Gold, Goats, and Guns: https://tomluongo.me/2021/10/06/european-energy-crisis-gas-you-think-burning/

The European Gas Crisis keeps hitting new high after new high as gas prices around the world go ballistic. While this isn’t just a European problem, if you read the MSM, that’s all they seem to care about.

You know, it snows in Japan as well folks, and China.

Prices keep skyrocketing in Europe because there is no shortage of idiocy at the top of the European power structure. The confluence of the pressurizing of Nordstream 2 with the release of the “Pandora Papers” and the beginnings of German coalition talks just after the beginning of Q4 should have everyone’s Spidey-Sense shutting down like your adrenals do after a long period of self-inflicted stress.

And honestly, whose adrenals aren’t on the verge of collapse after eighteen months of ‘flatten the curve,’ ‘follow the science,’ and ‘just roll over to the Communism, already, you disgusting plebe!’ that we’ve been going through.

I guess that’s yet another thing we have to try and factor into our analysis of what collapse is the most imminent?

Because when you put this gas crisis in Europe into its proper context it should be clear where the battle lines are being drawn as the extreme pressure cooker of today’s geopolitical landscape forces everyone off the sidelines and into the fray.

On the one hand we have natural gas prices in Europe approaching coffin corner. On the other we have Russia browning out gas deliveries to Europe. China is experiencing major energy shortages and the entirety of the coal delivery network around the world is buckling.

These are facts. There are more I could list but let’s stay focused here.

The thing that makes no sense, seemingly, is that no one has an answer why these facts exist in the first place.

Because all anyone official ever wants to do is blame the sneaky Russians to avoid their own responsibility for this.

Finally, after a couple of weeks of this howling, Russian President Vladimir Putin addressed the issue from their side.

I suggest strongly you read his remarks carefully. Because in there you’ll find a couple of ‘facts’ which make this entire crisis in Europe seem like yet another staged ‘false flag’ for political gain. Ready?

The two middle points are the ones the no one want to report on but are the key to the understanding of this.

Europe is engaged in a game of idiotic brinksmanship with its people and the capital markets over gas supplies. They do this to construct a narrative and distort markets for political benefit.

When the reality is that this entire ‘crisis’ is a manufactured one because of their unwillingness to bow to the forces their policies have unleashed.

Gas prices in Europe are this way because of Europe’s own mistakes in trying to remake its economy (Putin Point #4).

Moreover, Putin also urged Gazprom, as a gesture of good faith despite his misgivings, to ship gas through Ukraine even though it would be better to turn on other capacity.

“Gazprom believes that it is economically more viable, it would even be more profitable to pay a fine to Ukraine, but to increase the volume of pumping through new systems precisely because of the circumstances that I mentioned – there is more pressure in the pipe, less CO2 emissions into the atmosphere. Everything is cheaper, around 3 billion a year. But I ask you not to do this,” the President said.

Does this sound like the mustache-twirling tyrant that’s portrayed in the odious British, US and German media?

Of course not. Now, I’m not accusing Putin of being an angel here or anything, he’s throwing scraps back to people who have put themselves in a position to starve and freeze to death, both literally and politically.

The goal here is to highlight just how moronic the EU’s stance on energy has become, to finally to break up the logjam.

He’s happy to see Gazprom (and possibly Rosneft if need be) sell all Europeans as much gas as it can supply and they demand, but only on terms that benefit everyone, supplier and demander. As I’ve talked about in previous blog posts, the EU thinks they have a monopsony on Russian gas and because of this can dictate terms to them.

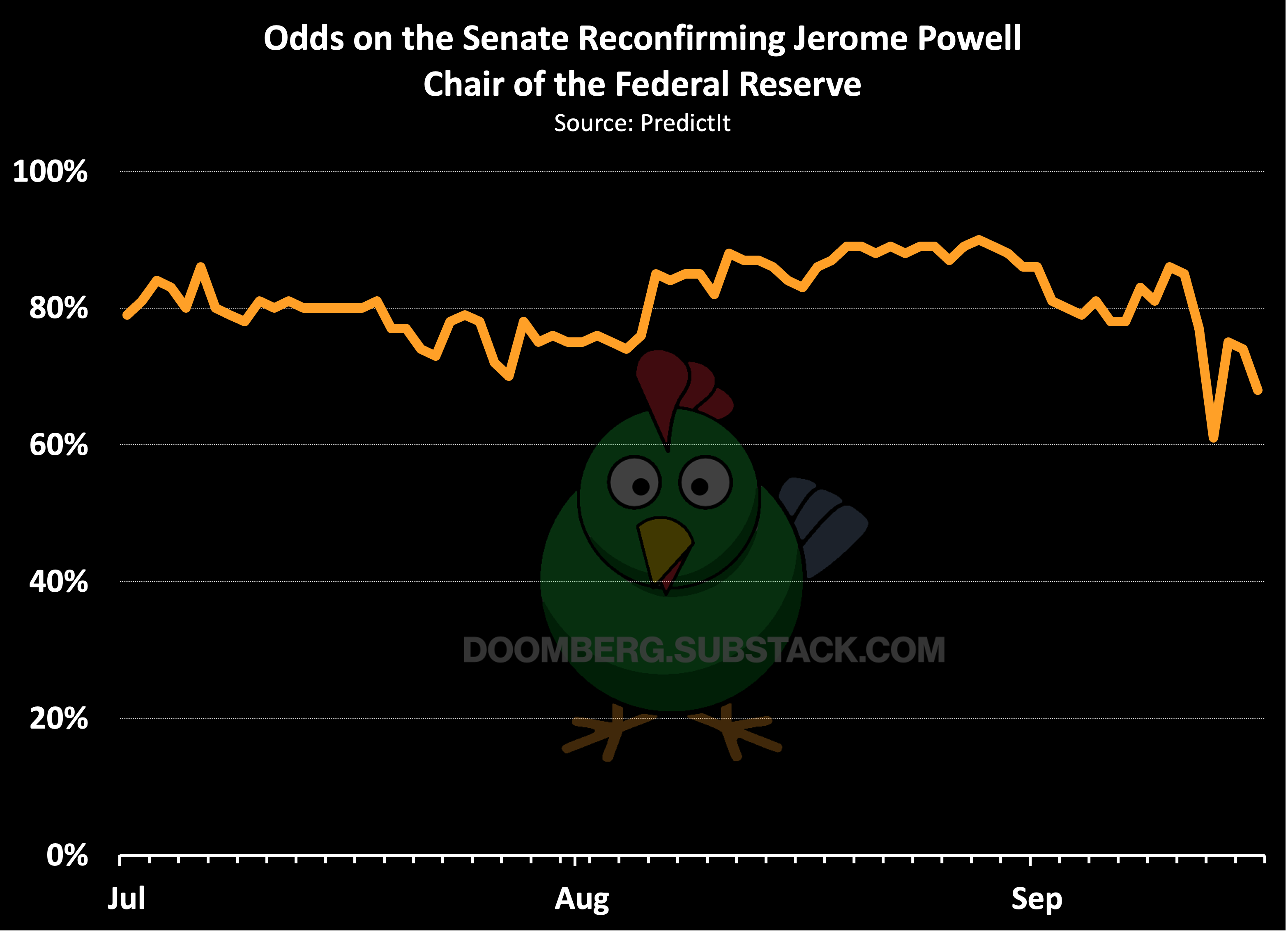

This is patently untrue, and Gazprom shifting around supplies for a few days here and there proves that point dramatically. Like Jay Powell draining the world of eurodollars with just five basis points, Putin and Gazprom can expose the the extent of Eurocrat mendacity with just a few days of slowing gas exports.

That’s why this brinksmanship over gas supplies and electricity prices isn’t aimed at the Russians, who clearly have other customers for their gas, but with the people of Europe themselves and the capital markets structured around one-sigma price volatility. They are now extremely vulnerable even if things begin to return to normal.

The Russian Bogey Man is simply the cover story for what is a much deeper and, frankly, much more disturbing game.

So, while Zerohedge is correct about gas supply brown outs in Europe it’s only partly for reasons abundantly clear to even first-year geopolitical analysts:

Flows dropped as Gazprom has booked only about a third of the gas transit capacity it was offered for October via the Yamal-Europe pipeline and no extra transit capacity via Ukraine.

Gazprom declined to comment. It has repeatedly said it was supplying customers with gas in full compliance with existing contracts and said additional supplies could be provided once the newly built Nord Stream 2 gas pipeline was launched.

Ball. Court. Germany.

Yes, Germany needs Nordstream 2. Hell, Europe needs Nordstream 3 if these Davos ninnies are wrong about Climate Change, which they are.

Germany is the country caught in the middle of this titanic battle for the future of the world and Davos is the group creating this false flag to force a shift in sentiment negatively towards Russia.

That’s what’s driving this current crisis, one that, I think, is now threatening the future of the European Union itself. If those are the stakes, then eventually someone will finally do the right thing. Putin just offered the smallest of olive branches. Now let’s see if the European Commission has three collective brain cells to rub together and figure out how to save face (and their backsides).

Beating up and demeaning your neighbor is not a winning strategy, nor is it a path to lower prices and stable markets. At some point they, in this case the Russians, realize the situation is exactly what it looks like from the outside, war. And, Putin is finally treating the EU commissars as enemy combatants because that’s who they are.

That’s why his comments were structured to put the onus of the crisis back on Europe’s leadership rather than blaming the people keeping the lights on.

Whenever things like this happen Capitalism is always blamed. But, it’s always Commie vandals like the EU Commission who created the problem, either deliberately with dumb things like the Third Gas Directive or malinvestment of capital which leaves the world vulnerable to a hot summer in Asia.

And this is the essential point no one wants to confront. The EU picked this fight purely for political purposes because they have an agenda — energy instability for political benefit — but it has come back to bite them in the ass.

Because, as I said, the markets are so tight it takes only a small shift in sentiment to see the prices of things with inelastic demand, like energy, rise dramatically with a marginal shift in either supply, demand or, in this case, both.

Russia doesn’t act this ‘by the book’ at this moment in time without a plan. Treating the EU like the enemies they are is the strategic play. Whining about it in the media only accentuates their weakness and lack of leverage.

My friends at Mittdolcino.com are positively despondent because they see this power play for how it affects Italy, which is that it will carve the country up into pieces over divergent needs for inflation and deflation between it and Germany since one of these two countries need to exit the Euro-zone.

There’s no way this massive ‘drop’ in Russian supplies to the EU occurs without a longer-term strategic plan by the Russians. Putin has made it clear he is fully fed up with EU shenanigans and this is the time for him to put the most pressure imaginable on Brussels to break the EU into tiny pieces.

How? It’s again, all about Germany.

When Nordstream 2 was announced and I was writing Gold Stock Advisor for Newsmax in 2013 I talked then about how the difference between how gold was accounted for between the ECB and the Fed. That put Germany squarely in the middle between the U.S. on one side and Russia on the other.

Russia and China still hadn’t signed the big deal for the Power of Siberia pipeline at the time. They are now working on Power of Siberia 2, which will open up the massive mineral deposits in Mongolia. So, even then, in my naïve way of seeing the world as a first-year geopolitical analyst, I understood that Russia’s foreign policy had to be focused on getting Germany to side with them versus the U.S.

The political establishment in Germany was never going to let that happen because under Obama Davos was running the operation to cleave Ukraine from Russia. To date, both have been partially successful. Both Ukraine and Germany are being torn apart from within as domestic leadership bows to internationals forces forcing them to pursue policies which go completely against their countries’ wishes and best interests.

So, now, fast forward to today. The day after the German elections brings a mess but with a highly likely outcome that the SPD will ally with the Greens and the FDP. With Christian Lidner (FDP) as Finance Minister (at least temporarily) we would have a German government at war with itself.

As Alex Mercouris brought up after I left the chat with Crypto Rich last week, the Greens are fracturing over the Russia issue. Part of them wants a restoration of good Russian relations, the other are neocon/Davos infiltrators trying to constantly move the goalposts on both Climate Change and geopolitics.

The SPD are pure Davos scum so expect nothing good from them. This is why I think Putin ‘shut off the taps’ the day after the election. Like everyone else, he can see what Davos is doing and doesn’t like it. So, in order for him to make his point he does exactly what he should: stop trading with those who have unofficially declared war on Russia and push the political scene in Germany to a breaking point.

Because here’s where this goes. Germany needs to either control the purse strings of the EU or it needs to leave the euro-zone and be independent of the sinking ship. Putin realizes that the best way to achieve this is to pour gasoline on a raging firestorm in the energy markets (oh, the humanity of the puns!) and remind German voters just who is truly responsible for their €2000/month electricity bills.

It’s not Putin. It’s Berlin. So, Berlin needs to sign off on Nordstream 2 and then ram it down the EU Commission’s throat. And they better do it soon because Winter is Coming, after all.

And they just voted for more of this while Merkel, who has been the biggest obstacle to AfD’s inclusion in any government, is leaving the scene. The CDU leadership got whacked across the board. Most of the big names will not be in the Bundestag this time around, so the party will be doing a lot of self-reflection and could finally become relevant again.

Inflation of the type Putin is ‘forcing’ on Europeans today is the type a country only recovers from with a political inversion. This is why today we’re seeing surprise rate hikes from Poland, for example. It’s why Serbia is begging Russia to increase gas supplies there and Hungary signed a 15-year deal to secure its energy future.

While there is no appetite for a political inversion in Germany today after last week’s vote, there will be in about 3 months if coalition talks stall. Because the ECB under Christine Lagarde cannot raise rates but is powerless to stop them rising ultimately if the market senses that there is no political leadership capable of reining it in.

That ship sailed a few months ago after the Fed called Lagarde’s hawkish bluff and actively drained more than $1 trillion from overseas dollar markets and just increased the capacity to drain even more, without tapering QE.

Now let’s go back to the Fed and Wall St. If there is a real backlash within some areas of the U.S. ‘big money’ against Davos which is showing up as Fed monetary policy, per my consistent analysis of the situation and events playing out to support it, then they are tacitly coordinating with Putin to give Germany what it wants, an excuse to leave the euro and conduct independent trade and energy policy.

Think about it. On the one hand the Fed is drying up dollars. On the other Putin is spiking energy prices making it impossible for Germany to fight inflation within the EU. On the third hand, China is cracking down on property speculation domestically, kicking out the foreign NGOs and reminding foreign investors that the rules in China are not the same as they are in the West.

You can and will lose all your money if you invest behind the Great Wall, as so many Evergrande bondholders just found out.

Now let’s square the entire circle. If Europe’s energy crisis is a constructed false flag event to spook capital, encourage speculators and effect political change, then can’t you make the same arguments for the concurrent fight on Capitol Hill regarding the Democrats, the debt ceiling and the spending bills?

Senate Majority Leader Mitch McConnell has been adamant that the Democrats do not need any help in passing a debt ceiling resolution. They can do it any time they want to. But, the Democrats won’t do this? Why? They are manufacturing a narrative that there is crisis on the horizon — default on U.S. bond payments.

This is the one outcome no investor wants to contemplate. So, the Democrats, like the Europeans, are arguing against themselves in order to blackmail the world into giving them their cookie or they will hold their breath until they collapse global markets.

Let me repeat. There is no debt ceiling crisis. There is no U.S. default crisis. There is only a bunch of Mafiosi on Capitol Hill doing what they’ve been told to do while purposefully scaring everyone into believing there is a crisis when none exists.

Do I have to invoke a classic Who song to make my point?https://www.youtube.com/embed/BfrUQA2tb6M?version=3&rel=1&showsearch=0&showinfo=1&iv_load_policy=1&fs=1&hl=en-US&autohide=2&wmode=transparent

What’s the goal? Chaos and the continued undermining of faith in politics, capital markets, energy production and seizing supply chains as we approach the winter in the Northern Hemisphere where susceptibility to pesky things like the flu, the latest iteration of COVID-9/11 and blatant political bullshit swells like a boil on the back of a government bureaucrat blocking a permit for some basic, but eminently important thing.

That Putin came out and told the world he’s ready to work with Europe to do his part alleviating the energy supply problems in Europe I’ve not heard one encouraging word from those that would benefit from this the most.

Their silence is deafening.

And that brings me back to Germany where, unless this gets resolved quickly, the most likely downstream outcome is Germany leaving the euro, reinstitute the Deutsche Mark, watch it fall vs. the dollar in the near term but outcompete the euro.

With the euro in freefall after a disastrous Q3 close and German Bunds getting prepared for their next big sell-off, perhaps, maybe, for the first time in a long time, the markets are beginning to wake up from their central bank induced SOMA injections and get real with the possibilities that forces are now aligned to do the unthinkable, break up the EU.

But that only happens with a political inversion where the CDU/CSU ally with AfD and the FDP to form a real government after the current parties can’t form a coalition or any three-way coalition formed fails as inflation crushes the German middle class.

If the AfD were smart now they would be blaming all of this on Merkel’s moronic energy policy. Now we’re seeing calls for delaying shutting down Germany’s nuclear reactors. They can’t import enough coal to feed the plants. BASF has shut down ammonia production, so food production is threatened.

There is no Agenda 2030 on the horizon if Germans freeze to death in their homes or get decimated by COVID-9/11 because they can’t afford to heat their homes.

This will crush France and Macron, overthrow Davos at the mid-terms here in the states and break the European Union in the process.

Germany is the lynchpin to the entire Davos edifice. Without a compliant and beaten Germany there is no further Great Reset. A Germany that breaks from the euro becomes a Germany that realigns with Russia and Eastern Europe. It’s a Germany no longer hell bent on internal European mercantilism and the establishment of the Fourth Reich through the EUSSR.

The German people keep asking for that policy to end but aren’t given the options by their leadership to make that happen. Then again, they keep giving their leadership just enough power to forestall their having to make a real decision. That decision is coming at them, fast.

As it is everyone across the West in various guises.

So, as as Powell under extreme pressure to go full MMT retard with five little basis points, Putin, with a few million BTUs of gas, is forcing open fault lines in the aristocracy that thinks it deserves to run the world. Together, if they simply sit back and continue to do nothing, can bring down the whole rotten edifice.