In Ernest Hemingway’s 1926 novel The Sun Also Rises, Bill asks Mike, “How did you go bankrupt?” “Two ways,” Mike said. “Gradually and then suddenly.” Hemingway succinctly conveyed the way things tend to fail. The gestation may be long: a slow, gradual compounding of headwinds, errors and missed opportunities, with failure becoming probable long before it actually happens. When it does happen however, it may seem sudden and even unexpected.

The gradual decline of Japan

I’ve been following the gradual decline of Japan’s economy for over ten years; Way back in March of 2010 I published an article titled, “Japan: the Harbinger of (bad) things to come,” opening with the sentence, “Large and gathering imbalances brewing in the Japanese economy threaten to generate a tsunami-like fallout that could soak most of the global economy.” The Bank of Japan (BOJ) cut interest rates to zero in 1999 and started quantitative easing in 2001, using its monetary printing presses to buy up corporate bonds, REITs, stocks and Japanese Government Bonds (JGBs).

Over the ensuing 12 years and several rounds of ever greater QE, the imbalances have only worsened and in February last year, the BOJ was forced to go full Mario Draghi, all-that-it-takes, committing to buy unlimited amounts of JGB’s. At the same time however, the BOJ capped the interest rates on 10-year JGBs at 0.25% to avoid inflating the domestic borrowing costs.

Yen will burn to a crisp!

Well, if you conjure unlimited amounts of currency to monetize runaway government debt, and you keep the interest rates suppressed below market levels, you are certain to blow up the currency. On 8 March this year, when the yen was trading around 115 to the US dollar I wrote in my daily TrendCompass report that the “yen will burn to a crisp over the coming years,” as discussed also in a podcast with Tom Luongo. By the way, that podcast has aged remarkably well considering everything that’s been happening through the super-eventful year 2022.

The sudden collapse

By the end of 2022 we may also have reached the inflection point between Hemingway’s gradually and suddenly. In December alone, the BOJ escalated its JGB purchases to keep the yield on JGB’s capped at 0.25%: it spent 17 trillion yen (equivalent to about 3% of Japan’s GDP). In spite of that, on December 20 we saw the BOJ’s first battlefield retreat when it unexpectedly raised the maximum rate of 10-year JGBs from 0.25% to 0.50%. In spite of that, the BOJ had to continue spending huge sums to defend the new rate: on 12 and 13 January, it spent another 10 trillion yen (2% of GDP) wetting a new daily record. By now, the Bank of Japan owns about 55% of all Japanese Government Bonds.

The risk is this…

Yesterday morning (Wednesday, 19 January 2023), as it concluded its 2-day meeting, the BOJ Policy Board announced that it would hold the 10-year JGB yields firm at 0.50%. But the unravelling is far from over. As Jim Grant said in his recent interview, “Japan is perhaps the most important risk in the world, not least because it is among the least discussed risks… The risk is this: Every business day, the Bank of Japan is spending tens of billions of dollars worth of yen to enforce governor Kuroda’s yield curve interest rates suppression program. To put this into perspective: in the UK, when the little crisis over liability driven pension investing in late September happened, the Bank of England spent around $5 billion. The BOJ does that before breakfast.“

Grant is also right about the fact that Japan is among the least discussed risks today. By the way, if you wish to keep abreast of the developments in Japan, I recommend Richard Katz’s excellent Substack, “Japan Economy Watch.”

What happens next?

There’s no predicting how this situation will unfold. Corroborating Ernest Hemingway, Jim Grant also points out that bond market cycles tend to be very long and that trends reverse only very gradually. However, when governments and central banks resort to the printing presses to monetize debt, and we have seen many such cases through history, the typical outcomes include the collapse of the currency, rise in interest rates, and very probably a sharp rise in equity values. One such example, and a possible indication of what we might see in Japan, was Germany at the beginning of the last century:

Here again, we can see the gradual phase of the decline from about 1896 turn into the suddenly phase in the beginning of 1918. By the end of 1922, German government bonds had become nearly worthless.

Stocks go vertical…

What typically happens as bonds and the currency collapse, equities tend to go vertical as we saw in many cases, including Venezuela, Zimbabwe, Argentina, Israel and also the Weimar Republic:

This is perhaps because investors see holding any asset preferable to holding cash, so they plough ever penny they can spare into stocks.

Even if the timing and magnitude of these events can’t be predicted, such large-scale price events invariably unfold as trends. The most reliable way to navigate trends is with trend following strategies. For example, last year we’ve already seen the beginnings of the collapse of the yen. Here’s how the 12 trend following strategies included in our Major Markets TrendCompass report performed:

The top of the chart shows the price of US dollar in yen, which suddenly vaulted through most of 2022. And in spite of the yen’s strong recovery in the last quarter of 2022, I expect that this story has only started its suddenly phase of collapse. Over the coming months and years, we’ll likely see further pressure on the yen and JGBs. The Nikkei will likely break into a significant uptrend fairly soon.

It’s not just Japan…

With time, the same developments will almost certainly engulf Great Britain and the Eurozone. Ultimately, even the United States will not be able to avoid the collapse; that outcome is baked into the economic equation from the get go under the monetary system based on fractional reserve lending with a fiat currency.

Europe’s gas emergency: A continent hostage to seller prices

The 2022 outbreak of war between Russia and Ukraine revealed the importance of energy security in bolstering Moscow’s geopolitical power in Europe. The continent, which imported about 46 percent of its gas needs from Russia in 2021, found itself in a vulnerable position as it sought alternative sources.

This presented an opportunity for the US to replace Russia and become the primary supplier of natural gas to Europe at significantly higher prices, resulting in large profits at the expense of its European allies. According France-based data and analytics firm, Kpler, in 2022 the EU imported 140 billion cubic meters (BCM) of liquefied natural gas (LNG), an increase of 55 BCM from the previous year.

Around 57.4 BCM of this amount (41 percent) now comes from the US, an increase of 31.8 BCM, 29 BCM from Africa (20.7 percent) – mainly from Egypt, Nigeria, Algeria and Angola – 22.3 BCM from Russia (16 percent), 19.8 BCM from Qatar (14 percent), 4.1 BCM from Latin America (2.92 percent) – mainly from Trinidad and Tobago – and 3.37 BCM from Norway (2.4 percent).

European gas imports 2022

In 2022, France was the leading importer of LNG in Europe, accounting for 26.23 percent of total imports. Other significant importers included Spain (22.3 percent), the Netherlands (12.65 percent), Italy (11 percent), and Belgium (10.42 percent).

These countries, along with Poland (4.7 percent), Greece (2.9 percent), and Lithuania (2.31 percent), imported over 90 percent of LNG exported to Europe at prices higher than Russian pipeline gas. It is worth noting that upon arrival, LNG is converted back to its gaseous state at receiving stations in Europe before being distributed to countries without such infrastructure, such as Germany.

Graph: 2020-2022 European gas imports, by month

Switching dependencies

Europe was able to reduce its reliance on Russian pipeline gas from 46 percent to 10 percent last year. This decrease, however, came at a high cost to the economy, as the price of gas rose to $70 per million British thermal units (Btu), up from $27 before the Ukraine war. By the end of the year, the price had fallen to $36, compared to $7.03 in the US.

This price disparity has been hard to stomach. French President Emmanuel Macron went public with his annoyance: “American gas is 3-4 times cheaper on the domestic market than the price at which they offer it to Europeans,” criticizing what he called “American double standards.”

High gas prices have made Europe an appealing destination for gas exporters from around the world, with increased interest from countries such as Egypt, Qatar, Turkey, UAE, Iran, Libya, Algeria, and those bordering the Mediterranean basin, as they either export gas, or possess gas but lack infrastructure.

To replace the cheaper Russian pipeline gas, European countries are being forced to seek out the more expensive LNG. The EU and Britain are working to increase LNG import capacity by 5.3 billion cubic feet (BCF) per day by the end of 2023, and by 34 percent, or 6.8 BCF per day, by 2024.

Can West Asia, North Africa meet Europe’s gas needs?

The West Asia and North Africa region has the potential to partially meet Europe’s gas needs due to its geographic proximity and the presence of countries with large gas reserves and export infrastructure, such as Palestine/Israel, Algeria, and Egypt. However, there are several obstacles that must be considered.

Map of natural gas pipelines to Europe

For example, Egypt’s high production costs and increasing domestic consumption limit its export capacity. Additionally, Europe would need to be willing to pay a higher price than the Asian market for Egyptian gas.

Israel, on the other hand, has seen an increase in gas exports to Europe in the first half of 2022 after the pipeline to Egypt via Jordan was restored in March, but it is unlikely to significantly increase exports in 2023 due to factors such as limited export capacity and high domestic consumption. Experts predict that Israel may export around 10 BCM of gas to Europe this year, similar to the amount exported in 2022.

Qatar is the only Persian Gulf emirate that has increased its gas exports to Europe for 2022. This is largely because Persian Gulf countries prefer to sell their gas to Asian markets, where they can garner higher profits due to lower shipping costs and longer-term contracts.

Last year, Qatar took advantage of the significant increase in gas prices to sell part of its shipments on the European spot market. According to the Qatari Minister of Energy, between 10 percent and 15 percent of Qatar’s production can be diverted to this market.

However, it may be difficult for Europe to attract Qatari gas away from the Asian market, especially as China is expected to recover its demand for gas in 2023. In a policy home-goal, western sanctions on Iran, which has the second-largest natural gas reserves in the world, impede the investment needed to increase Iranian production.

No real alternatives

Iran’s lack of infrastructure connecting it to Europe and high domestic consumption also affect its export capacity. According to a report by BP, Iran produced 257 BCM of gas in 2021, of which 241.1 BCM were consumed domestically.

With regards to Algeria, the main obstacle in increasing its gas exports to Europe is political tension with Morocco and Spain that led to the suspension of the Moroccan-European gas pipeline project, which can export 10.3 billion cubic meters of Algerian gas.

In the case of the UAE, despite having the seventh-largest proven natural gas reserves in the world, its production is not sufficient to meet the demands of the local market and it imports a third of its gas consumption from Qatar through an undersea pipeline. European countries are currently in talks with Abu Dhabi to accelerate work on gas projects and increase production.

As for Saudi Arabia, it consumes all of its gas production domestically and does not export any, with a total production of 117.3 BCM in 2021. There are also expectations for a significant increase in the demand for oil and coal in 2023. The World Bank reports that this is due to an increase in European countries’ reliance on these fossil fuels instead of natural gas. This increase in demand will keep oil prices high, allowing Saudi Arabia and other OPEC+ members to make large profits.

The dilemma of growing demand

The Paris-based International Energy Agency (IEA) predicts that global demand for natural gas will increase to 394 BCM this year, driven in part by Europe’s need to diversify its sources of gas away from Russia. And West Asia, with its significant reserves, remains a key region for Europe to tap into for this purpose.

The challenge remains in finding cost-effective ways to transport the gas from the region to Europe, which will necessitate building a pipeline connecting the Mediterranean Basin to the Old Continent.

Failure to do so will result in Europe continuing to pay a high premium for its energy security without achieving true independence. The alternative for Europe is to rely on LNG from the US. This gives Europe almost complete independence from Russian gas, but keeps it weak, obedient, and dependent on American energy supplies.

Authored by Simon White, Bloomberg macro strategist,

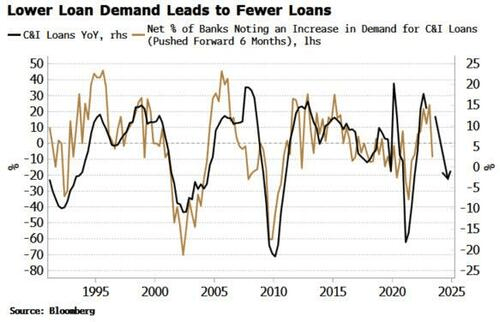

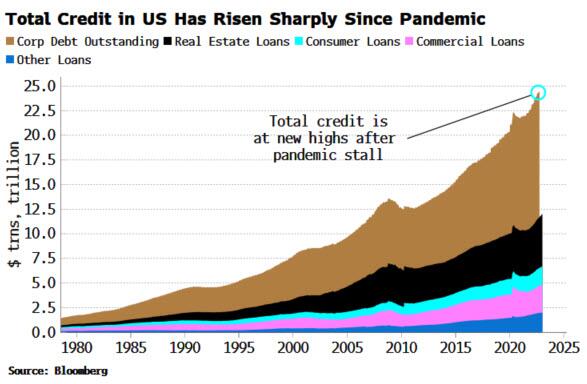

The credit cycle is turning, which points to wider credit spreads, increasing loan-losses at banks, and rising equity volatility.

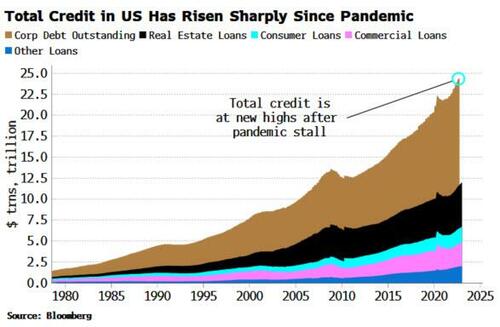

Credit has exploded higher since the pandemic. But all good things must come to an end, with credit busts typically following close on the heels of credit booms. Cracks are now emerging in lending markets as the sharpest monetary policy tightening in decades begins to bite.

The recent expansion in credit was across the board, from leveraged and private loans to corporate debt and bank loans. There was a brief retracement as some of the fiscal support extended to private lending was withdrawn after lockdowns were eased. But with monetary policy still extremely loose, credit took off again, soon making new highs.

Rapid expansions in credit are rarely a good thing as the quality of lending tends to deteriorate, ultimately leading to a bust as many loans go bad at once. This cycle has been no different, with more loans made at lower spreads, with fewer protections for lenders, and to lower-rated borrowers.

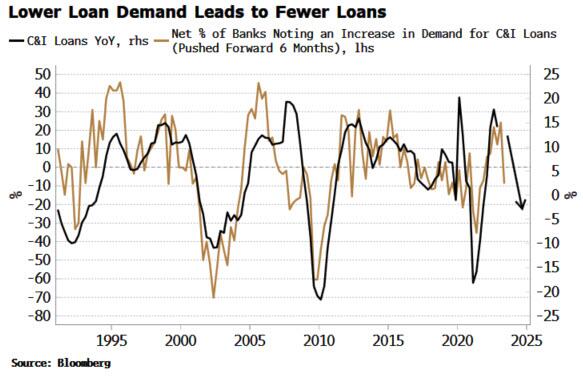

But after the feast comes the famine. The credit cycle operates in a well-defined sequence: first lending conditions tighten, then demand for loans falls, followed by a fall in loan supply. Loan delinquencies then increase as it is harder to get new credit, followed by a rise in charge-off rates as losses are realized. Finally, bankruptcies and defaults rise as loan losses lead to insolvencies.

Lending conditions have been tightening since October, based on the Fed’s Senior Loan Officer Survey for banks. This is leading to demand for loans falling, which in turn points to weaker loan growth.

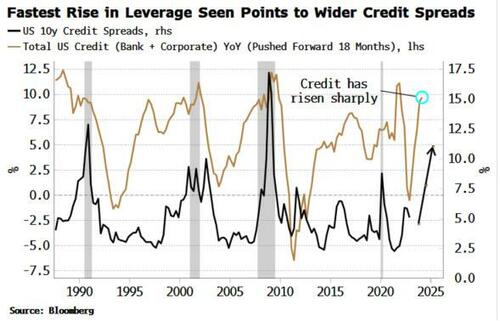

This tightening in conditions is not confined to bank lending – we are also seeing it in corporate debt, which dwarfs banks loans in size by about eight times. Credit spreads have widened markedly since the Fed has been raising rates.

I expect this trend to continue given the extraordinarily rapid rise in leverage since the depths of the pandemic. As the chart below shows, leverage leads credit spreads by about 18 months. This is because the bad lending that inevitably occurs during credit booms leads to stress on firms’ capital structures as old loans cannot be rolled due to tighter and pricier new lending.

Thus, despite the tightening in credit spreads seen in recent months, they are likely to begin widening again.

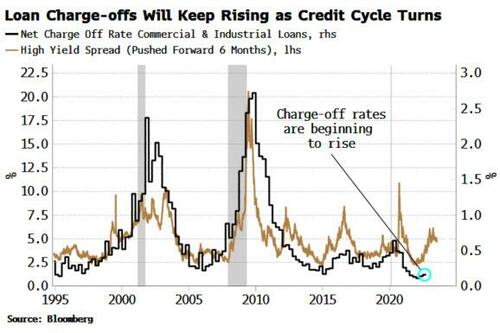

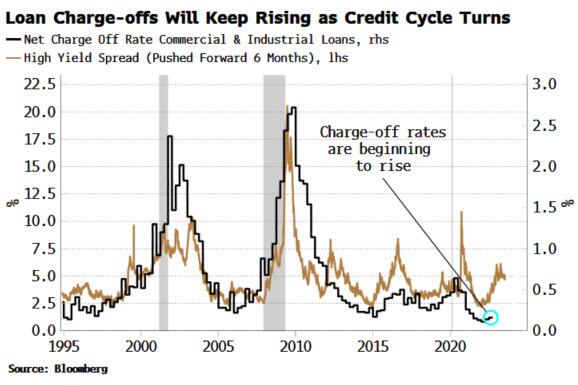

The most lagging parts of the credit cycle are delinquencies, charge-off rates and bankruptcies.

These peak during or after the recession, but begin rising before it. Delinquencies are slowly rising across loan categories, including credit cards, auto loans and mortgages.

Charge-off rates are beginning to climb as well. Wider credit spreads are a leading indicator for the further rise in loan charge-offs banks will soon see.

Lenders, including Bank of America and JPMorgan, have been increasing loan-loss provisions in preparation for a downturn or a recession. Still, loan-loss provisions for US banks remain more reflective of a zero-interest rate world, and are below where they were in the 1990s, a period with significantly above-zero rates similar to today. Banks are at risk from being underprepared for a potentially deep recession.

Cracks are also beginning to emerge in some of the most speculative parts of credit markets, such as leveraged loans. While a tiny sector compared to corporate credit, it is a harbinger for overall sentiment. Leveraged loans to junk-rated firms have been getting downgraded at the fastest pace since the pandemic, according to Citi, while leveraged-loan holders have a high sensitivity to rising rates due to floating-rate repayments and less hedging.

Weaker credit markets and wider credit spreads will also lead to higher equity volatility. The VIX has been missing in action this past year. After hitting 39 last January, it has remained below this level all through 2022 to now, despite one of the worst bear markets in over a decade.

A reduction in equity positioning leading to a reduced need for deep out-of-the-money downside protection is likely part of the reason, but that will change in a credit downturn and recession. Equity is just the thin sliver of capital between a company’s assets and liabilities, and when the capital structure comes under strain due to bad loans, the equity gets stressed leading to rise in equity volatility.

Loan and corporate-debt issuance has slowed this year compared to last, but the penny has not yet dropped that the credit cycle is on the cusp of turning, and could deteriorate significantly in the coming quarters – turbocharged by an impending recession. As always in markets, pay attention to what is going to happen, not what is happening, and prepare accordingly.

The 20 July Plot, an assassination attempt against Hitler, took place at the Wolf’s Lair on 20 July 1944.

The attempt was made by senior Wehrmacht officers with the backing of Allied nations. If successful, Germany would have been spared the final assault by Soviet and Western forces.

The German generals are trying it again. That’s the Wolf’s Lair plot of July 20, 1944.

To save themselves, they are begging their counterparts in Washington, DC, to find a way to lose the war in the Ukraine as quickly as possible without losing the US empire in Germany. This means overruling or replacing, not only Vladimir Zelensky’s regime in Kiev but also the Green Party ministers in power in Berlin, Robert Habeck and Annalena Baerbock, and maybe Chancellor Olaf Scholz to boot.

The Wehrmacht plotter this time is a retired brigadier general named Erich Vad (lead image, right). As German military officers go, he’s unusual. He was trained by a German-born Israeli infantry general turned academic. Vad then reached general’s rank, according to a senior German politician, but “never led a battalion, never led a brigade, and was never deployed in active operations”; he is a “desk general”.

Vad’s self-advertisements mention no active service or combat command. Instead, he has filled advisor posts at the Bundestag (2000-2006) and the Chancellery (2006-2013) when Angela Merkel was chancellor. Since 2014 he has been selling his advice either through Vad’s own consulting firm in Munich or a Swiss intermediary company in Zurich.

Merkel appointed Vad for the German military and the armaments industry to have a voice inside her office. Because they didn’t regard Vad as one of their own, Merkel promoted him to general’s rank.

The bomb Vad has just placed under Zelensky’s table and under the Green ministers’ desks in Berlin can be spotted in an interview he published last week in Cologne.

In his new press statement, as in every one of them since he left the Chancellery in Berlin, Vad is a supporter of war with Russia and its allies. “It was and is right to support Ukraine,” he declares at the beginning, “and of course Putin’s attack is not in accordance with international law.”

In July 2014, in his German press debut, Vad supported Germany’s role, alongside the US, in bombing Serbia. “As is well known, the situation for thousands of innocent people only changed when NATO soldiers set foot on Balkan soil.”

As Vad wrote this, Merkel had participated in the US overthrow of the Yanukovich government in Kiev; she had also begun her secret plan to rearm the Ukraine, and deceive Moscow of the German intention. A few days after Vad’s interview, after the Kiev regime arranged the shoot-down of Malaysia Airlines Flight MH17, Merkel vetoed a Dutch scheme for a NATO intervention in the Donbass. Vad had been warning Merkel to rearm Germany and the Ukraine before committing forces – Merkel had adopted Vad’s buy-time line.

In 2014 Vad didn’t mention the word “Ukraine”, but he expressly supported Merkel’s notion of rearming Ukraine to fight Russia, particularly if it was profitable for German business: “A responsible security policy,” he said in mid-July 2014, “also means supporting our partners [Ukraine] in the world across the entire spectrum of our capabilities, from development aid and good governance to equipment assistance and arms exports. As a global economic and financial power, we must not shirk our international responsibility. It is hardly comprehensible that pacifism in this country can go so far that we must not enable countries that act or want to act politically in our interest with the necessary means – e.g. with armaments – without the usual cries of horror. If we Germans ourselves do not want to or should not become militarily active worldwide, then we must at least be allowed to help those who are important for our national security interests in the hot spots of this world.”

In 2016, when asked to describe in detail what he had advised and agreed with Merkel in the earlier years, Vad said next to nothing.

In his latest press statement, dated January 13, 2023, Vad has warned that the Scholz government’s decision to supply the German-made Marder infantry fighting vehicle, in a joint rearmament plan with the US and France, “is a military escalation, also in the perception of the Russians, even if the 40-year old Marder is not a miracle weapon. We go on a slide. This could develop a momentum of its own that we can no longer control.”

Vad means the war in the Ukraine has already passed the point at which the US and German military believe they can control the outcome. “Now the consequences must be finally be considered” – this is Vad’s acknowledgement the war against Russia is being lost in the Ukraine.

Asked what “consequences” he means, Vad has replied with rhetorical questions: “Do they want to reconquer Donbass or Crimea? Or do they even want to defeat Russia completely?” Vad was identifying the goals of the civilian leaders in Berlin and in the State Department.

“We have a military operational stalemate, but we cannot resolve it militarily”, he noted, adding “this is also the opinion of the American Chief of Staff Mark Milley.” What Vad was implying was not “stalemate” but defeat – defeat by the Russian Army of the war allies in the Ukraine, including all the NATO reinforcements and operational plans. Those, Vad has dismissed: “There is no realistic end-state definition”.

He has then attacked the Green Party ministers in the German ruling coalition — explicitly Foreign Minister Annalena Baerbock, and implicitly Economy Minister and Vice Chancellor Robert Habeck. “I am glad that we finally have a [eine female] foreign minister in Germany, but it is not enough to just engage in war rhetoric and walk around Kiev or the Donbass with helmets and flak vests… I do not understand the Green’s mutation from a pacifist to a war party. I myself don’t know of any Green who has even done military service…The fact that a single party has so much political influence that it can manoeuvre us into a war is worrying.”

February 8, 2022 – Annalena Baerbock (right) with Ukrainian military escort in the Donbass.

Vad also attacked Scholz. Asked if he were his military adviser, what advice would he have given in February 2022. “I would have advised him to support Ukraine militarily, but in a measured and prudent manner in order to avoid the effect of sliding into a war party. And I would have advised him to influence our most important politically ally. Because the key to a solution to the war lies in Washington and Moscow.”

Vad repeated this message. “The key to resolving the conflict does not lie in Kiev, nor does it lie in Berlin, Brussels or Paris.” Vad’s interviewer didn’t notice the German general had not included London, and was ignoring the British in NATO and in their “special relationship” with the US.

Vad was also attempting to appeal to the Pentagon to save the situation. General Milley, Vad said, “has spoken an inconvenient truth. A truth that, by the way, was hardly published in the German media…. What is being waged in Ukraine is a war of attrition… This strategy did not work militarily then [1914-18] – and will not do so today”. To his German audience, Vad was also reminding them of the threats to German economic survival and political independence which followed the armistice of November 1918 and terms of the Versailles peace treaty of June 1919, and then led into World War II.

He then attacked the Scholz coalition for propagandizing the older German war aim without the military capacity to implement it against the Russian forces. “Military experts [and those] who know what is going on among the secret services, what it looks like on the ground and what war really means – are largely excluded from the [German public] debate. They do not fit in with the formation of media opinion. We are largely experiencing a coordination of the media, the likes of which I have never experienced before in the Federal Republic.”

Vad was implying there had been a stronger resistance to the war policies of Adolf Hitler and Joseph Goebbels, but not now against Baerbock, Habeck, or Scholz. “[From the German press] this is pure propaganda. And not on behalf of the state, as is known from totalitarian regimes but out of pure self-empowerment.”

“The Greens, FDP [Free Democratic Party] and the bourgeois opposition – flanked by largely unanimous media – are exerting such pressure that the chancellor can hardly resist it.”

Their war against Russia, Vad is warning, is not only lost in the Ukraine. It is threatening to destroy Germany in “a Third World War. And that’s exactly what doesn’t get into the minds of politicians and journalists here in Germany!”

“Germany is and remains an endangered nation”, Vad declared, adding that only the Americans can save the Germans from themselves now. “I myself am a convinced transatlanticist. I tell you honestly, when in doubt, I would rather live under American hegemony than under Russian or Chinese hegemony.”

He then revealed what he, his allies in the German General Staff and in German business circles want the Pentagon to negotiate with the Kremlin before the Russian Army advances to “the further destruction of Ukraine. What is left of this country? It is razed to the ground.”

“It is true that we must signal to the Russians: this far and no further!” How far across Ukrainian territory is that — Vad wasn’t asked and didn’t say. Nor did he disclose the terms which he and his German and US associates think can be negotiated in an agreement with Moscow against the resumption of the war against Russia in future. In fact, he doesn’t abandon the US-German war against Russian “hegemony” at all.

According to Vad, if the Pentagon concedes Russia’s “very specific geopolitical interests in the Black Sea region”, if the Donbass and Crimea remain Russian, “the territorial integrity of Ukraine would have to be restored, with certain Western guarantees. And the Russians also need such a security guarantee”. Exactly what “guarantee” can be negotiated after Merkel and ex-French President Francois Hollande have admitted their deception planning, Vad hasn’t advised, at least not in public.

“The West can send 100 Marders and 100 Leopards – they do not change the overall military situation. And the all-important question is how to deal with such a conflict with a belligerent nuclear power – mind you, the strongest nuclear power in the world! – without going into a Third World War. And that’s exactly what doesn’t get into the minds of politicians and journalists here in Germany!”

Left – the Schützenpanzer Marder 1, produced by Rheinmetall Landsysteme Maschinenbau in Kiel, between 1969 and 1975. Right, the Leopard main battle tank by Rheimetall and Krauss-Maffei Wegmann Maschinenbau of Kiel. Kiel voters think war against Russia is good for their incomes and have voted Green to achieve that result. In the last federal election of 2021, the Kiel vote saw the Greens gain almost 14% to score 28% of the total, while the Social Democratic Party lost ground but held on to the seat with 29.5%. Just over two thousand votes separated them. The anti-war Left and AfD candidates lost ground in Kiel, ending up with 5% and just over 7,000 votes each.

How does Vad and the Germans he is speaking for distinguish themselves now from the Wolf’s Lair plotters who believed – with secret US encouragement between 1943 and 1945 — that if the Wehrmacht could get rid of Hitler, they would make their deal with President Franklin Roosevelt to preserve Germany and continue the fight against the Kremlin? On one point, Vad is conceding the Russian Army is now more powerful by several magnitudes than it was in 1945, and Germany weaker by even greater magnitudes. And the US too, in Europe. This is the meaning of Vad’s phrase describing Russia – “mind you, the strongest nuclear power in the world!”

In such a balance of forces, Vad has calculated that Germany cannot survive as it has until now if the US protectorate is defeated in the Ukraine. He is also implying that the US protectorate which has now replaced Russian-made or locally made arms in Poland, Czech Republic, Slovakia, Romania, Greece, and Cyprus in exchange for expensive US rearmament, will also collapse into a rout.

“Excellent!” A veteran German banker with longstanding ties to the Chancellery in Berlin comments. “For once a moderating voice!”

From the German media Vad has been attacked for publishing “the opposite reasoning of the US State Department and other military experts”, and for whitewashing the war crimes of the Wehrmacht. According to Volksverpetzer, which claims to be a crowd-funded fact-checker, “under the guise of ‘expert status,’ [Vad] can then circulate narratives that almost coincide with Russian propaganda and are celebrated by those who spread pro-Russian narratives and disinformation. In his role as an ‘expert’, he first announces the defeat of Ukraine, then downplays attacks by Russia, talks about a nuclear war if heavy weapons are supplied, and denies, contrary to the assessment of many other experts, that Ukraine can win the war. There are other military experts who deserve this status without fear that there might be a politically tinged agenda behind their argument (source). All in all, the favourite general of the New Right seems more like a mouthpiece of Putin than a voice that can seriously assess the current situation.”

NOTE: To understand how committed the German military were, still are, to war for the destruction of Russian “hegemony”, read the works of German historian Christian Gerlach, now at the University of Bern in Switzerland. Start with Gerlach’s interview. Then his book, Chapter 9, “Hunger policies and mass murder”. According to Gerlach, for months before the attack on the Soviet Union began in June 1941, it was German military strategy to capture an area of Russia 2,000 kilometres deep and 1,600 km wide, seize all its crops and livestock to feed the German army and occupation forces, and starve the 30 million Russians to death. “This starvation policy [was] one of the biggest mass murder plans in human history [and] was designed earlier than any specific plans to kill European Jews, and was intended to kill far more [Russian] people.” For reference, the territory of the Ukraine in 2014 was 1,316 kms west to east, and 893 km north to south.

The imposition of US trade restrictions and sanctions against a number of nations, including Russia, Iran, Cuba, North Korea, Iraq, and Syria have been politically ineffectual and have backfired against western economies. As a result, the US dollar has been losing its role as a major currency for the settlement of international business claims.

Because they do not adhere to the policies of the US and other western powers, over 24 countries have been the target of unilateral or partial trade sanctions. These limitations, nevertheless, have turned out to be detrimental to the economies of the Group of Seven (G7) nations and have begun to impact the US dollar’s hegemony in world trade.

In its space, a “new global commercial bloc” has risen to the fore, while alternatives to the western SWIFT banking messaging system for cross-border payments have also been created.

Geopolitical analyst Andrew Korybko tells The Cradle that the west’s extraordinary penalties and seizure of Russian assets abroad broke faith in the western-centric paradigm of globalization, which had been declining for years but had nonetheless managed to maintain the world standard.

“Rising multipolar countries sped up their plans for de-dollarization and diversification away from the western-centric model of globalization in favor of a more democratic, egalitarian, and just one – centered on non-western countries in response to these economic and financial disturbances,” he adds.

Dwindling dollar reserves

The International Monetary Fund (IMF) recorded a decline in central bank holdings of US dollar reserves during the fourth quarter of 2020—which went from 71 percent to 59 percent—reflecting the US dollar’s waning influence on the world economy.

And it continues to worsen: Evidence of this can be seen in the fact that the bank’s holdings of dollar claims have decreased from $7 trillion in 2021 to $6.4 trillion at the end of March 2022.

According to the Currency Composition of Official Foreign Exchange Reserves (COFER) report by the IMF, the percentage of US dollars in central bank reserves has decreased by 12 percent since 1999, while the percentage of other currencies, particularly the Chinese yuan, have shown an increasing trend with a 9 percent rise during this period.

The study contends that the role of the dollar is waning due to competition from other currencies held by the bankers’ banks for international transactions – including the introduction of the euro – and reveals that this will have an impact on both the currency and bond markets if dollar reserves continue to shrink.

Alternative currencies and trade routes

To boost global commerce and Indian exports, the Reserve Bank of India (RBI) devised in July last year a rupee-settlement mechanism to fend off pressure on the Indian currency in the wake of Russia’s invasion of Ukraine and US-EU sanctions.

India has recently concluded agreements for currency exchanges of $75.4 billion with the UAE, Japan, and various South Asian nations. New Delhi has also informed South Korea and Turkey of its non-dollar-mediated exchange rates for each country’s currency. Currently, Turkey conducts business utilizing the national currencies of China (yuan) and Russia (ruble).

Iran has also proposed to the Shanghai Cooperation Organization (SCO) a euro-like SCO currency for trade among the Eurasian bloc to check the weaponization of the US dollar-dominated global financial system.

Mehdi Safari, Iran’s deputy foreign minister for economic diplomacy, informed the media earlier in June last year that the SCO received the proposal nearly two months ago.

“They must use multilateral institutions like BRICS and the SCO to this aim – and related ones, such as currency pools and potentially even the establishment of a new currency whose rate is based on a basket of their currencies, to mitigate the effects of trade-related restrictions,” Korybko remarked.

The International North-South Transport Corridor (INSTC) is being revived as a “sanctions-busting” project by Russia and Iran. The INSTC garnered renewed interest following the “sanctions from hell” imposed by the west on Moscow. Russia is now finalizing regulations that will allow Iranian ships free navigation along the Volga and Don rivers.

The INSTC was planned as a 7,200 km long multimodal transportation network including sea, road, and rail lines to carry freight between Russia, Central Asia, and the Caspian regions.

Ruble-Yuan Payment System

On 30 December, 2022, Russian President Vladimir Putin and his Chinese counterpart Xi Jinping held a video conference in which Putin reported that bilateral trade between the two countries had reached an all-time high with a 25 percent growth rate and that trade volumes were on track to reach $200 billion by next year, despite western sanctions and a hostile external environment.

Putin stated that there had been a “substantial growth in trade volumes” between January and November 2022, resulting in a 36 percent increase in trade to $6 billion. It is likely that the $200 billion bilateral trade target, if achieved by next year, will be conducted in Russian rubles and Chinese yuan, even though the details of the bilateral trade settlement were not specified in the video conference broadcast.

This is because Moscow and Beijing have already set up a cross-border interbank payment network similar to SWIFT, increased their gold purchases to give their currencies more stability, and signed agreements to swap national currencies in several regional and bilateral deals.

In addition, both Russia and China appear to have anticipated a potential US seizure of their financial assets, and in 2014 they collaborated on energy-centered treaties to strengthen their strategic trade links.

In 2017, the ruble-yuan “payment against payment” system was implemented along China’s Belt and Road Initiative (BRI). In 2019, the two countries signed an agreement to replace the dollar with national currencies in cross-border transactions and converted their $25 billion worth of trade to yuan (RMB) and rubles.

Independence from the dollar

This shift decreased their mutual reliance on the dollar, and currently, just over half of Russia’s exports are settled in US dollars, down from 80 percent in 2013. The bulk of trade between Russia and China is now conducted in local currencies.

Xinjiang in western China has also established itself as a key cross-border settlement center between China and Central Asia, making it a major financial hub in the region. Cumulative cross-border yuan settlement handled in Xinjiang exceeded 100 billion yuan ($14 billion) as early as 2013 and reached 260 billion yuan in 2018.

According to analyst Korybko, significant progress has been made in reducing reliance on the US dollar in international trade, but there is still much work to be done. He notes that the US is not likely to simply accept the challenges to its financial hegemony and is more likely to act to defend it.

“For this reason, it is expected that the US will try to enlist the support of key players by offering them preferential trade deals or the promise of such deals, while simultaneously stoking tensions between Russia, China, India, and Iran through information warfare and possibly threatening to tighten its secondary sanctions regime as ‘deterrence’.”

Eurasian Economic Union

Russia has been working to establish currency swap agreements with a number of trading partners, comprising the five-member Eurasian Economic Union (EEU), which includes Russia, Armenia, Belarus, Kazakhstan, and Kyrgyzstan.

These agreements have enabled the Russian Federation to conduct over 70 percent of its trade in rubles and other regional currencies. With a population of 183 million and a GDP over $2.2 trillion, the EEU poses a formidable challenge to western hegemony over global financial transactions.

Iran and the EEU have recently concluded negotiations on the conditions of a free trade agreement covering over 7,500 categories of goods. When the next Iranian year begins on 21 March, 2023, a market with a potential size of 700 billion dollars will become available for Iranian goods and services.

BRICS is driving de-dollarization

The trend towards de-dollarization in international trade, particularly among the BRICS nations, has gained significant momentum in recent years – together they represent 41 percent of the world’s population, 24 percent of its GDP, and 16 percent of its commerce

In 2015, the BRICS New Development Bank, recommended the use of national currencies in trade. Four years later, the bank provided 25 percent of its $15 billion in financial assistance in local currencies, and plans to increase this to 50 percent in the coming years.

This shift towards de-dollarization is an important step for emerging economies as they seek to assert their role in the global economic system and reduce their reliance on the US dollar. While the adoption of de-dollarization may present some challenges and uncertainties, it is an important step towards a more diverse and balanced global economy.

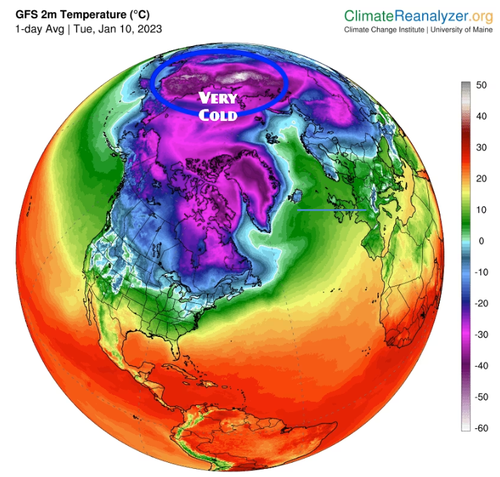

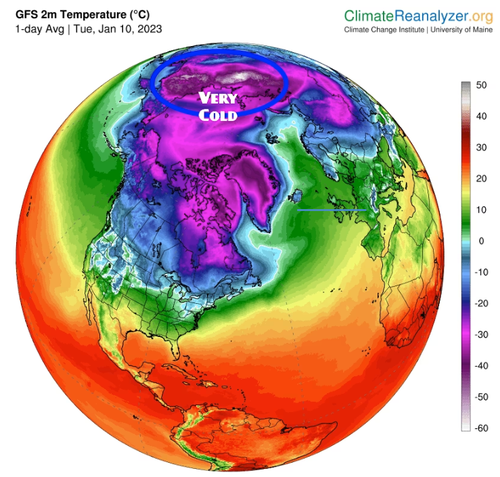

Siberia Records Minus-80 Degrees As Talk Of Polar Vortex Grows

BY TYLER DURDEN

SATURDAY, JAN 14, 2023 – 07:35 AM

Several weeks after the Christmas Arctic blast, much of the US and Europe have enjoyed record warmth. Recall on Dec. 27, we noted the cold air mass from Siberia that spread across the continental US would dissipate into the new year. So far, this is correct, as three weeks of above-average weather has staved off an energy crisis in the Northern Hemisphere. But just north, in Siberia, temperatures are sinking to near-record lows. And it could only be a matter of time before the giant cold air mass swirling in the North Pole becomes unstable, breaks down, and begins pouring into the US and Europe.

Global warming alarmists who called for an imminent climate disaster last summer are scratching their heads as the rural northern Siberian town of Zhilinda just recorded temperatures of minus-79.8 degrees, according to climatologist Maximiliano Herrera, who tracks extreme temperatures across the globe.

Herrera told The Washington Post that Zhilinda was just a few degrees off from breaking its record low of minus-82.3 degrees. The all-time low for the Northern Hemisphere was set in Russia in 1933 at minus-89.9 degrees.

Earlier this week, Arcfield Weather’s Paul Dorian said winter isn’t over and called for a significant change in North American weather “in about ten days or so.” Like anything, nothing is ever constant, and the warm spell could give way to colder temps later this month or early February.

“Sometimes, exceptionally cold air that builds over Siberia spills into the eastern United States,” WaPo explained, adding:

“Although the eastern United States has had very mild weather since that late December cold blast, there is the potential for a significant pattern change toward the end of January.”

For a polar vortex to flow into the US or Europe, there first needs warming in the Arctic stratosphere that pushes cold air lower. As explained by Michigan Weather Forecast:

This begins with the warming in the Arctic stratosphere which pushes the cold air south (simply put). The GFS, GEFS, ECMWS, and GEM models are displaying similar model runs. This is more of a heads-up than anything else. Do with it as you will, it is my humble opinion that winter in the sense of cold and snow isn’t over yet. We will see if the CPC comes on board with this.

And on Twitter, many folks are posting models predicting winter isn’t over and all that cold air trapped in the Arctic could pour into Europe and the US in the coming weeks.

Up in the mid-upper Polar Stratosphere (20-30km above the Pole), there are signs the currently stronger than normal Polar Vortex will start to weaken/warm by end of Jan/early Feb. Details on this are still not clear yet, but how this pans out will be key for February's weather! pic.twitter.com/gAJMgxAMHJ

For those who want a straightforward bottom line – #PolarVortex & tropospheric circulation are predicted to become increasingly coupled & supportive of more widespread #cold & #snow across the Northern Hemisphere in coming weeks but the important details are mostly still unknown. pic.twitter.com/7t7MO9nSPK

For those who want a straightforward bottom line – #PolarVortex & tropospheric circulation are predicted to become increasingly coupled & supportive of more widespread #cold & #snow across the Northern Hemisphere in coming weeks but the important details are mostly still unknown. pic.twitter.com/7t7MO9nSPK

#natgas It is impressive how fast the stratospheric vortex implodes by Jan29 (left) as warm air swallows the remains of a once mighty vortex (Jan9, right). This will reduce centrifugal forces and zonal winds, which will open the gates for polar air to flood continents. pic.twitter.com/mRRIAZHI7b

And maybe there’s some validity in the models above as the Climate Prediction Center’s 8-14 day temperature outlook has increasingly shown over the last week of colder weather slated for the end of the month.

So if the models are correct. Winter was just delayed.

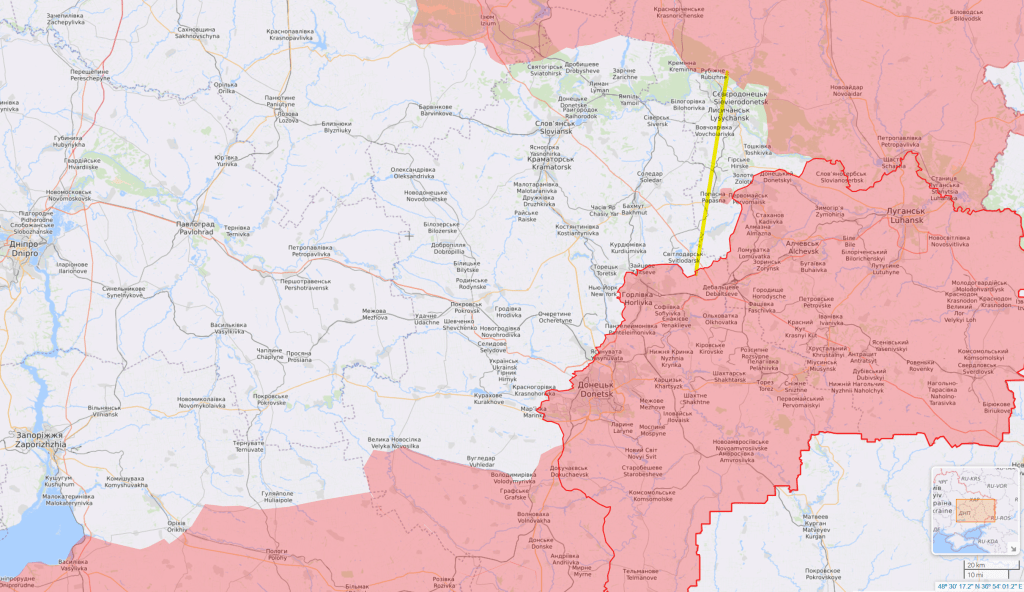

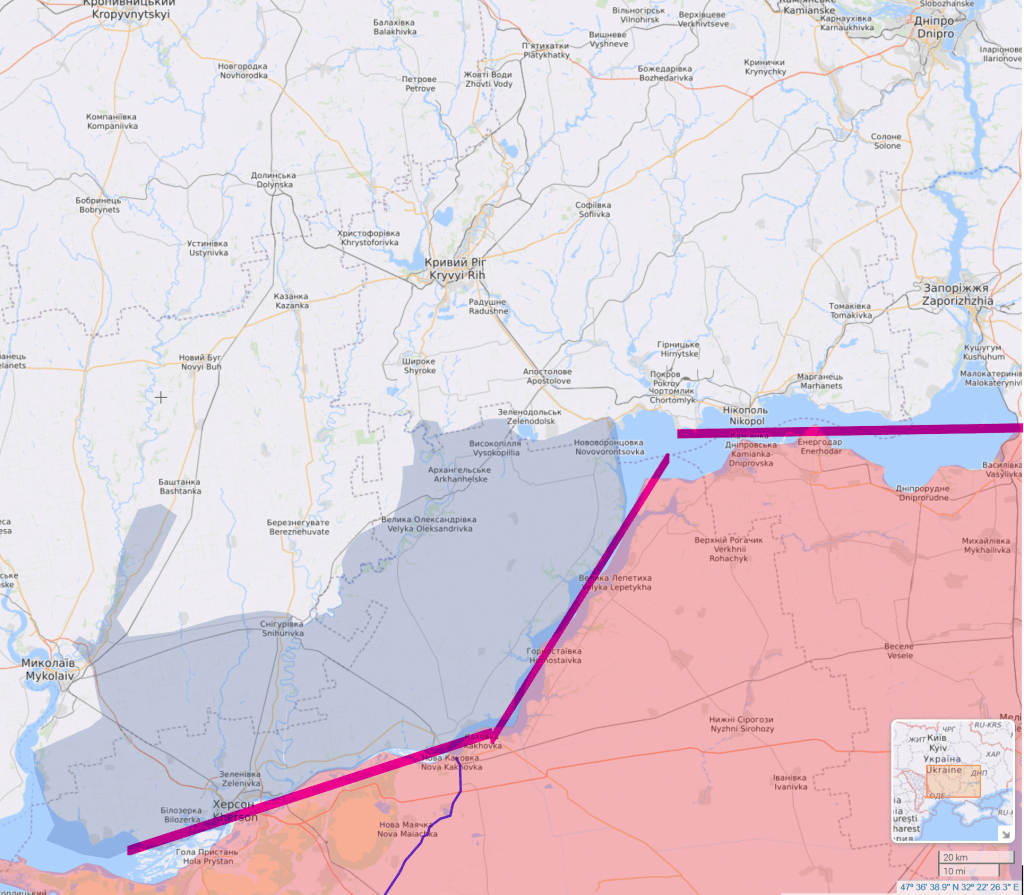

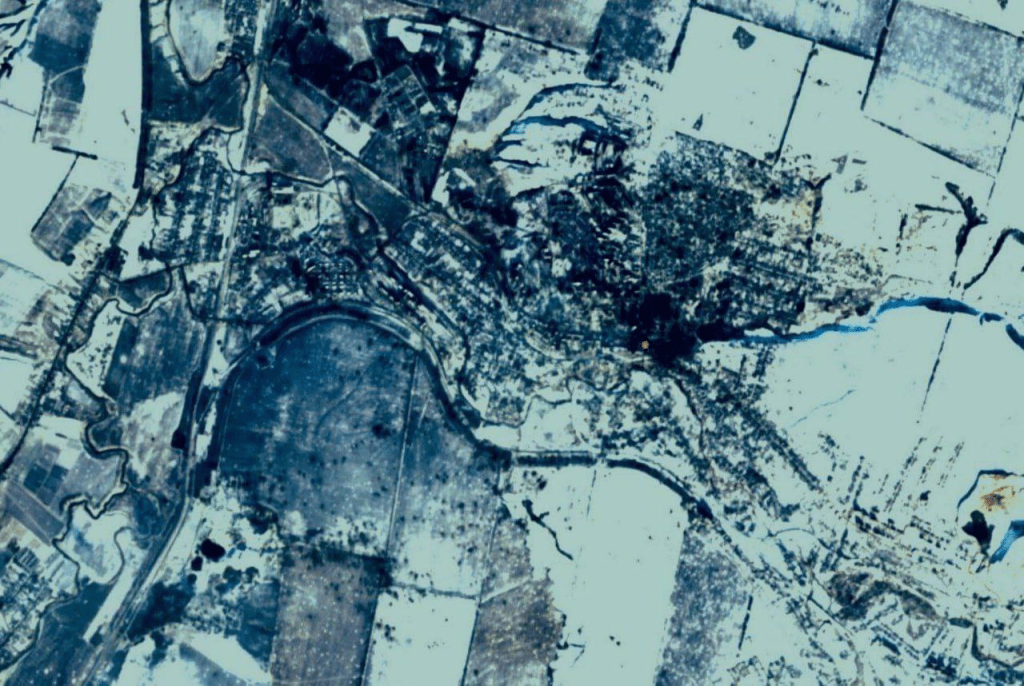

Soledar has fallen to Russian troops. Bakhmut (Artymovsk) will follow soon.

This constitutes the breach of Ukraine’s second defense line within the Donetzk and Lysichansk oblasts. I will discuss those lines with the maps below.

The first map shows the range of land taken by Russian forces by April 1 2022 (Kiev region not shown).

Russia had invaded with a small force of some 100,000 soldiers supported by some 50,000 soldiers of the Donetzk/Luhansk Republics. [Note: in February 2022, I assumed 400K-500K in the SMO invasion force.]The opposing forces were 250,000 regular Ukrainian army troops which quickly grew to 450,000 and then 650,000 by mobilization of reserve forces plus the Territorial Defense Forces. During the first weeks the Russian forces had taken a huge amount of land that they barely had the numbers to hold.

At that point Russia was still hoping that the negotiations held at that time with Ukraine in Turkey would have a positive outcome. As a confidence measure it had already started to pull back from around Kiev. However, after phone calls from and a visit by the British prime minister Boris Johnson the Ukrainian government ended the negotiations by suddenly adding demands the Russia would never agree to. The troops from Kiev were pulled back anyway and moved to the east of Ukraine where they started an attack on the first defense line (yellow) of the Ukrainian forces.

April 1 2022

This first defense line, like later ones, ran along railway and road communication routes that connect major cities. In the map above the cities that constituted the first defense line were, north to south, Siverodonetsk, Lysichansk, Popasna, Svitlodarsk.

By July 1 2022 the first Ukrainian defense line was breached and defeated by Russian forces. The Ukrainian troops moved back to their second defense line. However, the defeat of the first defense line had taken its toll of the small Russian Special Military Operation force.

July 1 2022

The second Ukrainian defense line, north to south, ran from Siversk to Soledar, Bakhmut, New York agglomeration and then along the old ceasefire line of the Donetzk Republic.

The Russian forces tried to avoid a costly direct attack on the second Ukrainian defense line. It launched an operation to breach into the Donetzk oblast behind the second Ukrainian defense line from the north (now gray area). The battles for Izium and Lyman were fought for that purpose. However, the wooden area north of the Siversky Donets river that runs east to west as well as the river itself proved to be difficult to cross. Several attempts to move significant forces across it failed.

At the end of August 2022 the exhausted Russian forces had switched to a defensive posture and into an ‘economy of force’ mode. Troops that were holding the Kharkiv area north of the Donetzk oblast were reduced. The other forces were moved to the eastern front to strengthen the Russian lines on that front.

Meanwhile Ukraine was openly discussing and preparing for an attack on the Kherson region north of the Dnieper river with the final aim of crossing the river to then move towards Crimea. Russia responded by further reducing the troop numbers in the northern Kharkiv region to a few thousand men and by using the others to further strengthen its positions in the south around Kherson.

During the fall the Ukrainian attacks on the Kherson region all failed with high losses. However U.S. intelligence advised the Ukrainian command that the Kharkiv region, while still held by Russian forces, was practically empty. The command switched the active front towards the north and successfully moved into the Kharkiv region while Russian troops still positioned there moved further east.

This was a quite fast operation that looked very successful. But the speed also meant that the heavy Ukrainian artillery cover was thin to not existent. This while the retreating Russian forces used their own artillery to attack Ukrainian front formations in pre-planned fire missions. After proceeding fast over some 70 kilometers from west to east the Ukrainian attack force had taken high losses and ran out of steam. It came up to a new Russian defense line (red) covered by two rivers that proved difficult to cross. The Kharkiv front has since stabilized.

Jan 1 2023

The Ukrainian ‘victory’ in the Kharkiv region gave the Russian government the necessary public backing for the mobilization of additional forces. 300,000 reservists were called up. Some 70,000 additional men joined as volunteers. The Wagner private military company increased its force size to some 50,000 men. Over the last three month of 2022 all those forces were supplied with the necessary equipment and went through refresher training.

Meanwhile a new Russian commander, General Sergey Surovkin, took over. He warned immediately that he would have to take some difficult decisions. This was related to the situation in the Kherson region north of the Dnieper. Constant attacks on the river crossings with U.S. supplied missiles made the logistic situation very difficult. The command decided to pull back behind the river. This operation was remarkably successful. Ten thousands of civilians plus some 25,000 soldiers with all their equipment were removed from the area with only few if any losses.

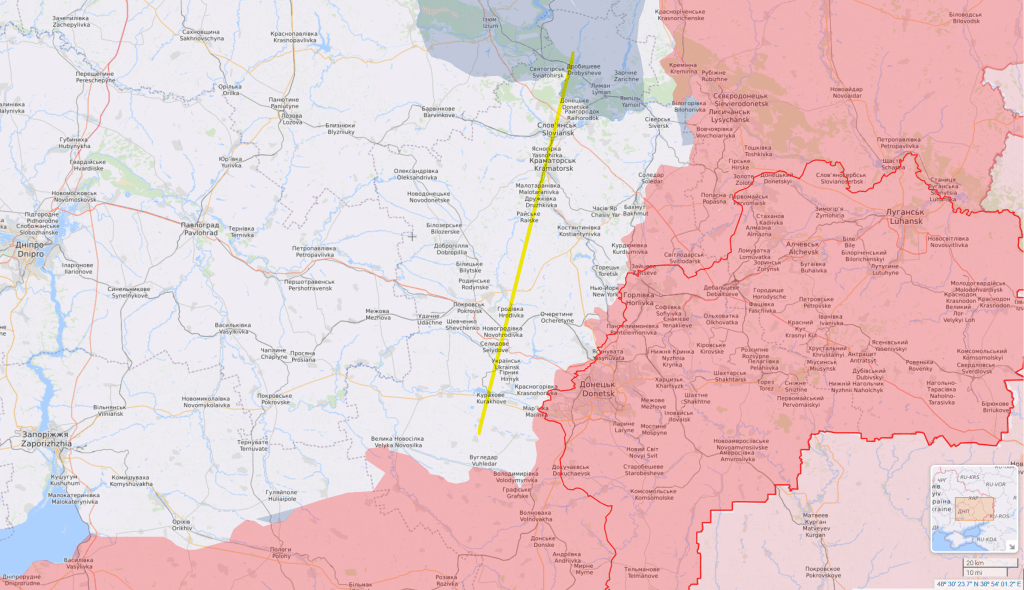

By the end of the year the shortening of the front lines and the introduction of fresh forces had allowed the Russian forces to regain the initiative. They launched intense attacks on Ukraine’s second defense line. With the successful taking of Soledar that line has now been breached. This makes the situation of Siversk, north of Soledar, and of Bakhmut, south of it, much more difficult. No Ukrainian troops or materials can now be moved on the roads and railways that were part of the line. The breach of the line will allow Russian troops to move west of it to the north and the south to then create cauldrons for the other positions within that same line. ‘Rolling up a defense line’ is a description of that process.

The now heavily reduced Ukrainian forces will likely have to give up on holding the second defense line to then create a third one to the west of it.

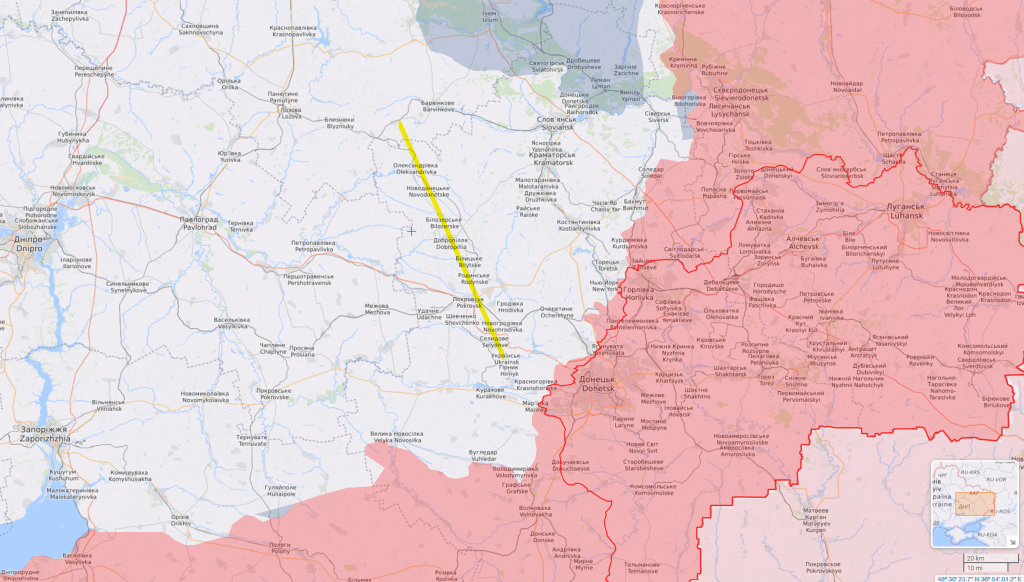

The third Ukrainian defense line will run from Sloviansk in the north through Kramatorsk, Druzhkivka, Kostantinovka to the New York agglomeration. I expect the complete defeat and cleanup of the second Ukrainian defense line by the end of March. The third Ukrainian defense line will probably fall by the mid of the year. Whatever is left of the Ukrainian forces will then try to hold a fourth defense line along the string of smaller towns west of it.

This will be the last Ukrainian line in the Donetsk oblast. It likely to fall before by the end of September.

The Russian moves against the third and fourth Ukrainian defense lines will likely be supported by a move from the south that will liberate the rest of the Zaporiziha and Donetsk oblast.

Aside from those operations the Russian command has sufficient number of troops available to run another major attack. This could come from the north into the Kharkiv regain behind the Ukrainian troops currently attacking the Russian lines further east.

The Russian forces in Ukraine were tasked with liberating the oblast that Russia had recognized as independent states (Donetzk and Luhansk) as well as those that had additionally voted to become part of Russia (Zaporiziha and Kherson).

With the breaking up of all four Ukrainian defense lines in Donetzk oblast that task will be fulfilled. This with the exception of the part of the Kherson region north of the Dnieper river which will require a separate operation on its own. The Russian command may want to wait for this until more Ukrainian forces have been destroyed while holding their defense lines.

Another task given to the Special Military operation was to ‘demilitarize’ and ‘denazify’ Ukraine. The Ukrainian tactic of holding fixed lines anchored on major cities at any price has come at a significant cost. Russian artillery is superior to the Ukrainian by a factor of ten. The Russian forces use it to destroy Ukrainian troops holding the lines while taking only few losses on their own side.

Today’s Wall Street Journal finally noted that this Ukrainian battle tactic is not a winning one:

Western—and some Ukrainian—officials, soldiers and analysts increasingly worry that Kyiv has allowed itself to be sucked into the battle for Bakhmut on Russian terms, losing the forces it needs for a planned spring offensive as it stubbornly clings to a town of limited strategic relevance. Some of them say that it would make sense to retreat to a new defensive line on the heights west of Bakhmut while such a pullback can still be organized in a coordinated fashion, preserving the Ukrainian military’s combat strength.

“It’s not me, it’s King Leonidas who figured out that you should fight the enemy on the terrain that is advantageous to you,” said one Ukrainian commander in Bakhmut, referring to the ruler of Sparta who battled the Persian Empire at Thermopylae. “So far, the exchange rate of trading our lives for theirs favors the Russians. If this goes on like this, we could run out.”

The Ukrainian soldier is right. However, a different form of fighting the war would be a mobile delay and retreat action from which local counter offensives would be launched. This requires a lot of equipment, battle tanks and infantry fighting vehicles, that the Ukraine no longer has. It also requires troops and larger formations trained for that type of fight. Some 60 year old mailman drafted during Ukraine’s 9th mobilization wave will not be able to learn this during his two weeks training course.

Had the professional Ukrainian army that exited before the war been allowed to give up on cities and had it used a mobile combined arms tactic of delay-retreat-counterattack it probably would have been more successful. But that army has by now been destroyed with Russian artillery because Kiev insisted on holding cities and lines at any price.

The U.S. will only now start to train Ukrainian troops in combined arms and joint maneuvering. It will be too little too late to make any difference.

As of current news, today we see fake news headlines like this from NBC:

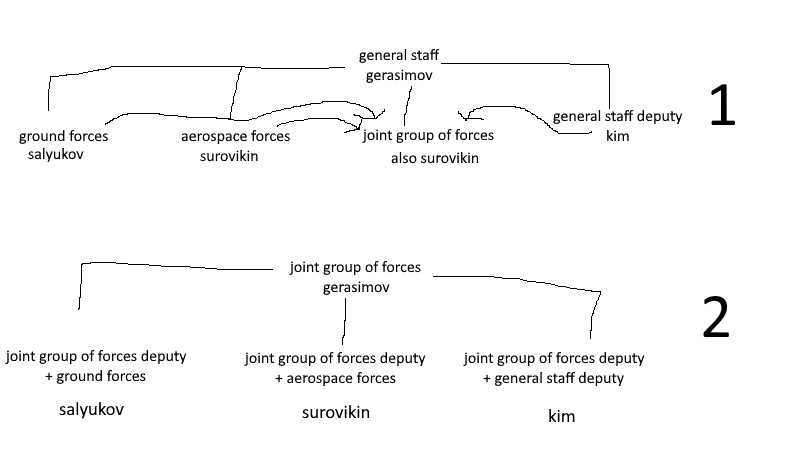

Russian President Vladimir Putin has replaced the commander leading his forces in Ukraine just three months after he handed him the job.

Gen. Valery Gerasimov will take over from Sergei Surovikin, the country’s defense ministry said on Telegram Wednesday, a change that comes as Kyiv warns Moscow is planning a major new offensive after months of battlefield setback.

The above is a misinterpretation of a simple naming change.

Neither was Surovkin pushed aside or demoted nor was Gerasimov promoted to a new job. Surovkin will continue to run the theater force in Ukraine. This move did not change command responsibilities but lifted the importance of the whole operation by making it the highest military commander’s priority.

On 10 January 2022, in the late afternoon, official media sources of the Russian Wagner PMC stated that the city of Soledar had been captured by Russian units.

Soledar was one of the key points of defence of the AFU in the East of Ukraine. The city is home to Europe’s largest salt production facility.

Evgeny Prigoggin, head of the Wagner PMC, announced: “Wagner PMC units have taken control of the entire territory of Soledar. A cauldron has been formed in the centre of the city, where urban fighting is taking place. The number of prisoners will be announced tomorrow. I should like to stress once again that no units other than those of the Wagner Cheka were involved in the storming of Soledar.”

Prigozhin himself was also in the ranks of his warriors in Soledar.

Prigozhin and his soldiers stand at the Salt Mine Museum, which is already closer to the western outskirts of Soledar, confirming full control of the town.

It is currently known that the city, for the most part including the centre, was occupied by Wagner PMC assault groups. The PMC units took all the dominant heights around the city, including Yurchina Mountain, taking direct fire control of the AFU supply roads and outposts. Several hundred more Ukrainian soldiers reportedly remain in the city.

A mopping-up of the city is underway.

The active phase of fighting for Soledar lasted more than four months, but the Ukrainian Armed Forces’ defences were resistant to regular army units and they were subsequently withdrawn from the front line. It took the Wagner Group just over two weeks to take the city directly.

**********

Additional reports:

Prigozhin left salt in Soledar: "… so that America does not think that we are fighting for it." pic.twitter.com/PuUMEyzxkK

Before we get to the sanctions front, here’s a brief update on the developments in the fighting at Soledar near Bakhmut in the Donbass. It’s sounding like the Russian forces have achieved some sort of breakthrough that significantly advances the slow encirclement of Bakhmut itself. Zelensky’s top adviser, Arestovich, has said: “We are on the defensive, they are advancing.”

This afternoon the reporting on the fighting at Soledar is hot and heavy. Soledar is just north of Bakhmut in the Donbass and secures the northern approaches to Bakhmut. The fall of Soledar will therefore place Ukrainian forces in Bakhmut in even more jeopardy. Reports indicate that Soledar has basically fallen, while pockets of Ukrainian and possibly Polish troops remain trapped in the area. The following tweets are not comprehensive nor authoritative, merely typical of reporting:

In Soledar, retreating units of the AFU left Polish mercenaries at the mercy of fate! Right now in Soledar, there is a collapse, where Ukrainians running and they forget to take foreign soldiers with them, said Ivan Filiponenko official representative of People's Militia of LPR. pic.twitter.com/03m4WCiRHF

In the following discussion—all 21 minutes of which is quite interesting—Douglas Macgregor asserts again what he has been saying for about a week. The Ukrainian forces in the south are crumbling, having been stripped of their best units which have been sent to Bakhmut. I take that reference to refer to the areas in the north of the Zaporozhye Oblast, where Ukraine had been building up forces for an offensive toward Melitopol:

The significance of what Macgregor is saying is that Russia has built up a very significant force in Zaporozhye and could open up an avenue for a relatively quick advance to the north, trapping the major portion of Ukrainian forces in the Donbass area.

Now, on to the sanctions front. Yesterday, Alex Mercouris remarked that Japan has been basically ignoring the sanctions regime and continues to import huge amounts of oil and gas from Russia. I’m not sure exactly where the Russian oil and gas is coming from. Russian oil from the Arctic is currently transported by tankers to China and India, but there are other possibilities. So, when I saw this item my interest was sparked:

Russia has managed to restore oil output at its Sakhalin-1 project after struggling with production following the exit of previous operator Exxon Mobil due to sanctions.https://t.co/k7HF7iiYq7

Japan has joint energy projects with Russia in the Sakhalin region, which it has continued despite the sanctions. Sakhalin lies directly north of Japan’s northern island of Hokkaido, and prior to WW2 was split in half between Russia and Japan:

The growth is being driven by high global energy prices

Trade between Russia and Japan saw an annual increase of 10% in the first 11 months of 2022 despite Ukraine-related sanctions introduced against Moscow by the West, according to estimates made by TASS, based on Japanese trade statistics.

In monetary terms, bilateral trade reportedly amounted to 2.365 trillion yen (some $18 billion).

…

Russia, one of the world’s biggest oil producers and exporters, remains one of the major suppliers of liquefied natural gas (LNG) to Japan. The sanctions-hit country accounts for about 9% of Japanese imports of the fuel. Russian gas accounts for 3% of electricity generation in Japan.

Nevertheless:

Tokyo reduced purchases of Russian crude to almost zero in July and August. Moreover, Japan has joined the oil price cap scheme adopted by the Group Seven nations last month. The mechanism bans Russian oil cargoes that are traded above $60 per barrel from getting key services provided by Western companies, including insurance. The price ceiling may be revised depending on market conditions.

Hypocritical? Realistic? Both? But it doesn’t bode well for the economic war against Russia. The US is a long way off from Japan. Although US bases are near, supply lines are very long. China and Russia are very near.

So here’s what Alex Krainer is talking about today:

US military is working hard on “setting the theater” for war on China, emulating the success it’s had in Ukraine.

I don’t know whether we’ll have a war on China this year, but it does appear that the western empire, led by the United States, is preparing for it in earnest. On Sunday, 10 January, Lieutenant General James Bierman, the commanding general of the Third Marine Expeditionary Force and of Marine Forces Japan gave an interview to the Financial Times in which he said that his command is working hard to replicate the empire’s military success in Ukraine.

I still want to believe that all this crazy talk will end up going nowhere, thwarted by the pressure of events in the Real World.

Is JPM Solvent? If not, what about Citi? Is anyone solvent?

An available-for-sale security (AFS) is a debt or equity security purchased with the intent of selling before it reaches maturity or holding it for a long period should it not have a maturity date.

Accounting standards require companies classify any investments in debt or equity securities when they are purchased in one of the following categories:

As interest rates have risen in response to Federal Reserve policies, the AFS securities have seen significant unrealized losses on their bond portfolios.

The change in bond portfolios has disrupted the bank M&A market and inflicted pressures on large commercial banks.

Generally accepted accounting principles (GAAP) require unrealized losses (or unrealized gain in a different environment) on AFS securities to be reflected on the balance sheet as accumulated other comprehensive income (AOCI).

AOCI losses have been dramatically rising over the past year.

Rising interest rate increases, coupled with soft loan demand and desire for yields, leave banks holding large investment portfolios.

These securities are often weighted down by longer maturities, which means significant, unrealized, losses. These unrealized losses have suppressed bank M&A activity.

The question is to what extent is the rising AOCI impacting large bank solvency.

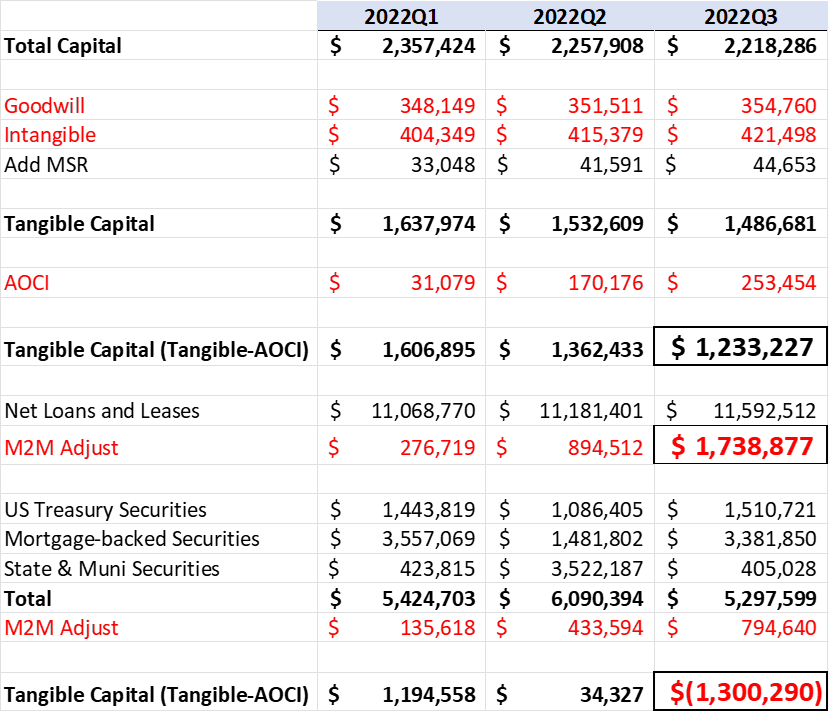

November 28, 2022 | Watching the Buy Side Pivot Platoon rev up for a new surge of asset allocation into large cap bank stocks, we remind readers of The Institutional Risk Analyst that US depositories currently are not particularly cheap, in nominal or real terms. In fact, in a stressed scenario, the liabilities of banks exceed the value of the assets by over $1 trillion, the classic definition of insolvency.

Once you adjust reported book value for the asset price inflation & now deflation of the QE/QT roller coaster ride, it is fair to ask: Just where is the value? If we told you that the capitalization of the industry was negative by over $1 trillion at the end of Q2 2022, would you still buy bank stocks for your clients? Let’s have a look at industry paragon JPMorgan Chase (JPM) just for giggles, but first we’ll start off with the industry view.

At the end of Q2 2022, the US banking industry had $2.2 trillion in total capital. That is, book equity. But much of total capital is not tangible, which is why regulators use Tier 1 Capital as the base measure for solvency. The legal definition of Tier 1 Capital, which excludes many items we discuss below, is found at 12 CFR Part 324 of the federal banking regulations.

Specifically, the law:

“requires that several items be fully deducted from common equity tier 1 capital, such as goodwill, deferred tax assets (DTAs) that arise from net operating loss and tax credit carry-forwards, other intangible assets (except for mortgage servicing assets (MSAs)), certain DTAs arising from temporary differences (temporary difference DTAs), gains on sale of securitization exposures, and certain investments in another financial institution’s capital instruments. Additionally, management must adjust for unrealized gains or losses on certain cash flow hedges.”

12 CFR Part 324

Of note, when adopted in 2015, CFR Part 324 allowed all non-advanced approach institutions (aka “little banks”) to make a permanent, one-time opt-out election, enabling them to calculate regulatory capital without AOCI. At the time, accumulated other comprehensive income was a minor entry on bank balance sheets and income statements, minor as in the footnotes. In the age of QE, however, AOCI is now a much bigger deal, but still is dwarfed by how QE has caused unrealized losses on bank balance sheets.

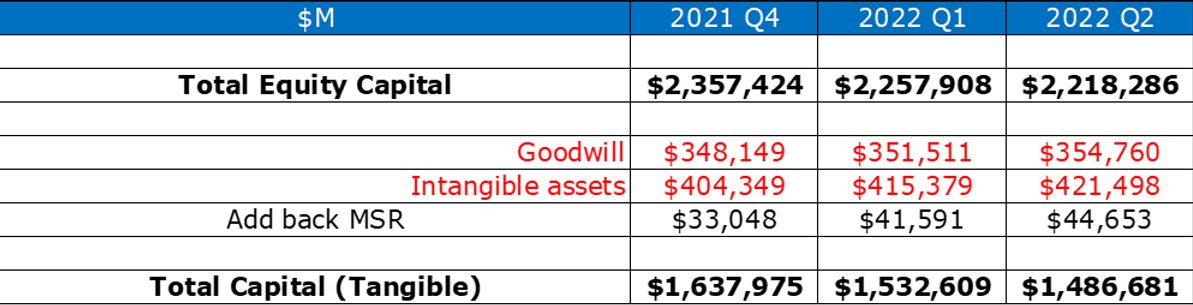

So, let’s begin the fun with the fire-sale calculation we perform using the aggregate data from the FDIC. We start with total capital, the broadest definition of bank equity. We then subtract the goodwill and all of the intangibles, but add back in the mortgage servicing assets just to be nice. Once you see the result of the analysis, you’ll understand why we say “nice” regards adding back the MSRs.

U.S. Banking Industry

Source: FDIC

Notice that tangible capital dropped by several hundred billion in three quarters since Q4 2021. As we’ve noted earlier, the large banks led by JPM plateaued in Q3 2022 in terms of AOCI, mostly through sales of assets and transfers into portfolio to be “held to maturity.” But the risk remains. MSR prices have likewise softened since June. Regulators refer to “assets” rather than rights because sometimes mortgage servicing can become a liability, particularly in the government market.

Thanks to QE and now QT, all sorts of assets have become negative return propositions for banks and nonbanks alike. If the coupon pays less than the funding costs, you’re losing money. Just ask Jerome Powell about the return on the Fed’s SOMA portfolio. Below we take the analysis through adding the net gain or loss reported in AOCI.

U.S. Banking Industry

Source: FDIC

So just subtracting the basics for Tier 1 capital leverage, including taking out the AOCI, we have almost cut Q2 2022 industry capital in half. And we have not even arrived at the fun part, which involves estimating the mark-to-market losses on loans and securities held in portfolio caused by the rapid increase in interest rates by the FOMC.

Even if the bank holds these low-coupon assets created during 2020-2021 in portfolio to maturity, cash flow losses and poor returns could eventually force a sale. This is why people who prattle on about how well capitalized are US banks are just showing their ignorance.

The table below shows our conservative M2M adjustment for the last three quarters on the almost $12 trillion in total loans and leases owned by banks. We adjust Q4 2021 by 2.5%, Q1 2022 by 8% of total loans and leases, and 15% of total loans and leases in Q2 2022 to approximate the low-end of M2M losses due to the rapid increase in interest rates in 2022.

U.S. Banking Industry

Source: FDIC

As you can see, the industry is already insolvent in Q2 2022 with the adjustment to the loan portfolio, which may be significantly underwater by next year. GAAP allows owners of assets held to maturity to ignore mark-to-market losses so long as they have the capacity and the intent to do so.

So, do you sell the 2% and 3% coupon loans and securities at a loss and buy some 8% and 9% loans coupons? Yes you do, eventually. This is how M2M becomes available for sale (AFS) “gradually, then suddenly” to recall Ernest Hemingway’s 1926 novel, The Sun Also Rises.

The final part of the analysis is to apply the adjustments above to the $5 trillion bank securities portfolio. The result is another $700 billion in potential M2M losses as of the end of Q2 2022 and a picture of the US banking industry that is a good bit less positive than the conventional wisdom.

U.S. Banking Industry

Source: FDIC

The value of the FDIC data is that they track all of the AOCI even if the banks do not need to add or subtract the balance from regulatory capital. The fact that the US banking industry had $1.3 trillion more in potential M2M losses that capital at Q2 2022 should put to rest any doubts that QE was too much funny money for too long. Notice that none of the economics reporters who cover the Fed ever ask about the impact of QE on the banking system.

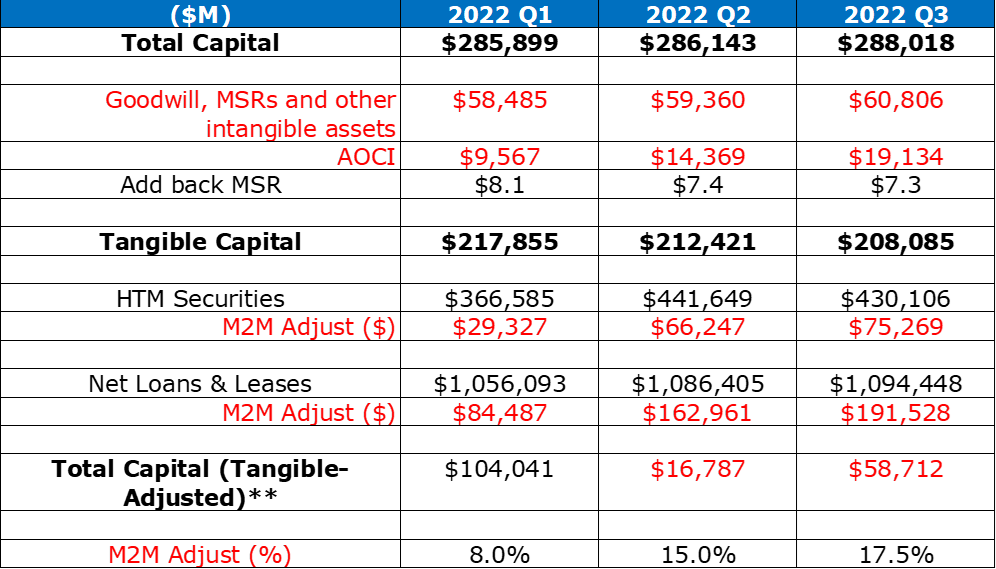

So now if we turn to JPM, which is one of the better managed banks in the US, the results are better than the industry as a whole but the bank still had a negative capital position at the end of Q2 2022 to the tune of -$16 billion in capital. The capital deficit increased to -$58 billion when we increased the M2M adjustment to 17.5% haircut in our stressed scenario.

JPMorgan Chase

Source: FDIC, Edgar

Don’t hold your breath waiting for Fed Chairman Jerome Powell to address the issue of bank solvency at the next FOMC press conference. First QE and now QT has injected such excessive levels of volatility into the prices of assets — all assets — that the value of capital has been compromised. Suffice to say that if the FOMC continues to raise interest rates above current levels, then we think that the issue of bank solvency may be front-and-center by next summer.

*****

They say the first rule of holes is if you find yourself in one, stop digging.

With that in mind, here’s Chris this morning regarding current TBA bids:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}