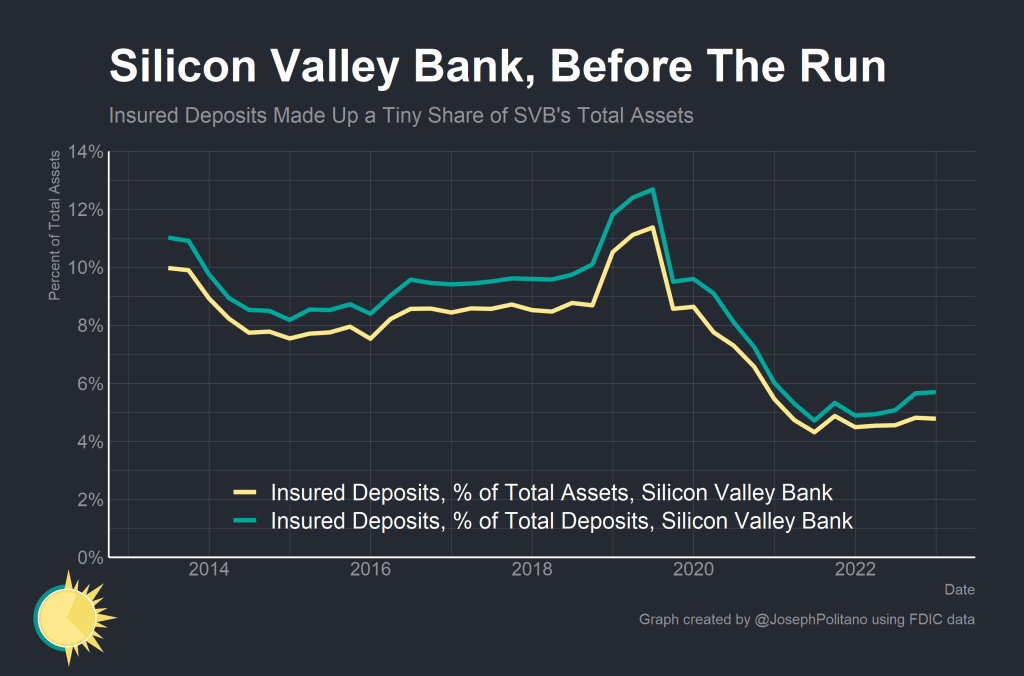

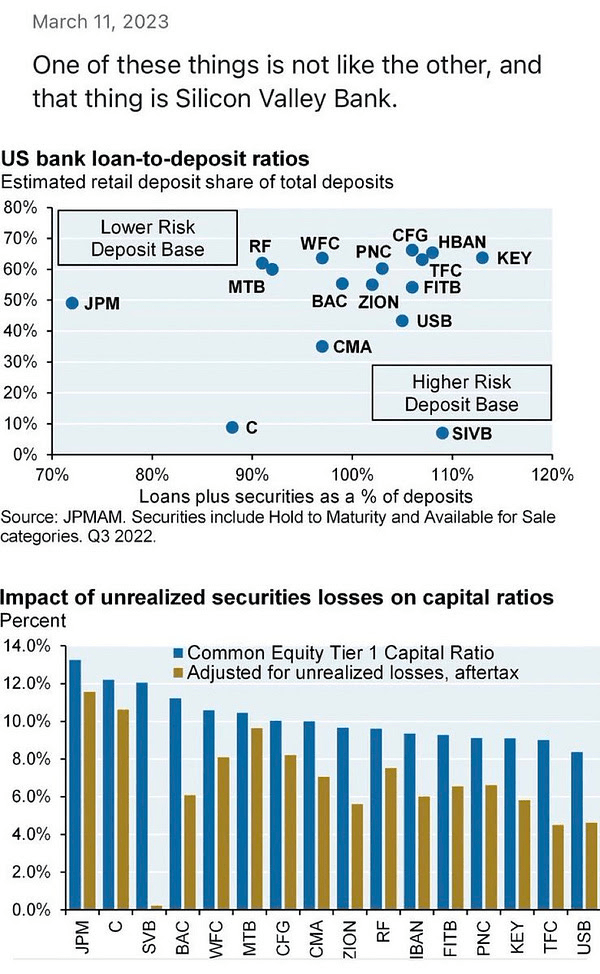

Here’s the pre-crash story — a lot of uninsured depositors appropriate to a business backed with high-end individuals.

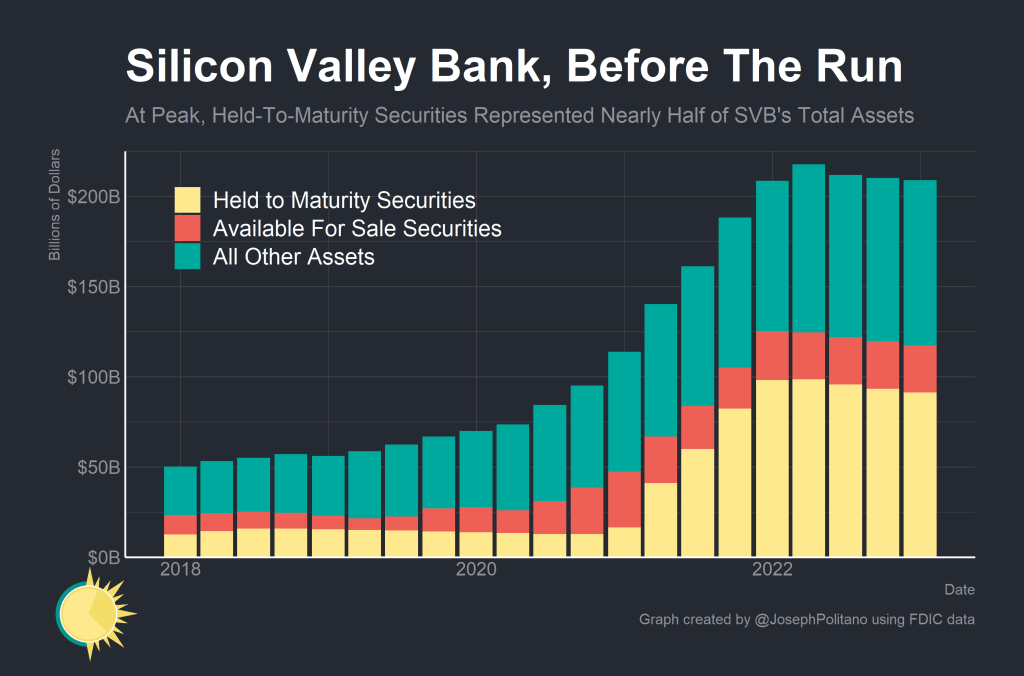

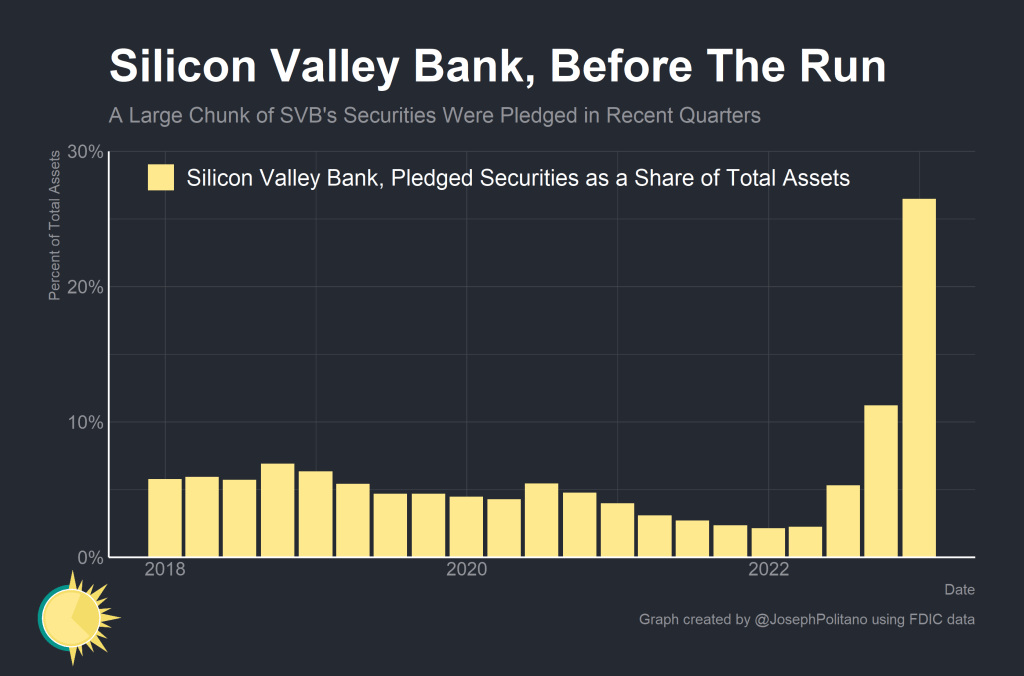

Deposits are a smaller fraction of the portfolio

With a growing fraction of long-dated assets.

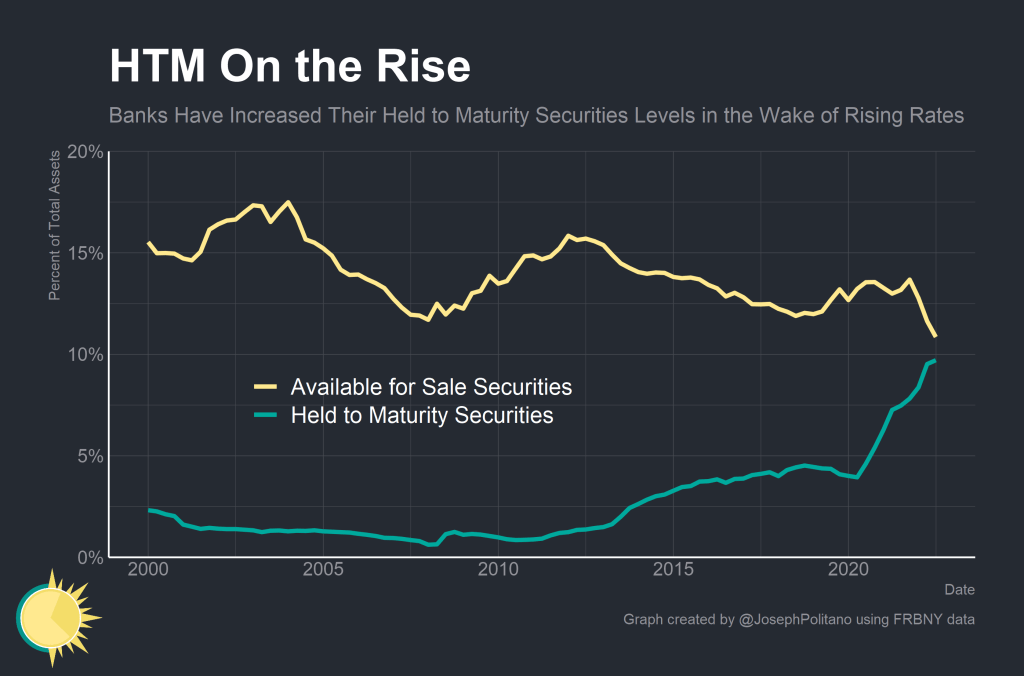

The dough had to go somewhere — so they went to long-dated securities like government paper — and then insanely held them to maturity as the Fed started raising interest rates.

Like climbing out on a limb while Jay Powell spins up a chain saw to cut the branch.

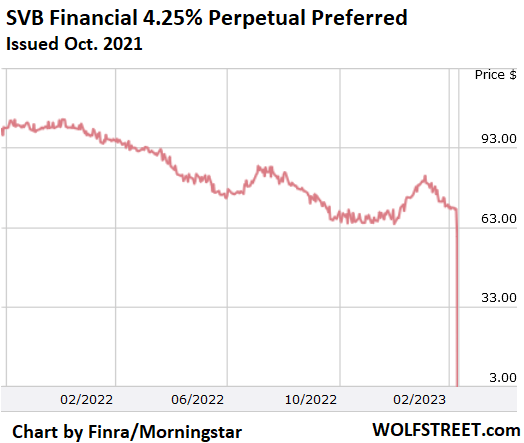

Here’s the effect of Jay’s cutting — AOCI starts piling up unrealized losses.

As Jay cut, the blood flowed all through 2022 while NOBODY did anything.

SVB was posting long-dated assets to back short term loans as the value of those assets plunged.

Duh!

Here’s SVB in the context of others from The_Real_Fly’s tweet

How did we get here? Let’s go to the tape.

Got it?

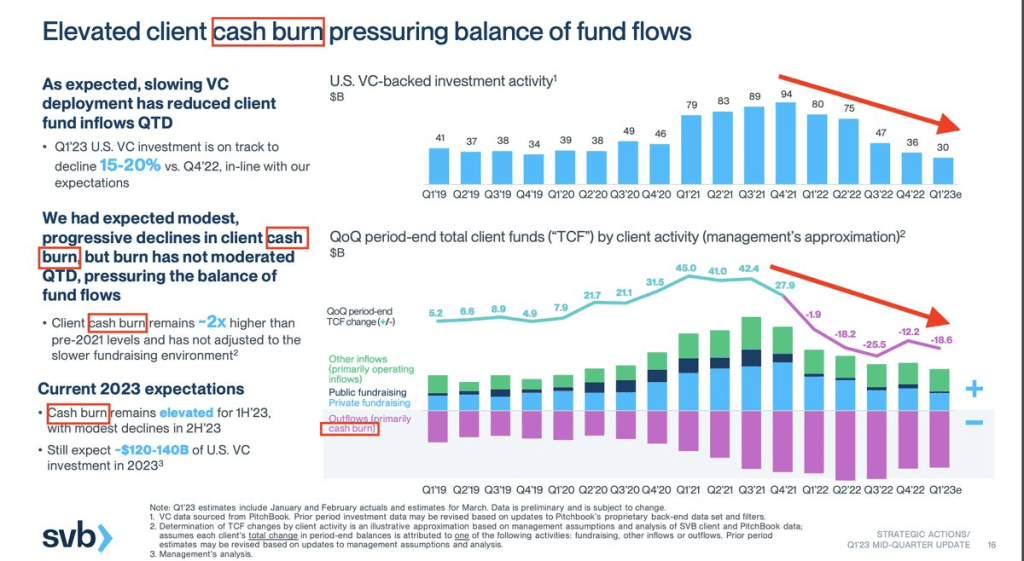

SVB was getting a slug of cash from Federal stimulus deposits over the last few years.

But, now the Congressional paydays are done and that cash is disappearing along with VC money — just like George Bailey when “Mr. Potter stole the drunk’s dough”

Normally, you would have a Chief Risk Officer with quant skills sufficient to anticipate these dynamics, and capable of advising how best to head them off.

Well, SVB’s last CRO left a year ago as the rats were starting to jump, leaving risk management in the hands of this thing — someone who could give you her pronouns before she could spell convexity:

I once had to work for a couple of unskilled “here are my pronouns” people at a company that went insanely woke. Fortunately, I worked for them for just for a short time.

Too long a story how it happened but it began with a class-act president leaving, replace by a wokester, my boss retiring, and well, you get the picture.

I saw the handwriting on the wall early but hung around to see what would happen. It was a surreal experience.

“Go ask Alice – when she’s 10-feet tall.”

Anyway, let’s go to the 2 minute “elevator pitch version” of what has happened and is currently happening, graciously provided by my trusted Mexican risk advisory

Clear enough?

SVB was full frontal woke, managing their portfolio on ESG, watching their unrealized losses pile up on their Treasuries as Powell drove interest rates back into the historic normal band.

As Jay hiked, SVB saw their deposits plunge as the Federal welfare wagon slowed.

And they did nothing.

Let’s recall the Clown Car exec team asleep at the switch — or sitting in DEI conferences 24×7:

- CEO: Greg Becker (Director at San Francisco Fed)

- CFO: Daniel Beck (former analyst at Freddie Mac)

- Chief Admin Officer: Joseph Gentile (Arthur Andersen -> CFO Lehman Bros – > SVB)

- Chief Risk Officer: Kim Olsen (led credit ratings in 2007 at Deutsche)

- Chief Legal Officer: Michael Zuckert (General Counsel at Citibank in 2008)

- Over the last 2 weeks, management sold nearly $5 million in stock.

Here’s Greg “Fearless Leader” Becker speaking at the “you’re fired/thanks for the memories” call (note the Gleneagles logo on his jacket – a primo golf resort in Scotland)

How about the ratings agencies? Where were they? Any “early warning”?

Nope – investment grade all the way up to the moment the FDIC stepped in, halted the bleed, and delivered the merciful kill-shot.

Let’s put this all in context by reviewing the week just ended:

- $200 billion collapse of Silicon Valley Bank in 24 hours

- Crypto market lost over $100 billion

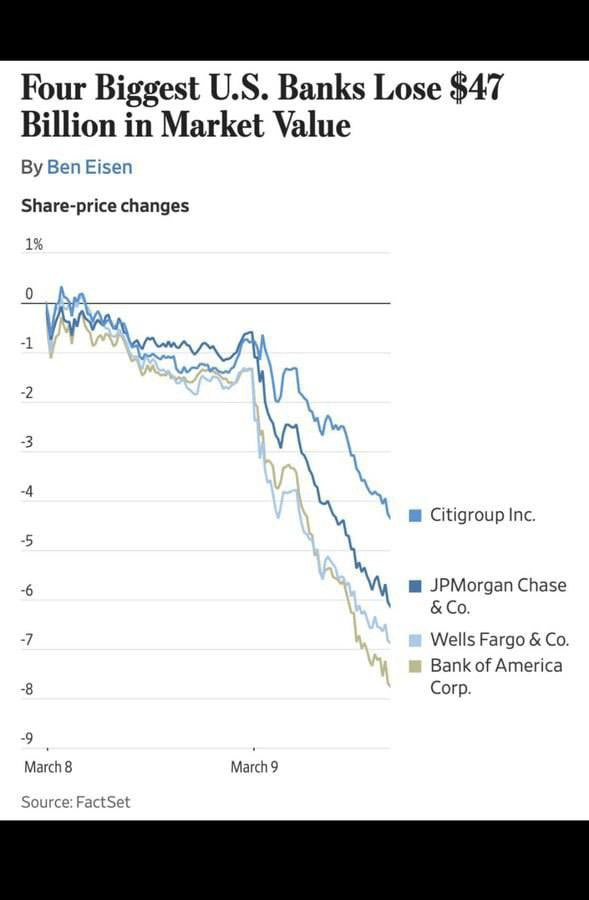

- Bank stocks lost $100 billion in value

- Mortgage demand hit 30 year low

- Fed said 2 million people will lose jobs

Who’s now at risk of a haircut or worse. Well, everyone with SVB balances over $250K are uninsured.

That includes:

- Circle: $3.3 billion

- Bill․com: $670 million

- Roku: $487 million

- BlockFi: $227 million

- Roblox: $150 million

- Sunrun: $80 million

- Ginkgo Bio: $74 million

- iRhythm: $55 million

- Rocket Lab: $38 million

- Sangamo Thera: $34 million

- Lending Club: $21 million

- Huuuge Inc: $24 million

- Payoneer: $20 million

- Ambarella: $17 million

- Protagonist Thera: $13 million

- Oncorus: $10 million

- Eiger Bio: $8 million

- Repare Thera: $7 million

Anybody you know?

And these are the only companies REPORTING exposure so far – ~$4 billion.

Yet SVB has $170 billion in uninsured deposits.

50% of all VC-backed startups in the U.S. have exposure to SVB.

97% or so of the deposits uninsured.

But there is a bright side — chatter has it Harry and Meghan had a lot of dough in cash in SVB along with Oprah.

We can dream, can’t we?

Clearly, the shareholders are wiped out. A lot of vendors stiffed. And, with haircuts all around, depositors will scramble to deal with their payments issues, take their haircuts, and move on.

So how does the US banking sector look this Sunday afternoon?

But, as our Mexican risk advisory said, “don’t panic” — Auntie Janet says there will be no bailout – just a “Special Monetary Operation” in the form of an SPV that looks like a bailout, smells like a bailout, and quacks like a bailout.

After all, a lot of California money on the table – that’s a lot of Progressive political power with substantial “value at risk”.

Here’s Auntie:

Translation — my “Special Monetary Operation” is a bailout.

For one thing, Jennifer Newsom has some “dough at risk”.

So Gavin says: “Mi problemo es tu problemo.”

After all, in the People’s Republic of California with $568 billion in debt, recall that 1% of the population pays most of the taxes. And a lot of that tax dough is — or was — parked in SVB.

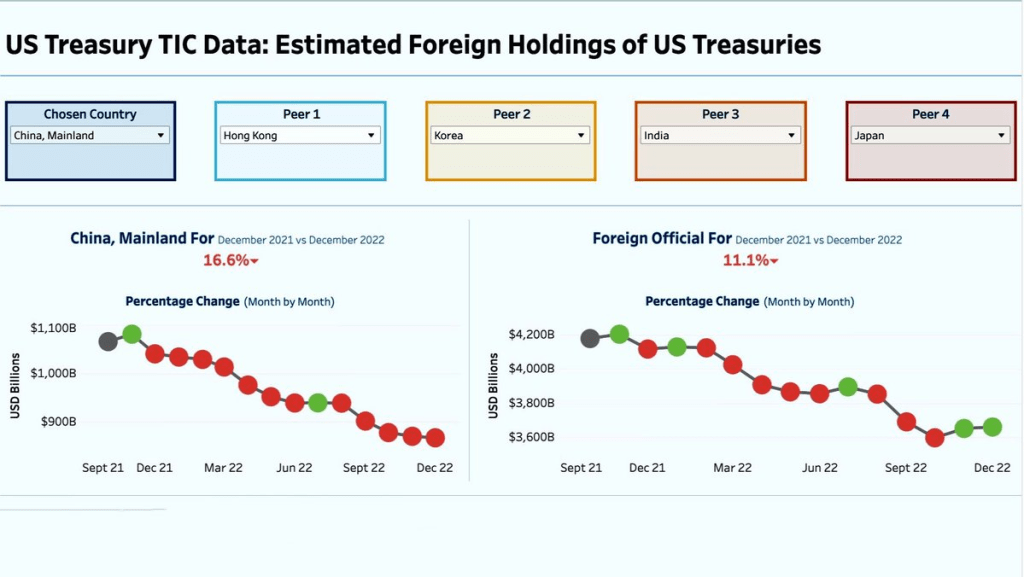

Meanwhile, in the real world, notes the Treasury dumping since the Biden Regime unlawfully seized power.

Not expecting the bank runs will do much to head this all off. And with China brokering peace between Iran and Saudi Arabia, any surprise China is no buying oil in Chinese yuan?

And the contagion risk is rising — HTM and AOCI are bleeding as interest rates rise, even as that portion of bank balance sheets gets bigger.

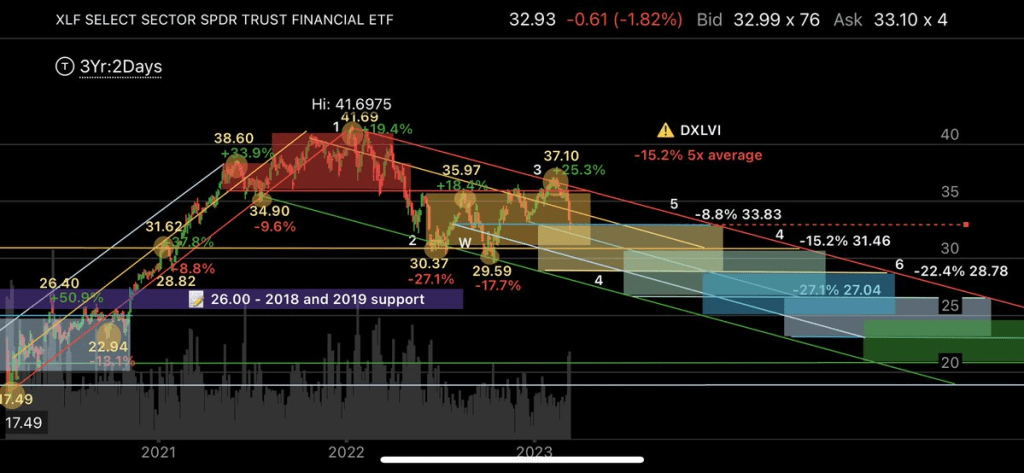

52 regional banks lost >10% market value last week with a combined market cap of $369 billion.

FDIC says the US banks are sitting on ovr $620 billion in unrealized losses.

As Winston Zeddemore famously said: “That’s a big Twinkie.”

Now, in fairness, some people did call this.

BTW, I want one of these shirts — I’m expecting to see a lot of these in the next few months in a wide variety of colors and logos.

It’s going to be a great week, kids. Lots of entertainment all around.

Cue up The Band — “it’s not like it used to be”