Fed policies are squeezing banks from multiple sides like the Wagner PMC meat-grinding the dwindling survivors of the decimated AFU brigades in Bahkmut.

AOCI trends have been negative putting an ever bigger drag on roll-offs.

Credit lines are hardening.

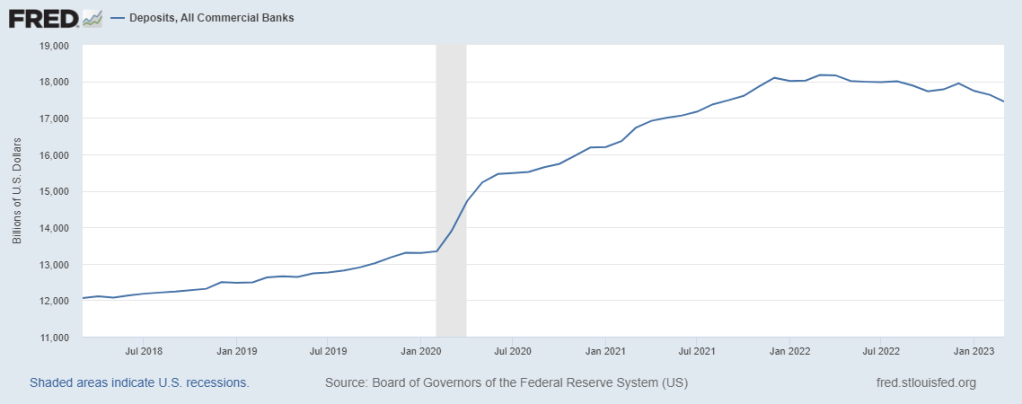

Rightfully so — deposits are tanking for the first time in, well, decades and decades. This is uncharted waters for most bankers.

It’s “May Day, May Day, Super-64 going down” time. Over $800 billion evaporated in Q1.

Down ~$1 trillion from peak deposit.

So, a lot of banks are going to have to go away in some fashion — voluntarily or “otherwise”.

There are several ways.

For example, there’s the “SVB way”. Or the “Signature Way” if you prefer.

Then, there’s also the firesale way. Or “break up into pieces way”.

Finally, a merger/acquisition of the survivors.

It’s fast becoming “eat or be eaten” as consolidation is all but a headline in Bloomberg.

Actually, Bloomberg is calling for stability – check this out: https://www.bloomberg.com/news/articles/2023-04-14/us-bank-lending-deposits-increase-in-the-first-week-of-april

LOL – yeah, right.

Of course, FT is on the case calling for 5600 banks at risk.

Which means those who sell into banks have a problem, don’t you think” Steve O”?

And if you are selling to these people when they are cutting back, well, let me tap into my “diversity training” to explain what that means (diversity is our strength, yada yada):

“Su problema es tu gran problema.”

Problema muy grande, camaradas!

These days, when any standard Fortune 500 woke-corp faces a crisis, its strategy is to double-down on woke principles that assume drive succes — translation manufacture more diversity.

You know, focus on discriminating more against some people for the usual reasons — skin tone, last name, age, gender — while promoting others for preferred characteristics like — different skin tone, different last name, different age, different gender.

Knowledge, skills, competency, and experience? LOL. Of course not — in times of crisis, it’s important you have the right statistical mix and emphasize your pronouns.

Which gets you betting your business on people like this

Oops, that’s back at Harvard. I meant this:

Her credentials: Groton, Harvard, Whaton, Intern … and then straight to VP and Chief Marketing Officer.

Not. Kidding.

Intern with minimal experience to “capa” with no real skills or industry experience.

No suprise, A-B bet an inexperienced exec with no knowledge of standard marketing analytics practice — like running focus groups on both the (1) target demo and (2) current cash cow — BEFORE approving the campaign to ensure net uptake is positive.

One does need quant skills for that — just “white board” and PPT skills taught at HBS.

And the ability to “think outside the box.”

Alisa went woke and bet on this

Which unfortunately can get you performance like this.

“However, since the furor over the partnership with Mulvaney, it saw a fall in that value of over $3 billion, with a market cap on April 10 of $130.8 billion. That figure has continued to decline since then, and as of 8 a.m. ET on Thursday, the company had a market cap of $110.6 billion—which would represent a fall of around $24 billion in 13 days.” Per Newsweek.

That’s the beer saga.

If your market is banking and insurance, you’re selling to people who are about to get whacked.

Go woke, go broke? Or get some competency.

Unlike beer where you can clip the woke team (good bye, Alisa), trust the competent and experienced who speak directly at you and stabilize the business before the squall hits and seas get heavy.

Meanwhile, my bank clients will handle this storm. They seem comfortable betting on quant skills, experience, and leadership.

In some places, that still counts.