A French journalist who returned from Ukraine after arriving with volunteer fighters told broadcaster CNews that Americans are directly “in charge” of the war on the ground.

The assertion was made by Le Figaro senior international correspondent Georges Malbrunot.

Malbrunot said he had accompanied French volunteer fighters, two of whom had previously fought against ISIS.

“I had the surprise, and so did they, to discover that to be able to enter the Ukrainian army, well it’s the Americans who are in charge,” said Malbrunot.

French reporter returning from Ukraine "Americans are directly in charge of the war on the ground." pic.twitter.com/m5yr7far6N

Adding that he and the volunteers “almost got arrested” by the Americans, who asserted they were in charge, the journalist then revealed that they were forced to sign a contract “until the end of the war.”

“And who is in charge? It’s the Americans, I saw it with my own eyes,” said Malbrunot, adding, “I thought I was with the international brigades, and I found myself facing the Pentagon.”

Malbrunot also mentioned America providing Ukraine with switchblade suicide drones, something highlighted by Defense Secretary Lloyd Austin in a tweet that revealed Ukrainian soldiers were being trained to use the devices in Biloxi, Mississippi.

U.S. Defense Secretary Lloyd Austin speaks to Ukrainian soldiers training on switchblade drones in Biloxi, Mississippi before they return today to defend their country pic.twitter.com/awUaoySgeH

Citing a French intelligence source, Malbrunot also tweeted that British SAS units “have been present in Ukraine since the beginning of the war, as did the American Deltas.”

Russia is apparently well aware of the “secret war” being waged in Ukraine by foreign commandos who have been in the region since February.

Both the United States and the UK have publicly asserted that there won’t be “boots on the ground” in Ukraine, but apparently there has been a US-UK military presence since the start of the war.

“Polls showed in the run up to the war the overwhelming majority of Americans wanted our government to stay out of it but our leaders know best and are more than happy to risk World War III in defense of Ukraine’s puppet regime,” writes Chris Menahan.

Western Dissent from US/NATO Policy on Ukraine is Small, Yet the Censorship Campaign is Extreme

Preventing populations from asking who benefits from a protracted proxy war, and who pays the price, is paramount. A closed propaganda system achieves that.

The Google logo seen on a cellphone with a background saying ‘censored’. (Photo by Guillaume Payen/SOPA Images/LightRocket via Getty Images)

If one wishes to be exposed to news, information or perspective that contravenes the prevailing US/NATO view on the war in Ukraine, a rigorous search is required. And there is no guarantee that search will succeed. That is because the state/corporate censorship regime that has been imposed in the West with regard to this war is stunningly aggressive, rapid and comprehensive.

On a virtually daily basis, any off-key news agency, independent platform or individual citizen is liable to be banished from the internet. In early March, barely a week after Russia’s invasion of Ukraine, the twenty-seven nation European Union — citing “disinformation” and “public order and security” — officially banned the Russian state-news outlets RT and Sputnik from being heard anywhere in Europe. In what Reuters called “an unprecedented move,” all television and online platforms were barred by force of law from airing content from those two outlets. Even prior to that censorship order from the state, Facebook and Google were already banning those outlets, and Twitter immediately announced they would as well, in compliance with the new EU law.

But what was “unprecedented” just six weeks ago has now become commonplace, even normalized. Any platform devoted to offering inconvenient-to-NATO news or alternative perspectives is guaranteed a very short lifespan. Less than two weeks after the EU’s decree, Google announced that it was voluntarily banning all Russian-affiliated media worldwide, meaning Americans and all other non-Europeans were now blocked from viewing those channels on YouTube if they wished to. As so often happens with Big Tech censorship, much of the pressure on Google to more aggressively censor content about the war in Ukraine came from its own workforce: “Workers across Google had been urging YouTube to take additional punitive measures against Russian channels.”

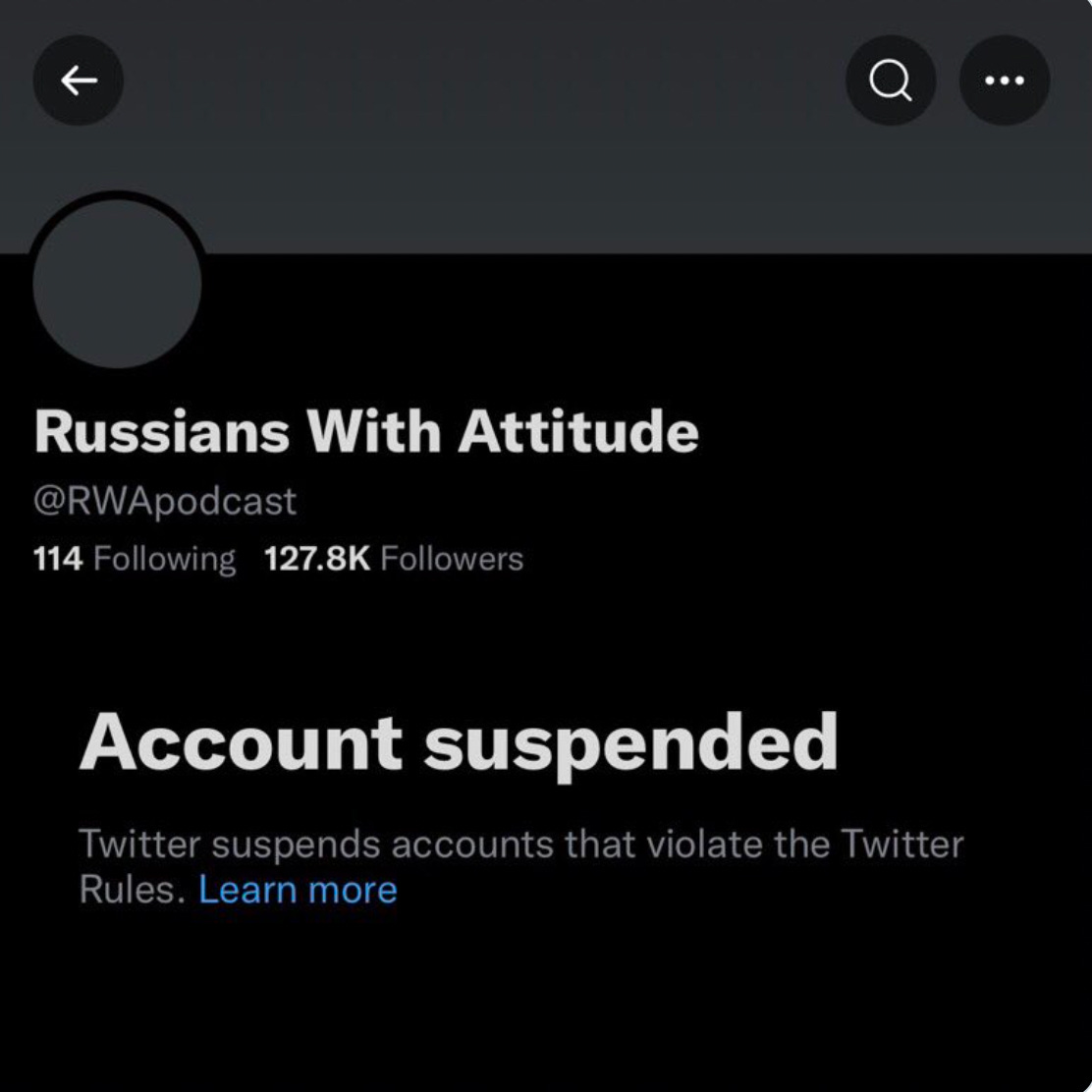

So prolific and fast-moving is this censorship regime that it is virtually impossible to count how many platforms, agencies and individuals have been banished for the crime of expressing views deemed “pro-Russian.” On Tuesday, Twitter, with no explanation as usual, suddenly banned one of the most informative, reliable and careful dissident accounts, named “Russians With Attitude.” Created in late 2020 by two English-speaking Russians, the account exploded in popularity since the start of the war, from roughly 20,000 followers before the invasion to more than 125,000 followers at the time Twitter banned it. An accompanying podcast with the same name also exploded in popularity and, at least as of now, can still be heard on Patreon.

What makes this outburst of Western censorship so notable — and what is at least partially driving it — is that there is a clear, demonstrable hunger in the West for news and information that is banished by Western news sources, ones which loyally and unquestioningly mimic claims from the U.S. government, NATO, and Ukrainian officials.

As The Washington Postacknowledged when reporting Big Tech’s “unprecedented” banning of RT, Sputnik and other Russian sources of news: “In the first four days of Russia’s invasion of Ukraine, viewership of more than a dozen Russian state-backed propaganda channels on YouTube spiked to unusually high levels.”

Note that this censorship regime is completely one-sided and, as usual, entirely aligned with U.S. foreign policy. Western news outlets and social media platforms have been flooded with pro-Ukrainian propaganda and outright lies from the start of the war. A New York Timesarticle from early March put it very delicately in its headline: “Fact and Mythmaking Blend in Ukraine’s Information War.” Axios was similarly understated in recognizing this fact: “Ukraine misinformation is spreading — and not just from Russia.” Members of the U.S. Congress have gleefully spread fabrications that went viral to millions of people, with no action from censorship-happy Silicon Valley corporations. That is not a surprise: all participants in war use disinformation and propaganda to manipulate public opinion in their favor, and that certainly includes all direct and proxy-war belligerents in the war in Ukraine.

Yet there is little to no censorship — either by Western states or by Silicon Valley monopolies — of pro-Ukrainian disinformation, propaganda and lies. The censorship goes only in one direction: to silence any voices deemed “pro-Russian,” regardless of whether they spread disinformation. The “Russians With Attitude” Twitter account became popular in part because they sometimes criticized Russia, in part because they were more careful with facts and viral claims that most U.S. corporate media outlets, and in part because there is such a paucity of outlets that are willing to offer any information that undercuts what the U.S. Government and NATO want you to believe about the war.

Their crime, like the crime of so many other banished accounts, was not disinformation but skepticism about the US/NATO propaganda campaign. Put another way, it is not “disinformation” but rather viewpoint-error that is targeted for silencing. One can spread as many lies and as much disinformation as one wants provided that it is designed to advance the NATO agenda in Ukraine (just as one is free to spread disinformation provided that its purpose is to strengthen the Democratic Party, which wields its majoritarian power in Washington to demand greater censorship and commands the support of most of Silicon Valley). But what one cannot do is question the NATO/Ukrainian propaganda framework without running a very substantial risk of banishment.

It is unsurprising that Silicon Valley monopolies exercise their censorship power in full alignment with the foreign policy interests of the U.S. Government. Many of the key tech monopolies — such as Google and Amazon — routinely seek and obtain highly lucrativecontracts with the U.S. security state, including both the CIA and NSA. Their top executives enjoy very close relationships with top Democratic Party officials. And Congressional Democrats have repeatedly hauled tech executives before their various Committees to explicitly threaten them with legal and regulatory reprisals if they do not censor more in accordance with the policy goals and political interests of that party.

But one question lingers: why is there so much urgency about silencing the small pockets of dissenting voices about the war in Ukraine? This war has united the establishment wings of both parties and virtually the entire corporate media with a lockstep consensus not seen since the days and weeks after the 9/11 attack. One can count on both hands the number of prominent political and media figures who have been willing to dissent even minimally from that bipartisan Washington consensus — dissent that instantly provokes vilification in the form of attacks on one’s patriotism and loyalties. Why is there such fear of allowing these isolated and demonized voices to be heard at all?

The answer seems clear. The benefits from this war for multiple key Washington power centers cannot be overstated. The billions of dollars in aid and weapons being sent by the U.S. to Ukraine are flying so fast and with such seeming randomness that it is difficult to track. “Biden approves $350 million in military aid for Ukraine,” Reuters said on February 26; “Biden announces $800 million in military aid for Ukraine,” announced The New York Times on March 16; on March 30, NBC’s headline read: “Ukraine to receive additional $500 million in aid from U.S., Biden announces”; on Tuesday, Reuters announced: “U.S. to announce $750 million more in weapons for Ukraine, officials say.” By design, these gigantic numbers have long ago lost any meaning and provoke barely a peep of questioning let alone objection.

It is not a mystery who is benefiting from this orgy of military spending. On Tuesday, Reuters reported that “the Pentagon will host leaders from the top eight U.S. weapons manufacturers on Wednesday to discuss the industry’s capacity to meet Ukraine’s weapons needs if the war with Russia lasts years.” Among those participating in this meeting about the need to increase weapons manufacturing to feed the proxy war in Ukraine is Raytheon, which is fortunate to have retired General Lloyd Austin as Defense Secretary, a position to which he ascended from the Raytheon Board of Directors. It is virtually impossible to imagine an event more favorable to the weapons manufacturer industry than this war in Ukraine:

Demand for weapons has shot up after Russia’s invasion on Feb. 24 spurred U.S. and allied weapons transfers to Ukraine. Resupplying as well as planning for a longer war is expected to be discussed at the meeting, the sources told Reuters on condition of anonymity. . .

Resupplying as well as planning for a longer war is expected to be discussed at the meeting. . . . The White House said last week that it has provided more than $1.7 billion in security assistance to Ukraine since the invasion, including over 5,000 Javelins and more than 1,400 Stingers.

This permanent power faction is far from the only one to be reaping benefits from the war in Ukraine and to have its fortunes depend upon prolonging the war as long as possible. The union of the U.S. security state, Democratic Party neocons, and their media allies has not been riding this high since the glory days of 2002. One of MSNBC’s most vocal DNC boosters, Chris Hayes, gushed that the war in Ukraine has revitalized faith and trust in the CIA and intelligence community more than any event in recent memory — deservedly so, he said: “The last few weeks have been like the Iraq War in reverse for US intelligence.” One can barely read a mainstream newspaper or watch a corporate news outlet without seeing the nation’s most bloodthirsty warmongering band of neocons — David Frum, Bill Kristol, Liz Cheney, Wesley Clark, Anne Applebaum, Adam Kinzinger — being celebrated as wise experts and heroic warriors for freedom.

This war has been very good indeed for the permanent Washington political and media class. And although it was taboo for weeks to say so, it is now beyond clear that the only goal that the U.S. and its allies have when it comes to the war in Ukraine is to keep it dragging on for as long as possible. Not only are there no serious American diplomatic efforts to end the war, but the goal is to ensure that does not happen. They are now saying that explicitly, and it is not hard to understand why.

The benefits from endless quagmire in Ukraine are as immense as they are obvious. The military budget skyrockets. Punishment is imposed on the arch-nemesis of the Democratic Party — Russia and Putin — while they are bogged down in a war from which Ukrainians suffer most. The citizenry unites behind their leaders and is distracted

Russia’s current account surplus, the broadest measure of trade, more than doubled in the first quarter of 2022 from the same period last year amid soaring oil and gas prices, according to data from the Russian central bank cited by Bloomberg.

Russia—which continued its oil and gas sales in Q1 at the highest prices in years—saw its current account surplus jump by more than 2.5 times from last year’s first quarter to $58.2 billion from $22.5 billion.

Russian revenues from oil and gas sales soared in the first quarter, while imports plunged amid companies withdrawing from Russia over Vladimir Putin’s invasion of Ukraine. This resulted in a major surplus in the Russian trade of goods and services.

“Export inflows stayed practically the same, but imports dropped sharply because of logistics limits and restrictions imposed by Western countries,” Russian Finance Minister Anton Siluanov told local newspaper Izvestia in an interview published during the weekend.

Despite the widespread global condemnation of the Russian invasion of Ukraine, Russia continued to sell its oil and gas to its key export markets in the first quarter. Asian buyers China and India continued buying Russian oil at hefty discounts, while Europe continued buying natural gas. Europe also continued buying Russian oil for most of Q1, although many European majors said in early March that they would not trade with spot Russian crude and oil products after the invasion of Ukraine.

Russia expects to earn additional oil and gas revenues equivalent to $9.6 billion (798.4 billion Russian rubles) this month, its finance ministry said last week.

Despite the self-sanctioning of many European buyers of Russian oil, Moscow continues to export its oil, and Europe continues to pay for and import Russian natural gas.

On Friday, the EU said it would be imposing a ban on imports of coal and other solid fossil fuels from Russia as of August 2022 as part of the fifth round of EU sanctions against Russia over its invasion of Ukraine. The EU is currently discussing sanctions on Russian oil, although a consensus seems weeks away as the bloc is split over an oil embargo.

You Know Things Are Bad When Saudi State TV Mocks Joe Biden

You know things are bad when Saudi television mocks the president of the United States in a SNL-style spoof. A state-run TV station featured a comedy sketch depicting Joe Biden attempting to address the Ukraine crisis, but he’s seen wandering away from the podium and falling asleep mid-sentence, while also being constantly prodded by his VP over what to say given he struggles to remember basic names and information.

The sketch went viral after it hit social media on Monday, and comes after last month Saudi Crown Prince Mohammed bin Salman reportedly rejected attempts by the White House to set up a phone call between he and Joe Biden, at a moment the US is urging the Saudis to ramp up oil output. Watch the brief segment above.

The sketch from the show Studio 22 begins with “Biden” barely aware of his surroundings as “Harris” tries to pull him back on stage in order to stutter through some short sentences, as The Jerusalem Postdescribed further:

The overarching theme of the clip is that President Biden is old. The character is obviously unaware of his surroundings and prone to falling asleep mid-sentence. Consequently, the audience sees Harris, played by a male actor in drag, telling the President what to say and do. At the end of the clip, Biden finally falls asleep and Harris literally puppets his unconscious body, screaming, “clap for the president!”

The clip was an obvious and perhaps over-the-top attempt at highlighting the 79-year old president’s cognitive decline in old age, also after a series of recent remarks on Ukraine that the White House had to scramble to walk back. The Saudi spoof included the following dialogue:

BIDEN: Yeah, we gotta talk about the crisis in Africa.”

HARRIS: [taps and whispers again]

BIDEN: Yeah Russia. And I wanna talk about President of Russia–[pauses].

HARRIS: [whispers]

BIDEN: Putin. Putin. Putin! Listen to me, I have [a] very important message to you. The message is [falls asleep and snores].

But just days ago a very real clip of Biden giving a press conference on the White House lawn while standing beside Harris wasn’t too far off from the extremes that the Saudi skit depicted…

BIDEN: "I was in the the foothills of the Himalayas with Xi Jinping, traveling with him, that's when I traveled 17,000 miles when I was Vice President. I don't know that for a fact." pic.twitter.com/hoiGCUGckR

He began by saying “America as a nation can be defined as a single word…”

But then Biden inexplicably drifted off and changed thought entirely, breaking into his own sentence with “…excuse me, I was in the foothills of the Himalayas with Xi Jinping, traveling with him, traveled 17,000 miles when I was Vice President. I don’t know that for a fact.”

And it’s of course unclear what the bizarre Himalaya story was meant to convey. Given the timing and fact that the Saudi skit was produced days after that last Friday White House speech, the Saudis were clearly taking aim at the incident, using it to highlight current lack of faith in Biden as a global leader during the Ukraine crisis.

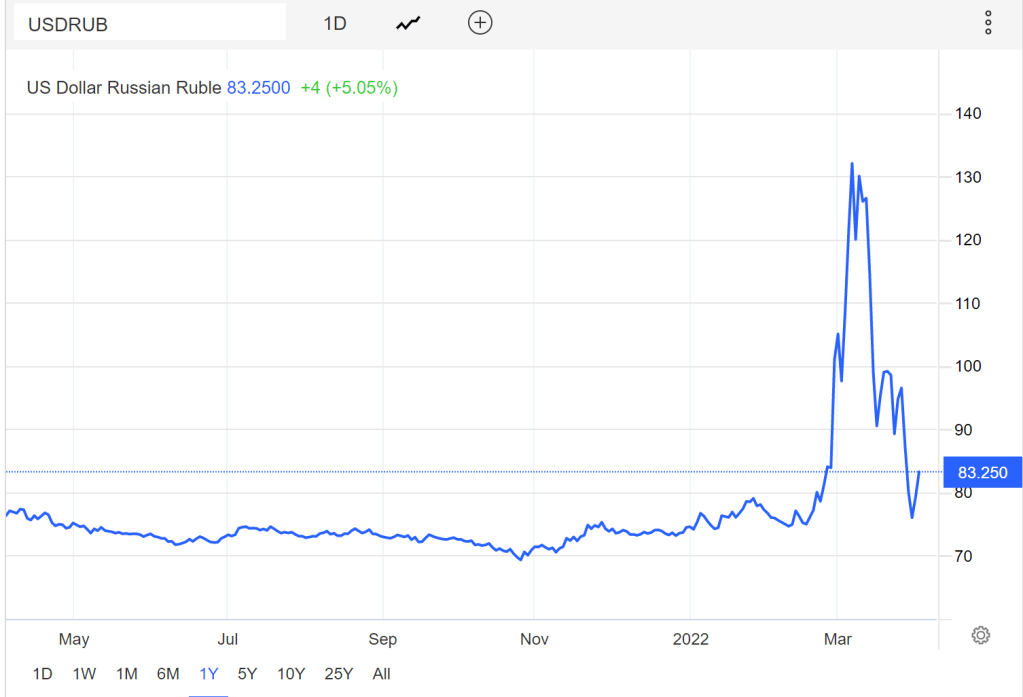

Probably the most current metric for how Russia is doing is the Ruble. So far, it is holding its own even as Biden sanctions are destroying the EU economy and crippling the US.

We’ll summarize what we know about principal military attack vectors, share Russian/DPR perspective, and end with Scott Ritter’s analysis.

We’re not cheerleaders. But with Western media nothing more than Biden Regime “psyops”, it’s always helpful to see how the other side sees things, plus a little reality check.

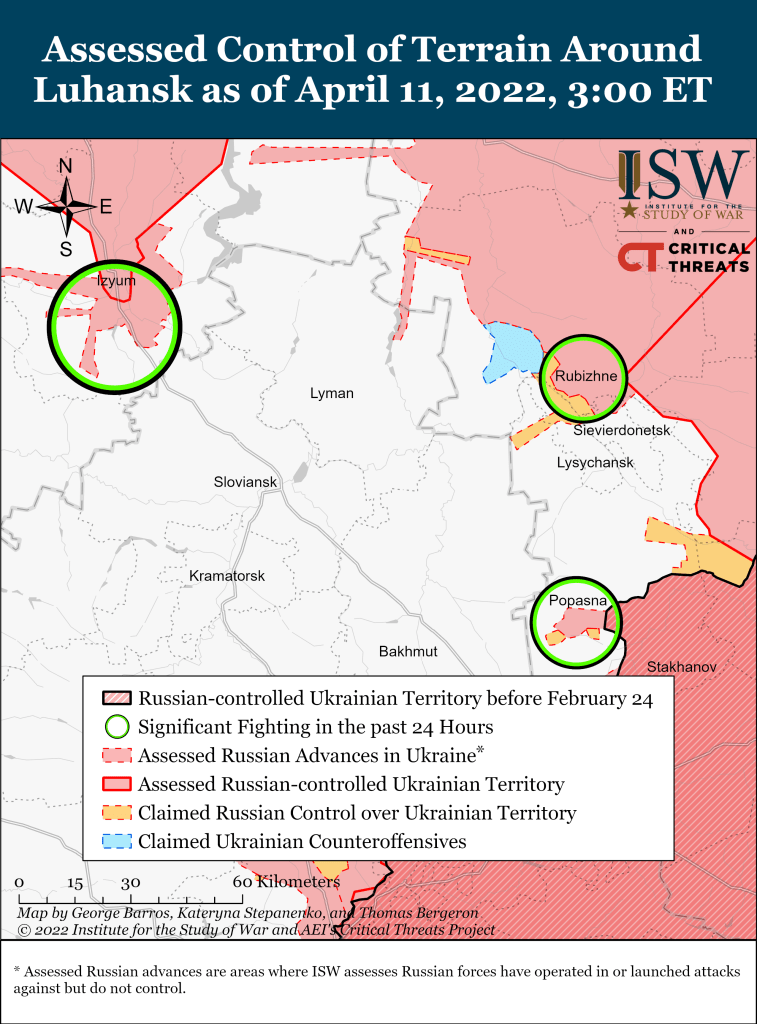

Now to the front which has shifted north and east as the Mariupol ends.

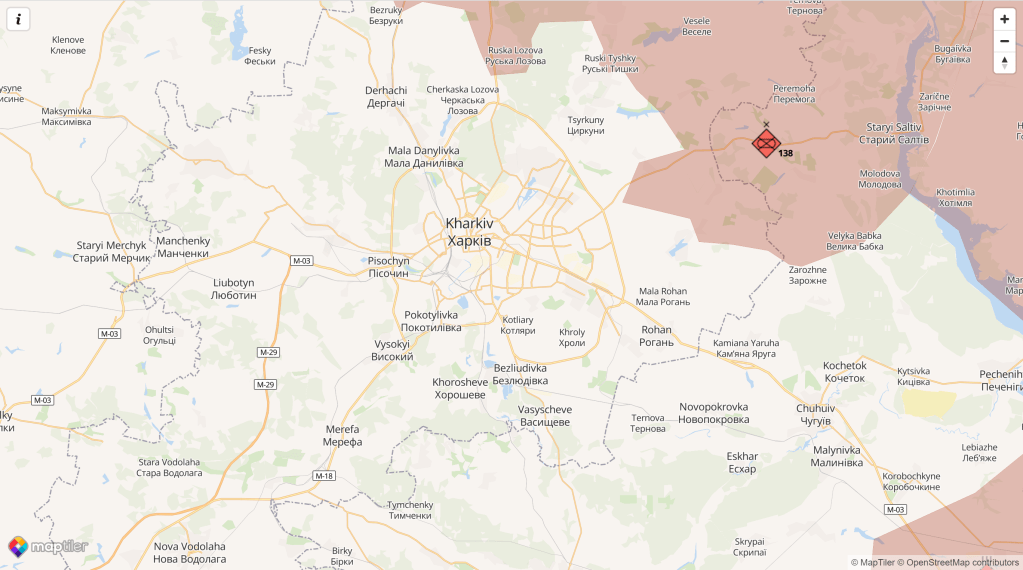

Karkiv

On the right flank of the Russian position is the 138th Separate Guards Motorized Rifle Brigade of the 6th Combined Arms Army (6th CAA). The 138th employs MT-LBV armored personnel carriers and T-72B3 tanks. According to the Finnish newspaper Helsingin Sanomat article, two battle groups of approximately 800 men each from the brigade had been sent to participate in the 2022 Russian invasion of Ukraine.

Here are some T-72s reportedly in the vicinity ot Kharkiv.

Russia completed its withdrawal from Sumy Oblast and additional forces from the 35th Combined Arms Army (CAA) arrived on the Izium axis. 2nd Guards Motorized Rifle DIvision’s (2nd GMRD) 1st Guards Tank Regiment conducted a possible probe south of Izium near Sulyhivka. 1st Guards Tank Army’s remaining combat power may not be enough to achieve a breakthrough without further reinforcements. 35th CAA likely begun to arrive in this sector, with Ukraine’s General Staff noting the arrival of the 38th Seperate Motorized Rifle Brigade.

This appears to be a flank security position for the larger body of troops aimed at IZyum.

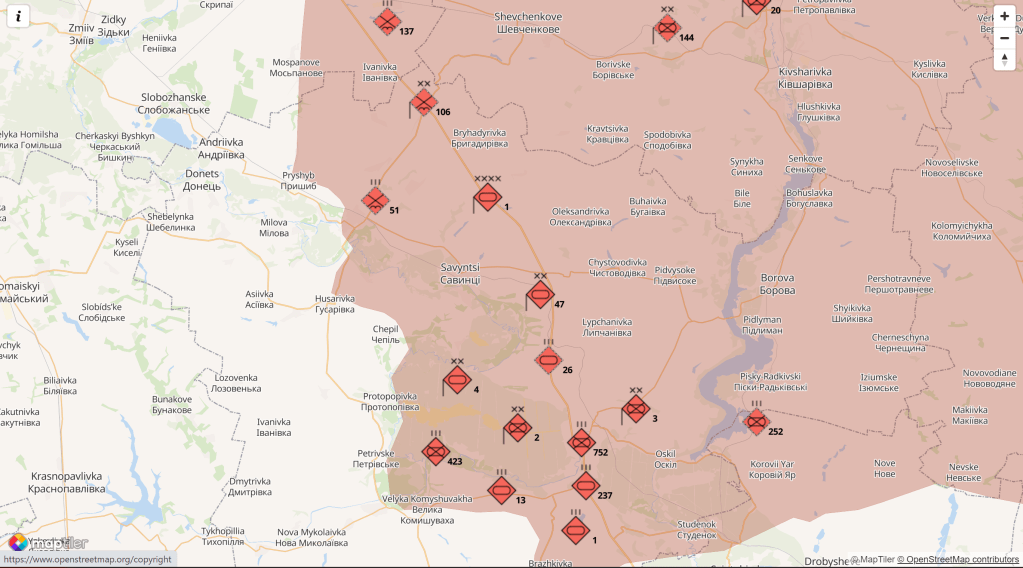

Izyum

The 1st Guards Tank Army is the Russian hammer.

Russian forces will continue reinforcing the Izyum-Slovyansk axis and attempting to advance to and through Slovyansk to encircle Ukrainian forces.

Here we see the bulk of the 1st Guards Tank Army stretched along the vital M-03 road.

More broadly, Russia continued its redeployment of VDV and Eastern Military District forces from Belarus to the Donbas and Kharkiv Oblast. Additional 35th Combined Arms Army (CAA) elements and possibly part of the 76th Guards Air Assault Division arrived at Valuyki and Kup’yans’k. The 35th CAA’s remaining combat capable units will arrive over the next five days, possibly achieving allowing Russia overall to reach a correlation of forces favorable enough to mount an offensive south of Izium. 5th CAA elements have been identified in the Sievierodonetsk area. Kherson has been slightly reinforced by an unidentified naval infantry unit, possibly indicating Russia intends to try to hold it.

But back to the M-03: the primary rail hubs being used to reinforce the Izium axis are Valuyki and Kup’yans’k.

Imperial (black and yellow and white) and St. Andrew (Russian Marines) flags – units heading east

Abrams tank captured by DPR forces on the Eastern front.

As reported by Tass:

“During the day, high-precision land-based missiles hit a battalion command center, three company strongholds, two company tactical groups of the 24th Ukrainian mechanized brigade and a territorial defense brigade, and two place of the deployment of personnel, weapons and military hardware near the settlements of Popasnaya, Novozvanovka, and Zolotoye in the Donetsk region,” he said, adding that up to 300 Ukrainian militants were killed and more than 50 armored combat vehicles were destroyed.

Mariupol and the Russian/DPR Point of View

Finally, Scott Ritter on the Battle of Donbass – the “Double Envelopment”

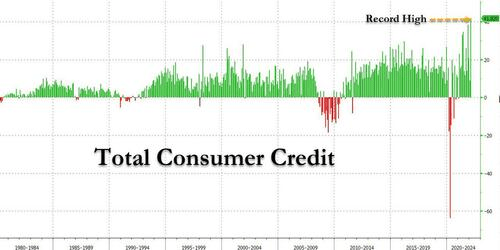

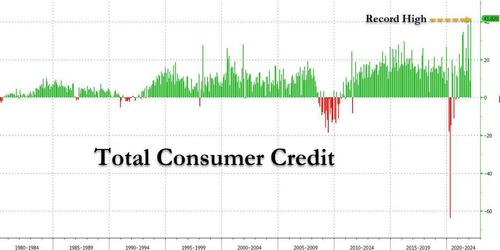

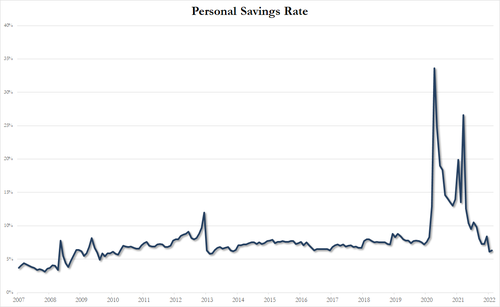

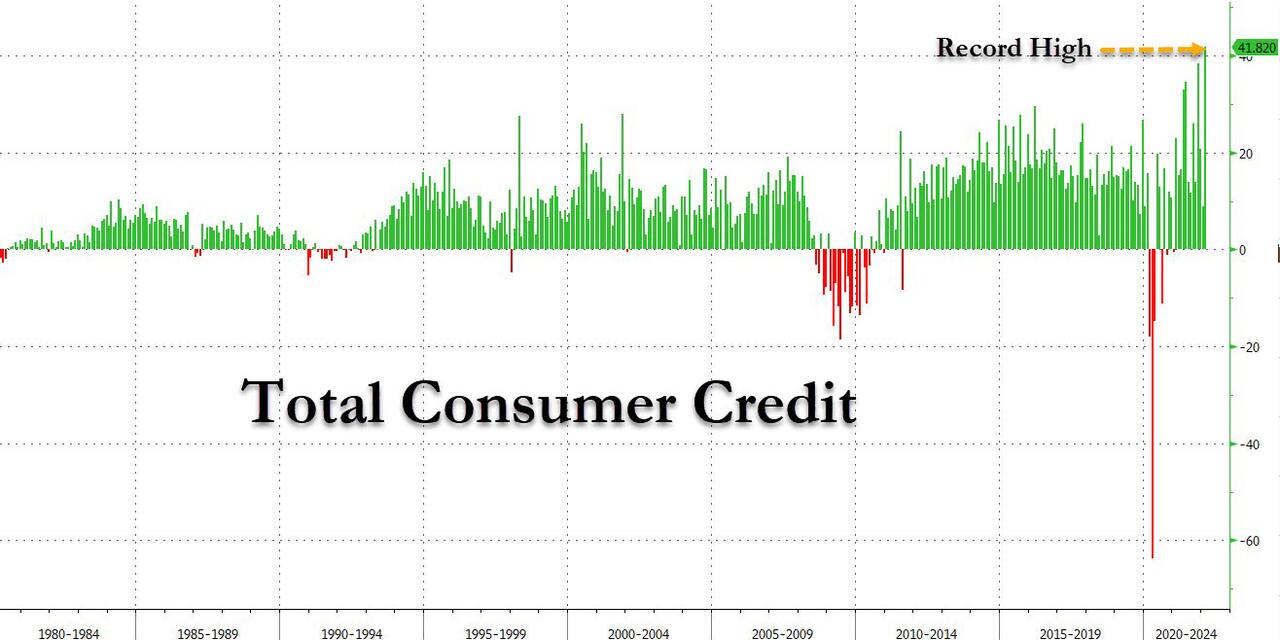

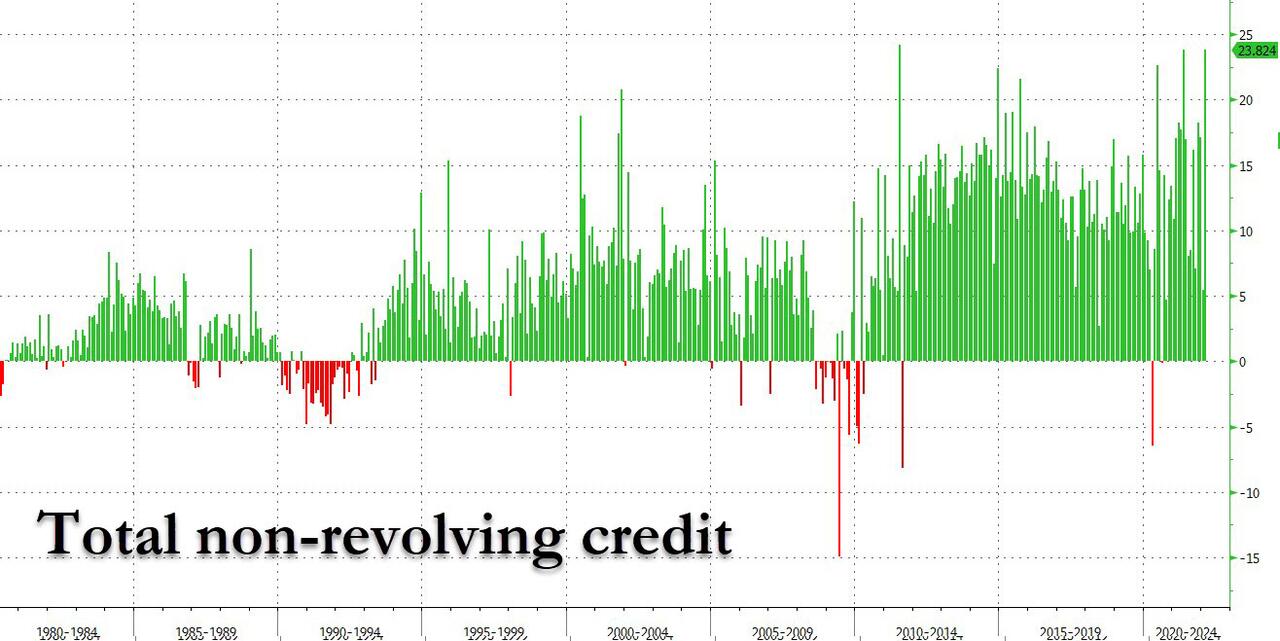

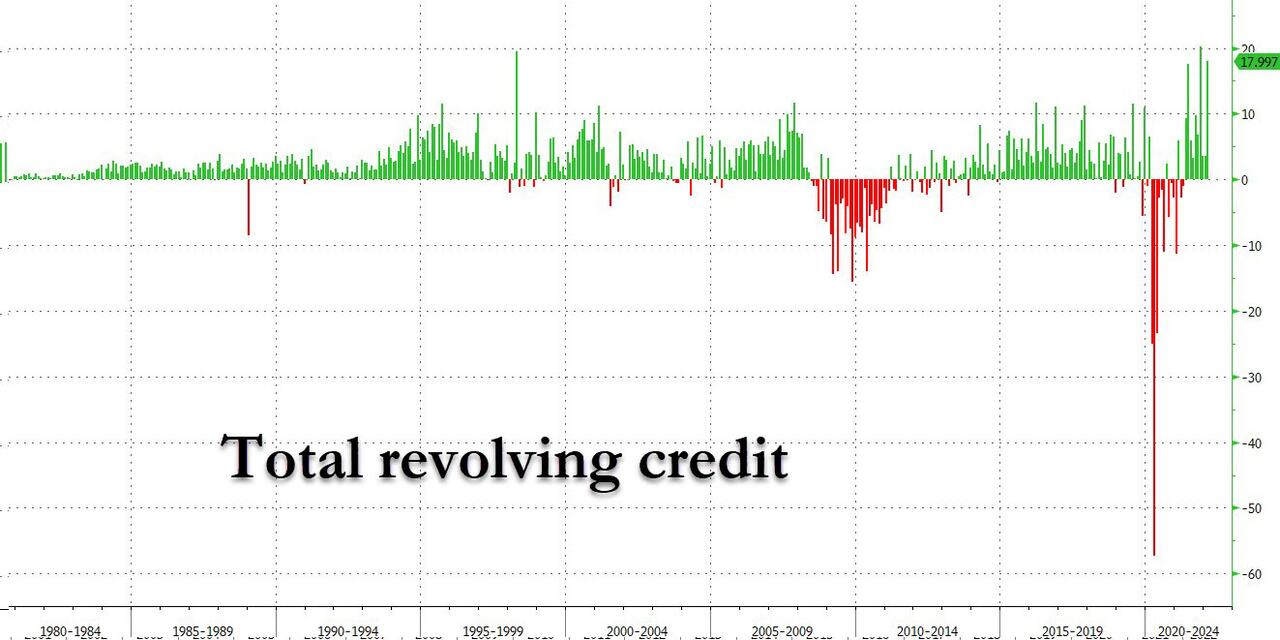

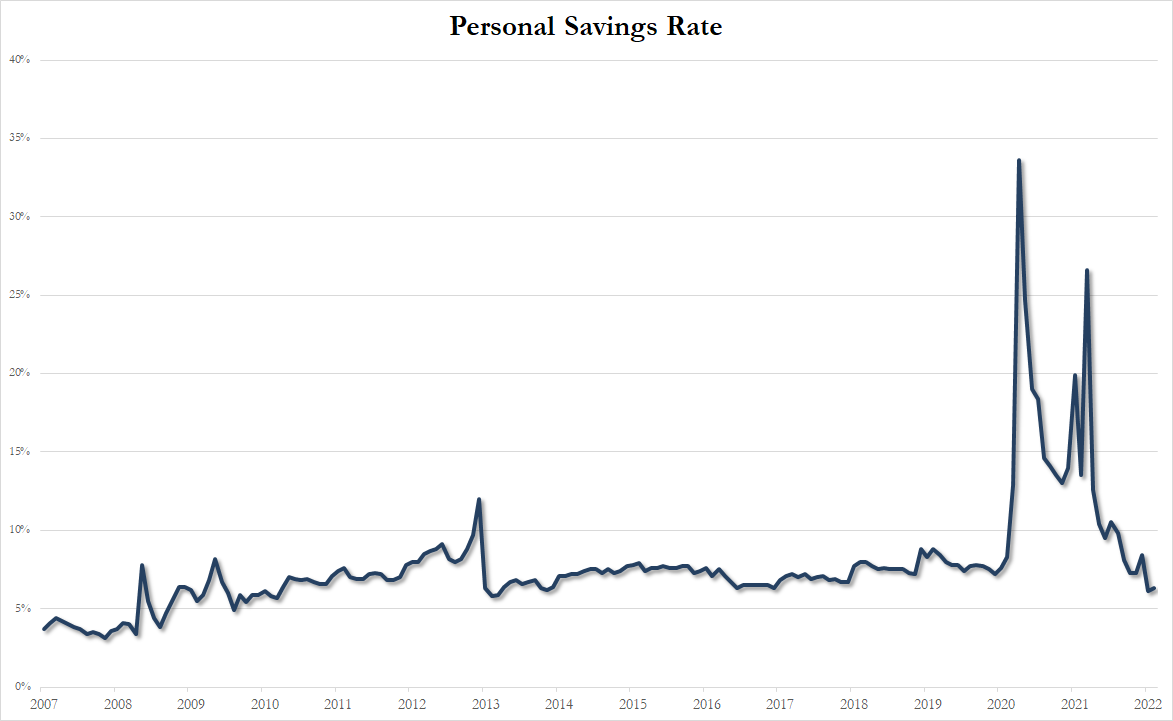

Shocking Consumer Credit Numbers: Credit Card Debt Soars With Savings Long Gone

BY TYLER DURDEN

THURSDAY, APR 07, 2022 – 03:21 PM

While it is traditionally viewed as a B-grade indicator, the February consumer credit report from the Federal Reserve was an absolute stunner and confirmed what we have been saying for month: any excess savings accumulated by the US middle class are long gone, and in their place Americans have unleashed a credit-card fueled spending spree.

Here are the shocking numbers: consumer credit exploded by a whopping $41.8 billion, more than double the expected $18.1 billion print, nearly five times more than the upward revised $8.9 billion January number (revised from $6.8 billion), and the highest on record!

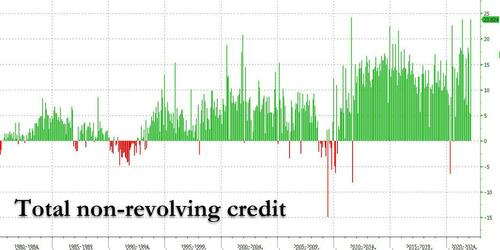

And while non-revolving credit (student and car loans) surged by a near record 23.8 billion, the third highest on record…

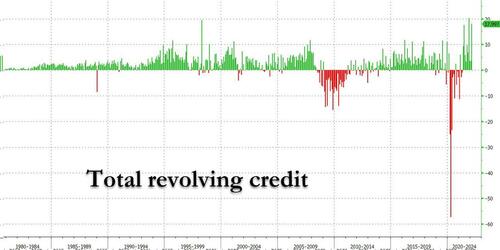

… the real stunner was revolving, or credit card debt, which soared nearly six-fold February to $18 billion from $3.1 billion in January, the second highest print on record, just in time for those credit card APR to starting moving higher, first slowly and then fast.

While this unprecedented rush to buy everything on credit at a time when there were no notable Hallmark holidays should not come as much of a surprise, after all we have repeatedly shown that for the middle class any “excess savings” are now gone, long gone…

… the fact is that most economists – such as those at Goldman Sachs – had previously anticipated that continued spending of savings by consumers (who they fail to realize are now tapped out) is what will keep the US economy levitating in 2022. Unfortunately, as today’s consumer credit numbers clearly demonstrate, any savings that US middle class households may have stored away courtesy of stimmies, are now gone. The implications are profound: any model that projected that US spending will be fueled by “savings” can now be trashed. And since this is most of them, the consequences are dire as they confirm – once again – that the Fed is tapering, QTing and hiking right into a recession, which according to Deutsche Bank will begin in late 2023 and which according to Morgan Stanley can start in as little as 5 months. Today’s data suggests that Morgan Stanley is right…

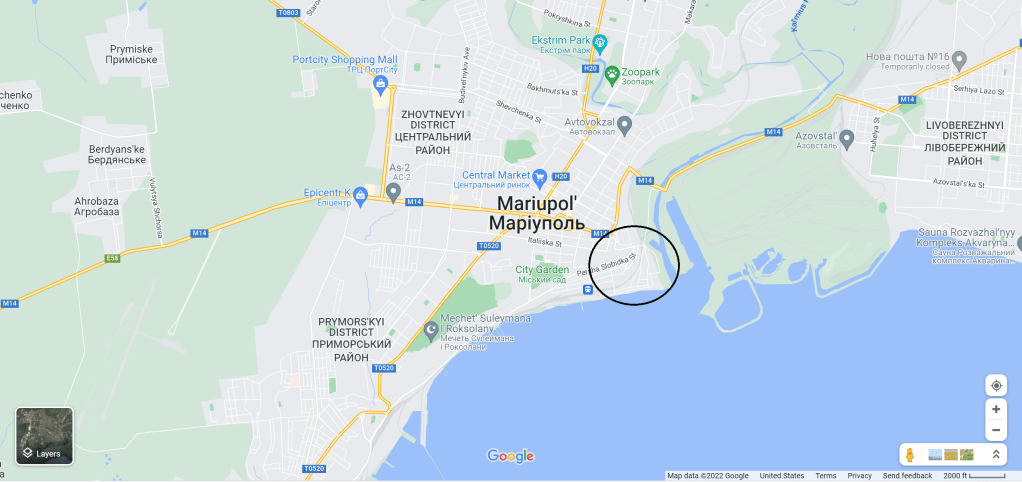

The city map below highlights the Steel Plant where the last of the “really out there” Azov Battalion (more like a division) and other units of the dwindling Ukrainian forces are using their American weapons to the last round duking it out with Chechen, Russian Marines, and LDPR units.

Before a few of today’s videos, first a bit about Mariupol.

The city is largely and traditionally Russian-speaking, while ethnically the population is divided about evenly between Ukrainians and Russians. There is also a significant ethnic Greek minority in the city.

In 2002, ethnic Ukrainians made up the largest percentage (48.7%) but less than half of the population; the second greatest ethnicity was Russian (44.4%). A June–July 2017 survey indicated that Ukrainians had grown to 59% of Mariupol’s population and the Russian share had dropped to 33%.[62]

The city is home to the largest population of Pontic Greeks in Ukraine (“Greeks of Priazovye”) at 21,900, with 31,400 more in the six nearby rural areas, totaling about 70% of the Pontic Greek population of the area and 60% for the country.

Following the 2022 Russian invasion of Ukraine, Mariupol stood as a strategic target for Russian and pro-Russian forces. From 25 February, the city has been under siege. On 13 March the Red Cross warned that the siege had become a humanitarian crisis.

A month into the conflict, Ukrainian authorities said that about 90% of buildings in Mariupol were damaged or destroyed.[ An aid worker from the Red Cross described the conditions there as “apocalyptic”, with concerns for the humanitarian situation caused by severe damage to infrastructure, access to sanitation, and food shortages.

By 18 March, Mariupol was completely encircled and fighting reached the city centre, hampering civilian evacuation efforts.

On 24 March, Russian forces entered central Mariupol as part of the second phase of the invasion.

That operation is coming to a close as isolated Ukrainian units run out of supplies.

Mass surrender of 264+ Ukrainian servicemen from the 501st Separate Marine Battalion, 36th Marine Brigade of the Armed Forces of Ukraine.

Russia to see record capital inflow this year – reports

Skyrocketing oil prices and falling imports are the main factors, experts say

Russia’s balance of payments surplus could hit a historic high this year, amounting to $200-$300 billion, business news outlet RBC reported on Monday. Economists polled by RBC have predicted record capital inflows into the country, despite the tightening Western sanctions. [Note: $300 billion is what the US and EU stole – err, “froze” after the Biden Sanctions. And, that freeze prompted Russia’s insistence for payment in rubles]

They pointed to major factors behind the inflow, such as the increase in the value of Russian energy exports, and a reduction in merchandise imports to Russia by up to 50%.

“The key driver of the Russian balance of payments surplus [hydrocarbon exports] still looks confident,” the Institute of International Finance (IIF) said in its review, seen by RBC.

According to a Bloomberg analysis, Russia will get an estimated $321 billion in energy exports revenue in 2022, marking a surge of more than a third compared to last year. That’s despite the huge discounts the country provides. The Russian Ministry of Finance said last week that, on average, Russian Urals oil cost over $89 per barrel in March, which is a 40% rise year-on-year.

The IIF said that the number of oil tankers moored in Russian ports awaiting departure is only slightly less than in the same period in previous years. Data by TankerTrackers, a company that tracks the movement of oil tankers around the world, showed that Russia still exports about three million barrels per day of oil by sea, and those deliveries are quite transparent.

President Biden banned U.S. imports of crude oil, refined petroleum products, natural gas, coal, and coal products that originate in Russia. The President’s executive order, however, does not restrict U.S. energy imports originating in other countries that transit through Russia or depart from Russia’s ports. Crude oil exported from countries including Kazakhstan, Azerbaijan, and Turkmenistan moves through Russia’s energy export infrastructure. Crude oil from Russia can be imported into the United States if it is marketed and loaded with a certificate of origin verifying that the crude oil is of non-Russian origin.

Crude oil exported from Kazakhstan moves primarily through the Caspian Pipeline Consortium (CPC) system. The CPC travels around the north side of the Caspian Sea and through Russia, transporting crude oil produced in Kazakhstan to the Russian Black Sea port of Novorossiysk. Some crude oil produced in Russia is transported in the same pipeline as CPC grade crude oil, but it represents around 10% of the crude oil exported through the CPC system.

Crude oil is also exported from Kazakhstan through Russia’s Transneft pipeline system to Novorossiysk and the Russian Baltic Sea port of Ust Luga, as well as through the Kazakhstan-China Pipeline to China. Most exports originating in Kazakhstan travel by pipelines through Russia or are shipped out of Russia’s ports.

Exports of crude oil from Azerbaijan are largely transported through the Turkish port of Ceyhan through the Baku-Tbilisi-Ceyhan (BTC) pipeline, which does not pass through Russia. However, small amounts of crude oil are exported from Azerbaijan through Russia. Significant volumes of crude oil are not exported from Turkmenistan, but it can travel west to Ceyhan through the BTC pipeline or travel north to Novorossiysk from the Russian Caspian port of Makhachkala through the Baku-Novorossiysk pipeline. In 2021, 25,000 barrels per day (b/d) was exported from Azerbaijan, and 43,000 b/d was exported from Turkmenistan through Russia, according to data from Argus Media.

In 2021, most exports of crude oil from Kazakhstan went to Europe, but some were received in the United States. Ports on the U.S. East Coast received 18,000 b/d of light, sour crude oil imports from Kazakhstan—an amount representing less than 0.3% of U.S. crude oil imports that year. Crude oil from Azerbaijan has not been imported into the United States since 2018, and crude oil from Turkmenistan has never been imported into the United States.

Russian Ruble relaunched linked to Gold and Commodities – RT.com Q and A

With Russia’s central bank having just profoundly altered the international trade and monetary system by linking the Russian ruble to both gold and commodities, the journalists at RT.com in Moscow asked me to write a Q and A article on what these developments mean, and the ramifications of these changes on the Russian ruble, the US dollar, the gold price and the global system of currencies. This article has been published on the RT.com website here.

Regular readers will recall that I have contributed to quite a few RT.com articles before, such as about Australian gold (see BullionStar here), US Treasury gold (see BullionStar here), Poland’s gold (see RT site here), China’s gold (see RT’s Spanish site here), why buy physical gold (see RT site here), and gold price manipulation (see RT site here).

However, since RT.com is now blocked and censored in many Western locations such as the EU, UK, US and Canada, and since many readers may not be able to access the RT.com website (unless using a VPN), my Questions and Answers that are in the new RT.com article are now published here in their entirety.

Who would have thought that citizens of ‘free speech’ Western countries would need a VPN to read a Russian news site?

Why is setting a Fixed Price for Gold in Rubles significant?

By offering to buy gold from Russian banks at a fixed price of 5000 rubles per gram, the Bank of Russia has both linked the ruble to gold and, since gold trades in US dollars, set a floor price for the ruble in terms of the US dollar.

We can see this linkage in action since Friday 25 March when the Bank of Russia made the fixed price announcement. The ruble was trading at around 100 to the US dollar at that time, but has since strengthened and is nearing 80 to the US dollar. Why? Because gold has been trading on international markets at about US$ 62 per gram which is equivalent to (5000 / 62) = about 80.5, and markets and arbitrage traders have now taken note, driving the RUB / USD exchange rate higher.

So the ruble now has a floor to the US dollars, in terms of gold. But gold also has a floor, so to speak, because 5000 rubles per gram is 155,500 rubles per troy ounce of gold, and with a RUB / USD floor of about 80, that’s a gold price of around $1940. And if the Western paper gold markets of LBMA / COMEX try to drive the US dollar gold price lower, they will have to try to weaken the ruble as well or else the paper manipulations will be out in the open.

Additionally, with the new gold to ruble linkage, if the ruble continues to strengthen (for example due to demand created by obligatory energy payments in rubles), this will also be reflected in a stronger gold price.

Gazprom – Natural gas powerhouse and Russia’s largest company

What does this mean for Oil?

Russia is the world’s largest natural gas exporter and the world’s third largest oil exporter. We are seeing right now that Putin is demanding that foreign buyers (importers of Russian gas) must pay for this natural gas using rubles. This immediately links the price of natural gas to rubles and (because of the fixed link to gold) to the gold price. So Russian natural gas is now linked via the ruble to gold.

The same can now be done with Russian oil. If Russia begins to demand payment for oil exports with rubles, there will be an immediate indirect peg to gold (via the fixed price ruble – gold connection). Then Russia could begin accepting gold directly in payment for its oil exports. In fact, this can be applied to any commodities, not just oil and natural gas.

What does this mean for the Price of Gold?

By playing both sides of the equation, i.e. linking the ruble to gold and then linking energy payments to the ruble, the Bank of Russia and the Kremlin are fundamentally altering the entire working assumptions of the global trade system while accelerating change in the global monetary system. This wall of buyers in search of physical gold to pay for real commodities could certainly torpedo and blow up the paper gold markets of the LBMA and COMEX.

The fixed peg between the ruble and gold puts a floor on the RUB / USD rate but also a quasi-floor on the US dollar gold price. But beyond this, the linking of gold to energy payments is the main event. While increased demand for rubles should continue to strengthen the RUB / USD rate and show up as a higher gold price, due to the fixed ruble – gold linkage, if Russia begins to accept gold directly as a payment for oil, then this would be a new paradigm shift for the gold price as it would link the oil price directly to the gold price.

For example, Russia could start by specifying that it will now accept 1 gram of gold per barrel of oil. It doesn’t have to be 1 gram but would have to be a discounted offer to the current crude benchmark price so as to promote take up, e.g. 1.2 grams per barrel. Buyers would then scramble to buy physical gold to pay for Russian oil exports, which in turn would create huge strains in the paper gold markets of London and New York where the entire ‘gold price’ discovery is based on synthetic and fractionally-backed cash-settled unallocated ‘gold’ and gold price ‘derivatives.

Russian gold bars stored in wooden boxes in the Gokhran vaults, Moscow

What does this mean for the Ruble?

Linking the ruble to gold via the Bank of Russia’s fixed price has now put a floor under the RUB/ USD rate, and thereby stabilized and strengthened the ruble. Demanding that natural gas exports are paid for in rubles (and possibly oil and other commodities down the line) will again act as stabilization and support. If a majority of the international trading system begins accepting these rubles for commodity payments arrangements, this could propel the Russian ruble to becoming a major global currency. At the same time, any move by Russia to accept direct gold for oil payments will cause more international gold to flow into Russian reserves, which would also strengthen the balance sheet of the Bank of Russia and in turn strengthen the ruble.

Talk of a formal gold standard for the ruble might be premature, but a gold-backed ruble must be something the Bank of Russia has considered.

What does this mean for Other Currencies?

The global monetary landscape is changing rapidly and central banks around the world are obviously taking note. Western sanctions such as the freezing of the majority of Russia’s foreign exchange reserves while trying to sanction Russian gold have now made it obvious that property rights on FX reserves held abroad may not be respected, and likewise, that foreign central bank gold held in vault locations such as at the Bank of England and the New York Fed, is not beyond confiscation.

Other non-Western governments and central banks will therefore be taking a keen interest in Russia linking the ruble to gold and linking commodity export payments to the ruble. In other words, if Russia begins to accept payment for oil in gold, then other countries may feel the need to follow suit.

Look at who, apart from the US, are the world’s largest oil and natural gas producers – Iran, China, Saudi Arabia, UAE, Qatar. Obviously, all of the BRICS countries and Eurasian countries are also following all of this very closely. If the demise of the US dollar is nearing, all of these countries will want their currencies to be beneficiaries of a new multi-lateral monetary order.

“It was once said that ‘gold and oil can never flow in the same direction’.” ANOTHER 1997

What does this mean for the US Dollar?

Since 1971, the global reserve status of the US dollar has been underpinned by oil, and the petrodollar era has only been possible due to both the world’s continued use of US dollars to trade oil and the USA’s ability to prevent any competitor to the US dollar.

But what we are seeing right now looks like the beginning of the end of that 50-year system and the birth of a new gold and commodity backed multi-lateral monetary system. The freezing of Russia’s foreign exchange reserves has been the trigger. The giant commodity strong countries of the world such as China and the oil exporting nations may now feel that now is the time to move to a new more equitable monetary system. It’s not a surprise, they have been discussing it for years.

While it’s still too early to say how the US dollar will be affected, it will come out of this period weaker and less influential than before.

What are the Consequences of these Developments?

The Bank of Russia’s move to link the ruble to gold and link commodity payments to the ruble is a paradigm shift that the western media has not really yet been grasped. As the dominos fall, these events could reverberate in different ways. Increased demand for physical gold. Blowups in the paper gold markets. A revalued gold price. A shift away from the US dollar. Increased bilateral trade in commodities among non-Western counties in currencies other than the US dollar.

{kind=link}

{kind=link}

{kind=link}

{kind=link}