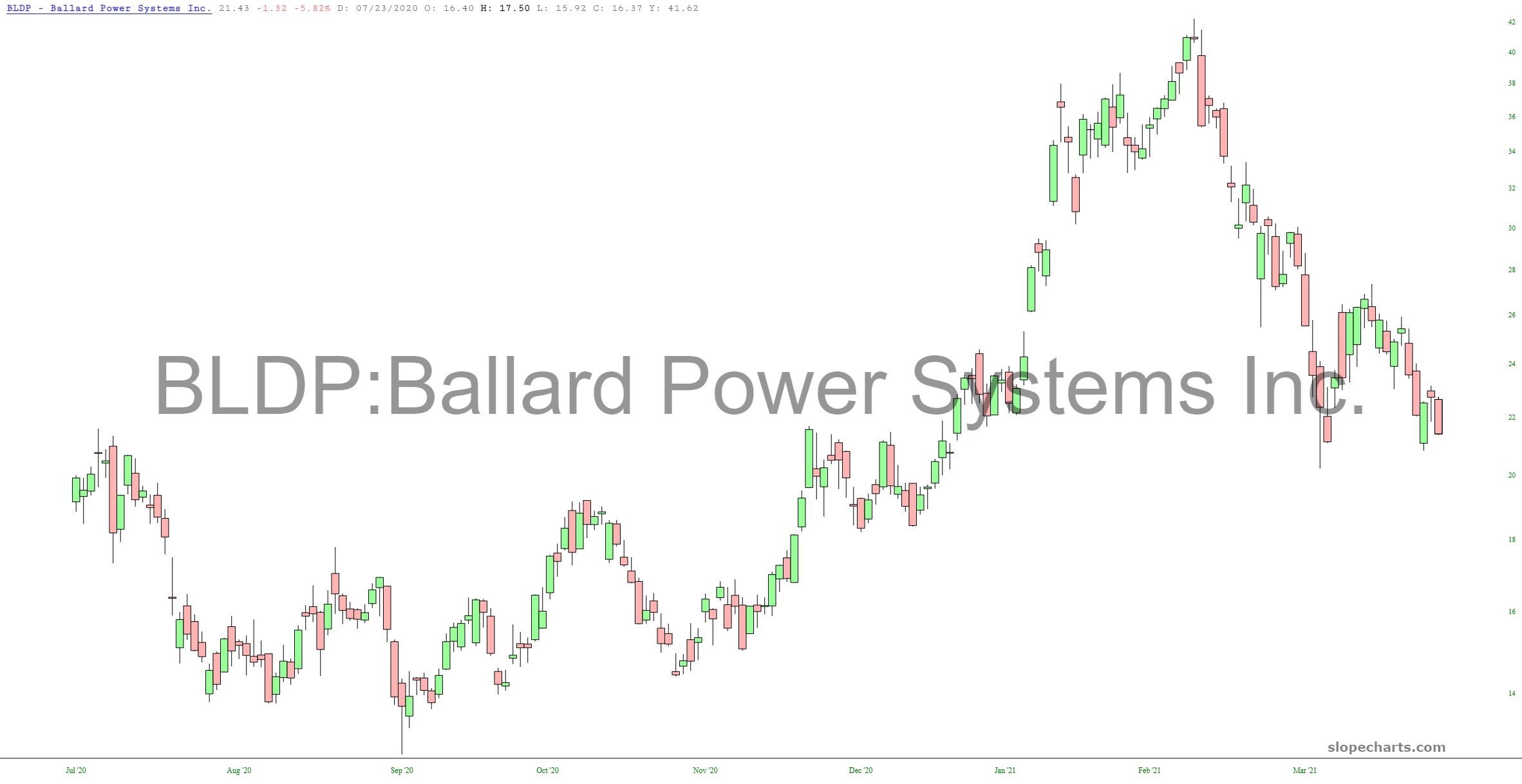

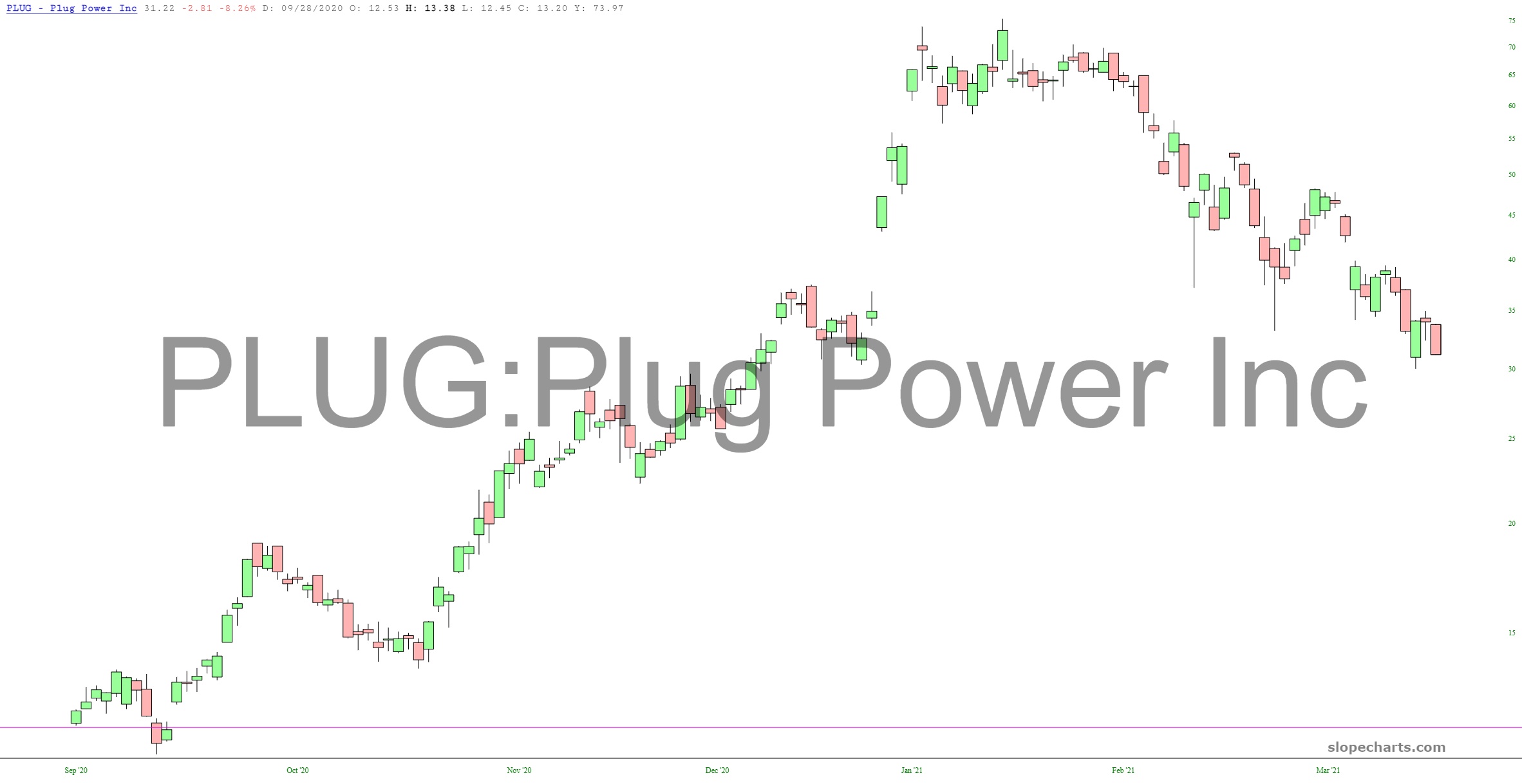

Not long ago, all you needed to to as a company to guarantee success as a financial entity was to somehow associate yourself with electric cars. That’s over. Just take a look at the corrosive erosion taking place across the entire sector. My view is that this collapse has only just started, and I’m not even including the outright frauds you already know and shan’t be repeated here.

Cooper (2021) at least seven genetically independent lineages acquired a mutation at one particular spot on the virus’s infamous spike protein. Spike has a sequence of linked amino acids, and the mutation occurs at position number 677. In the original SARS-CoV-2 this is the amino acid glutamine, abbreviated as Q.

Mutations in at least eight different positions in the spike protein are simultaneously on the rise around the world, appearing in B.1.1.7 and in other major variants of concern known as B.1.351, P.1 and P.3. These variants share combinations of mutations at positions 18, 69–70, 417, 452, 501, 681 and a particularly concerning E484K mutation that evades neutralizing antibodies.

Cooper speculates that the virus is beginning to run out of new, major adaptations.

The former director of the Centers for Disease Control and Prevention believes the virus that causes COVID-19 escaped from a lab in Wuhan, China, according to a new interview.

Robert Redfield told CNN on Friday that it was his “opinion” that SARS-CoV-2 — the new coronavirus responsible for killing 2.7 million people globally — did not evolve naturally.

“I’m of the point of view that I still think the most likely etiology of this pathology in Wuhan was from a laboratory — escaped,” said Redfield, who led the CDC during the height of the pandemic. “Other people don’t believe that. That’s fine. Science will eventually figure it out.”

Researchers believe the deadly and highly transmissible strain of coronavirus behind the global pandemic mutated from a virus that infects animals — namely, bats — to one that sickens humans.

But some believe the virus was somehow released from the Wuhan Institute of Virology — which is the only lab in China authorized to study the most dangerous known pathogens, according to Axios.

“It’s not unusual for respiratory pathogens that are being worked on in a laboratory to infect the laboratory worker. … That’s not implying any intentionality,” Redfield said. “It’s my opinion, right? But I am a virologist. I have spent my life in virology.

“I do not believe this somehow came from a bat to a human and at that moment in time, that the virus came to the human, became one of the most infectious viruses that we know in humanity for human-to-human transmission.”

Redfield said usually when a virus jumps from animals to humans, “it takes a while for it to figure out how to become more and more efficient in human-to-human transmission.” (Emphasis added)

Thinking back to a long time ago, I recall dealing with some rather unsavory people for a time. They were cashing government paychecks, of course, which made the “unsavory” part predictable. Then again, so was I at that time.

Anyway, they were a lot of fun off-duty – most sociopaths are. As long as you regularly remind yourself who you are drinking with, you can have fun AND still maintain some situational awareness.

Besides, I “wasn’t the droid they were looking for.”

I kind of think that’s why the FBI had more of a challenge smearing Carter Page in the “Get Trump Anyway You Can” campaign – Page was a player and he had situational awareness when approached. Page just assumed the DOJ would never set him up.

Silly rabbit.

Seems today, most of the country is really into the sociopath thing – Clinton, Obama, celebrity worship. I continue to be surprised when seemingly intelligent people tell me how wonderful the Obamas are.

We interrupt today’s Caitlin Johnstone article with this breaking news report from the National News Conglomerate. NNC: Obey.

WASHINGTON — One of the nations the United States government has targeted for destruction is guilty of doing a very bad thing that nobody can see, according to sources familiar with the matter.

One senior official who spoke on conditions of anonymity told NNC that while nobody was killed or injured by the bad thing that was done by the bad country, and that the bad thing has in fact had no discernible effect on anything anywhere that everyday Americans would be able to perceive with the naked eye, it was still a very bad thing and will almost certainly require a much more inflated military budget to deal with.

“It’s true that the thing which was done was not bad enough to have hurt any American or to have affected the observable universe in any way that Americans can verify by observation, but it was definitely bad enough to justify strengthening our military presence against the bad country,” the official said. “I hear the Raytheon family has a fine line of surprisingly affordable new products to choose from that would be ideal for our nation’s national security needs.”

Other sources confirmed that the US intelligence community is between “somewhat confident” and “kinda confident” in its assessment that the thing we just reported as verified fact in preceding paragraphs actually occurred.

When another source familiar with the matter was asked if the US government would be providing the public with any evidence that the bad thing had in fact happened and had actually been done by the accused foreign government, the source said “Ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha.”

“Ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha,” the source then added. “Oh wait you’re serious, let me laugh even harder, ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha.”

“The evidence is classified,” the source added, anonymously. “It’s secret, invisible evidence.”

Les Overton, a senior fellow at the DC-based policy group American Freedom Democracy for Freedom Institute, told NNC that it is common for US government agencies to make unverifiable claims about invisible misdeeds being perpetrated by nations the US government doesn’t like.

“Sometimes it’s hacking, sometimes it’s paying bounties on US soldiers in Afghanistan, sometimes it’s election interference, sometimes it’s considering doing a bad thing and then not actually doing it,” Overton said. “Either way we always uncritically report the allegation as a fact unless it’s irrefutably proven false, and even then we just sort of still act like it’s true because we don’t want to be unpatriotic.”

“I mean, if you can’t trust an assertion by an anonymous official from the United States government, what in this world can you trust?” Overton added.

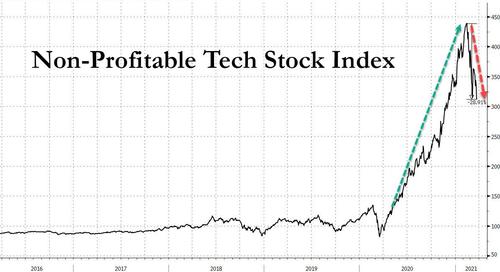

At the start of February, when the dual short squeezes of option gamma and WallStreetBets meme stocks were all the rage, a chart from Goldman indexing non-profitable tech companies was making the rounds across Wall Street desk; it showed the sector’s tremendous ascent since the Fed’s panicked response to the covid crisis, which more than quadrupled the return of this index.

Well, in the past month, things have gotten uglier, and at one point this morning, the index had plunged more than 30% from its February peak (now down 28.8%) after tumbling a whopping 7% yesterday.

Commenting on this furious reversal and the chart above, this morning Rabobank’s Michael Every – who evoked Jaws in his daily post for several other reasons – said “do you know what the graph of that particular market segment is starting to look like to me? A shark’s fin: and if that is indeed the case, we would soon see happy young traders suddenly pulled underwater and tossed around like rag dolls.”

Of course, this won’t be the first time “happy young traders are pulled underwater”, nor the first time that unprofitable companies explode higher only to crash immediately after. While many current traders won’t remember, and many may not even have been alive, an almost identical pattern presented itself in the run up to the bursting of the dot com bubble.

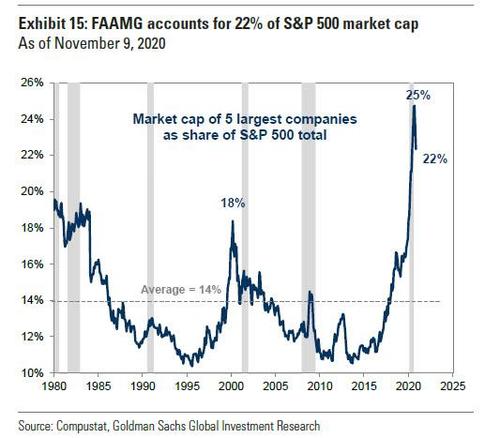

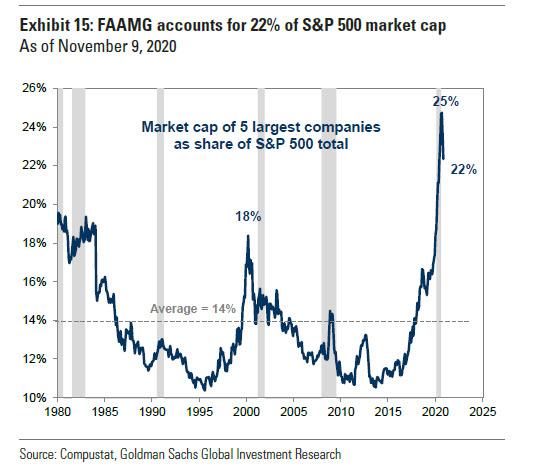

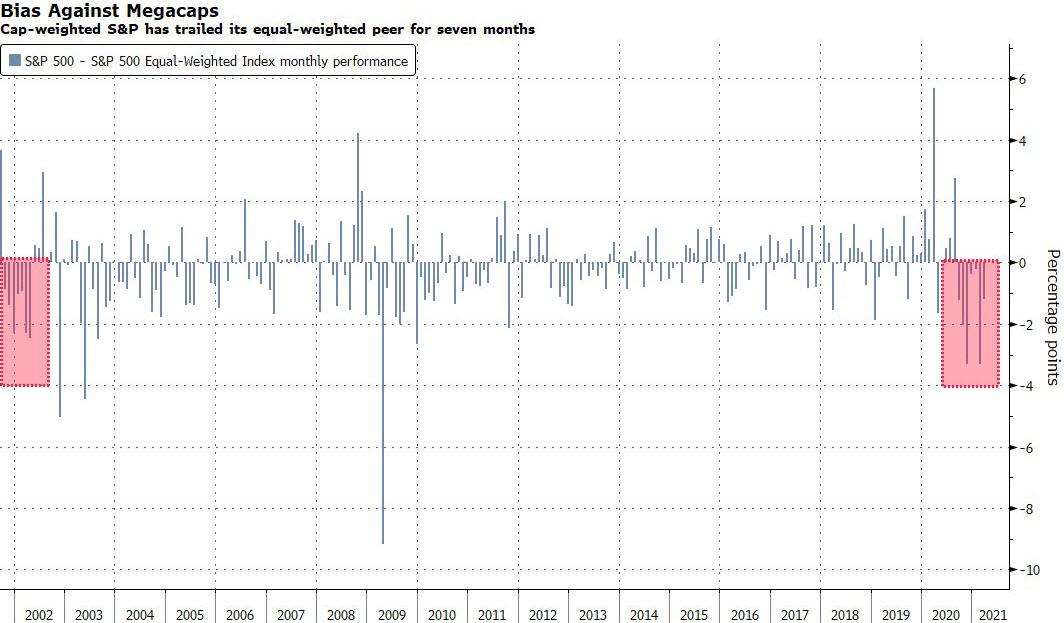

There are other reasons why the current market is “evoking memories of the dot-com crash” as Bloomberg notes this morning. One among them is the growing revulsion to the sector that in many ways defined 2020 – the FAANG names, which at one point last year account for a quarter of all market cap.

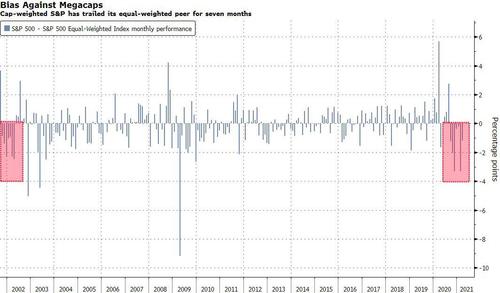

As Bloomberg’s Elena Popina writes in the daily Taking Stock colimn, “when the hegemony of the FAANG stocks cracked in September, it was a welcome reprieve for investors who watched a handful of names rule the market all year. Now it’s March, and the streak of under-performance by stocks with megacap bias is becoming historic.”

She refers to an equal-weight version of the S&P 500, which has outperformed its cap-weighted peer for seven months. That’s notable because it has now topped the streak after the financial crisis to become the longest stretch since the dot-com bust, indicating the buildup of a huge anti-megacap bias within the market. Said otherwise, a gauge of mega-cap stocks from Alphabet to Facebook and Netflix has trailed the S&P 500 Index for five out of seven months, as the value reversal kicked in and growth stocks have been left in the dust.

“Mega-cap tech, which dominates the market-cap-weighted index, is not looking as rosy in a post-pandemic world as we shift our consumption from screens to services,” said Max Gokhman, head of asset allocation at Pacific Life Fund Advisors.

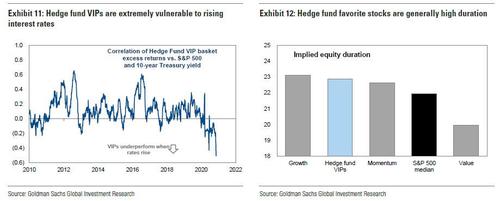

While it’s true that things have changed dramatically for tech stocks since the popping of the Internet bubble some 20 years ago, one thing stays the same: the group’s sensitivity to rising rates which has gotten even bigger. We have repeatedly shown this with a chart demonstrating the “duration” of the growth sector, and just how exposed the hedge fund community is to risk from higher interest rates (i.e. duration).

So going back to the bursting of the dot com bubble, Bloomberg reminds us that in the seven months from late 2001 through April 2002, the under-performance of the cap-weighted S&P 500 Index coincided with rising 10-year yields, which traded north of the 5% mark in the spring of 2002. A similar pattern happened in late 2009-early 2010, when a cap-weighted S&P 500 Index trailed its equal-weighted peer as yields went up.

“The difference this time around is that rates are likely to continue to climb over the long term,” said Matt Maley, chief strategist at Miller Tabak + Co. “In 2002 & 2009, they rolled back over after a couple of months.”

Actually no, Matt, the difference this time is that unlike 2002 and 2009, the Fed is now openly protecting stocks and defending even the dumbest equity investors, which is why Powell’s job (and that of his replacement in 2022) will be fascinating: how does the Fed achieve its two true mandates of runaway inflation (remember: no rate hikes until 2024) while avoiding a full blown crash in the tech sector.

I wasn’t being a wise guy. I was alone with him in his office, that’s how it came about,” Biden continued. “It was when President Bush had said, ‘I’ve looked in his eyes and saw his soul.’ I said, ‘I looked in your eyes, and I don’t think you have a soul.’ He looked back and he said, ‘We understand each other.’ ” — ABC News, Joe Biden with George Stephanopoulos on V. Putin of Russia

Somehow, I don’t think Joe Biden understood what he thought Vladimir Putin understood about what they mutually understood. If I had to guess, I’d say that Mr. Putin understood Joe Biden to be the most pathetic blustering schlemiel he’d ever encountered on the international scene. But that must have been before Mr. B was installed in the White House by powers and persons unseen because it’s evident now that his handlers do not allow him to talk to foreign leaders, not even on the phone. Ms. Harris does that.

The alleged president went on to tell Mr. Stephanopoulos that Mr. Putin was “a killer” who would “soon pay a price” for interfering in the 2020 election. In turn, Mr. Putin promptly called the Russian ambassador back home “for consultations,” which is generally what happens when one country makes warlike noises to another country.

Mr. Putin added a tantalizing taunt days later, saying. “I’ve just thought of this now. I want to propose to President Biden to continue our discussion, but on the condition that we do it basically live, as it’s called. Without any delays and directly in an open, direct discussion. It seems to me that would be interesting for the people of Russia and for the people of the United States. I don’t want to put this off for long. I want to go to the taiga this weekend to relax a little,” Mr. Putin went on. “So, we could do it tomorrow or Monday. We are ready at any time convenient for the American side.”

Do you suppose Vladimir Putin is having some sport with Mr. Biden, this lightweight even among US politicians, with brain-rot to boot? Pretty soon, the president’s handlers will have to forbid him to open his pie-hole in public altogether. No more one-on-one interviews even with slow-pitch party shills like Mr. Stephanopoulos. They’ll just wheel him into the rose garden periodically like a cigar store Indian for proof-of-life demonstrations and leave the management of the nation… to others.

And how’s that going after a couple of months? Apparently, economic collapse is not enough for the party in charge of things now. They’re strangely compelled to seek every possible opportunity to insult the public’s intelligence while destroying what’s left of American culture. Case in point out of Nancy Pelosi’s Congress: HR1, the so-called “For the People Act,” institutionalizing ballot fraud in US elections. The law would make permanent the Covid-19 emergency mail-in voting system, over-riding whatever each state’s election law says — which makes the act appear patently unconstitutional — plus permitting same-day motor-voter registration of any live body, citizen or not, plus removing all voter ID requirements, and much more to ensure the country is never again threatened by a fair election.

Next up: HR5, the so-called “Equality Act,” institutionalizing the notion that categories of “male” and “female” are mere cultural constructs and must in no way be allowed to order any cultural activity from school to work to leisure. The bill was initially conceived to harden into law President Obama’s EO expanding the Department of Education’s Title IX rules on school sports — which eventuated in “trans women” disrupting girls’ sports. Now, men pretending to be women (and vice-versa) will be allowed to disrupt everything else in American life, especially the civil courts, with frivolous lawsuits.

Also in the pipeline: HR6, the so-called “American Dream and Promise Act,” and its Senate companion, S264, the plain “Dream Act,” that will grant permanent residency and then citizenship to currently “undocumented” people who snuck into the USA as children. The dreams and promises have already been delivered, even before the final passage of any new act, with an unprecedented flood of unaccompanied migrant children crashing the border, as well as a surge of adults fleeing Mexico and Central America. Apparently, the thinking in Washington these days is that we don’t have enough poor people in America, that their lives are not difficult enough. The message couldn’t be clearer to millions outside the United States: by all means, cross the border and we will do nothing about it. And so, with the border reduced to just another cultural construct, Mr. Biden himself took the extraordinary action of telling them on TV, “Don’t Come!” I guess that’ll do the trick.

Do you have any idea how pissed-off a clear majority of the American public will be after a few more months of this?

According to media reports, there has been a mass shooting. As of now, it is unclear how bad the mass shooting is, or whether anyone should care about it– since authorities have not yet released the skin colors of the perpetrator and the victims.

“It’s possible this could be a horrific mass shooting we will talk about for years to come,” said one news anchor. “On the other hand, it may just be a run-of-the-mill mass shooting that we’ll forget by tomorrow since it doesn’t fit the narrative we are trying to sell right now. For the time being, please be sure to assume this shooting confirms all your most horrific biases about the state of our country. Stay tuned for more details– unless we decide you don’t really need to hear more details.”

Already, social media is buzzing with speculation and anger, confirming everything everyone already knew about how horrible the groups of people who they think are so horrible really are.

“Not surprised,” said one American. “This is America– the country where the exact people I hate are as horrible as I thought they were.”

The media has assured they will probably just hold off on reporting further details until the preferred narrative has had time to run its course.

UPDATE 5 PM ET:

The suspect in the Monday afternoon Boulder, Colorado supermarket shooting which left 10 dead is 21-year-old Ahmad Al-Issa from Arvada, Colorado, so expect this not to be classified as terrorism, and the motive to remain unclear for some time.

And, of course, the racism-white supremacy-Trump thread is done.

Though we’re sure Rachel Maddow and CNN will fill in the blanks.

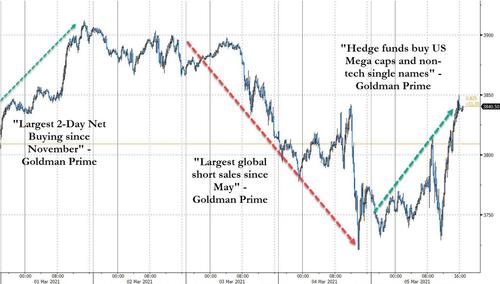

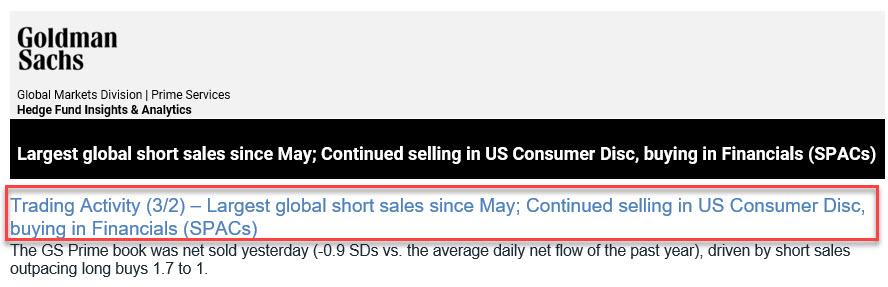

At the end of the first week of March which saw an eruption in violent market turbulence in the aftermath of the sharp spike in bond yields and the catastrophic 7Y auction we pointed out an observation from Goldman’s Prime Broker desk, which noted that halfway through the week, Goldman traders saw the “largest global short sales since May” with the GS Prime book was net sold yesterday (-0.9 SDs vs. the average daily net flow of the past year), driven by short sales outpacing long buys 1.7 to 1.” In fact, the mid-week puke wasn’t so much selling as short-selling, as “modest net selling (-0.5 SDs) was driven by short sales outpacing long buys 1.5 to 1.”

This prompted us to predict that what was coming would be a “mega squeeze” in stocks.

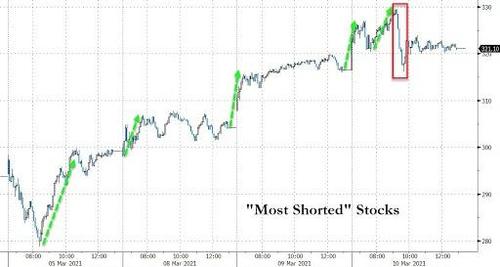

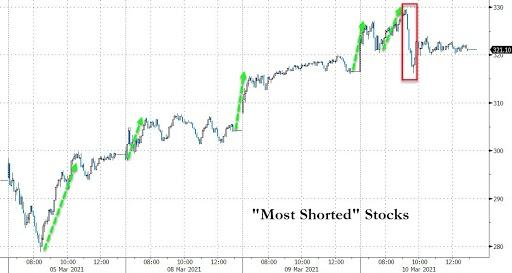

Sure enough just a few days later, on March 10, when stocks did explode higher in the second week of March, Goldman’s Prime Brokerage Service observed that Tuesday’s eruption was the result of “risk unwind in Macro Products vs. large net buying in Single Names” led by TMT and Consumer Disc stocks, with the Goldman Prime book net bought for a fifth straight day in which “trading flows were risk-off with short covers outpacing long sales 4 to 1.” And just to make sure there is no confusion, Goldman prime said that “yesterday’s de-grossing activity – short covers and long sales combined – was the largest since late January (-2.0 SDs).“

Furthermore, Bloomberg added that short covering in unprofitable tech firms helped the group halt seven straight days of selling and score the third-biggest net buying of the year. In fact, in the first two days of that week, Goldman basket of the most-shorted tech stocks soared 7%, more than double the return of the Russell 3000.

Commenting on the move, Andrew Brenner, the head of international fixed-income at NatAlliance Securities in New York told Bloomberg that “we see yesterday’s move as short covering without legs.” Ok fine, but tell that to any Nasdaq shorts whose legs – and everything else – was steamrolled in the historic move higher.

We concluded our post by saying that “with the latest iteration of shorts now out of the picture, it’s time for a new cohort of bears to take their place, and we wouldn’t be surprised if we see renewed weakness in the Nasdaq as a flood of new shorts hammers the tech index only to then suffer another massive squeeze and so on, rinse, repeat.”

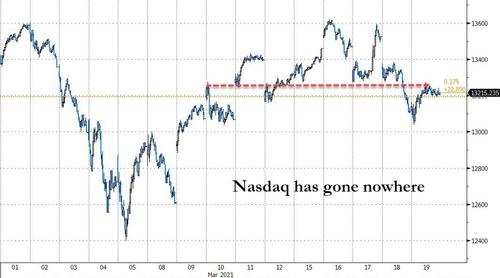

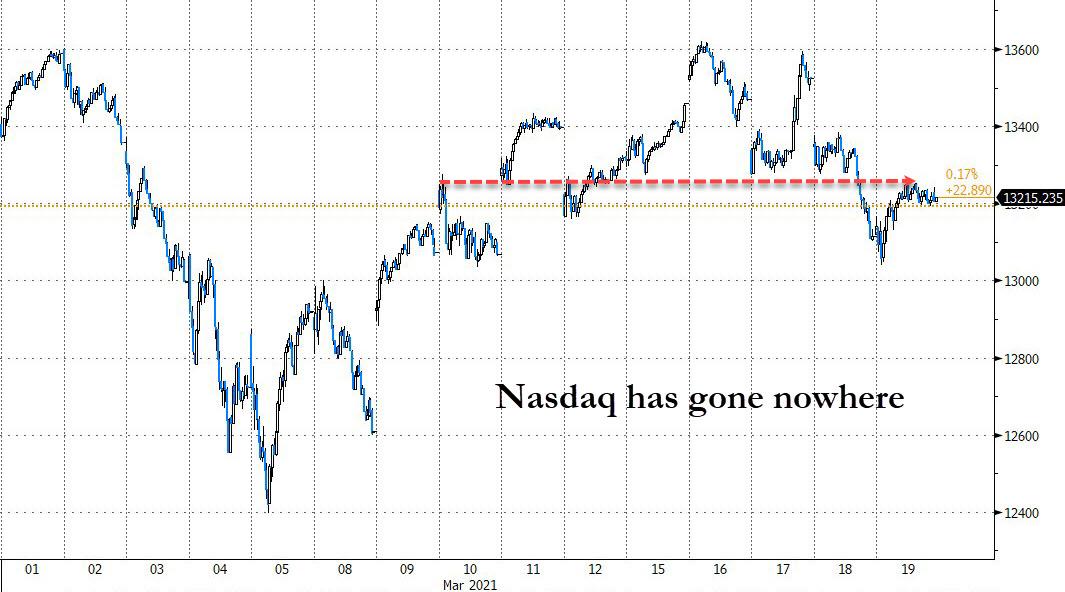

Well, one again that is indeed what happened because while the Nasdaq did move sharply higher for a few days, it closed on Friday precisely at the March 10 short squeeze high as every squeeze higher has been met with a fresh burst of shorting.

We bring all this up because we now have the latest Goldman Prime data and – drumroll – we appear to be headed for another mega squeeze!

As Goldman’s hedge fund client-facing desk wrote after the close on Friday, in a reversal of last week’s buying activity, “the GS Prime book saw the largest $ net selling since Dec ‘18 (-2.5 SDs), driven by short sales and long sales (3 to 1).” The bank then reveals that all regions and sectors saw increased shorting on the week with “Single Names/Macro Products were both net sold and made up 70%/30% of the $ net selling. With the exception of Asia which was net bought driven by long buying in Japan, all regions were net sold led by North America and Europe.” Finally, broken down by industry, “10 of 11 global sectors were net sold led by Consumer Disc, Comm Svcs, Info Tech, and Materials, while Financials was the only net bought sector.”

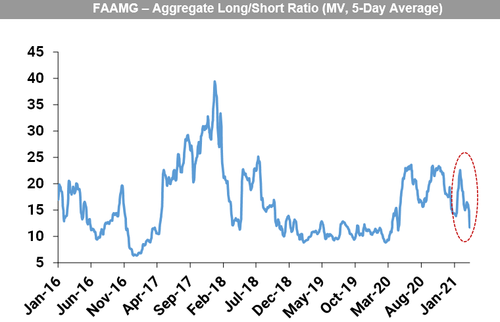

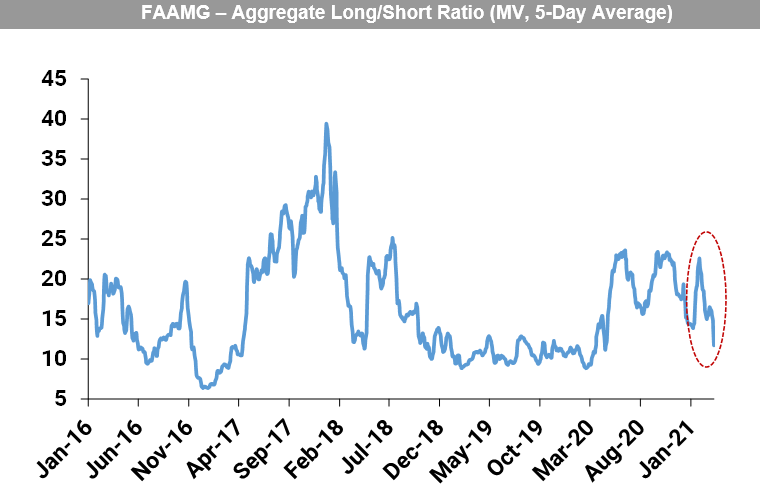

But what is most notable is that like two weeks ago, Goldman Prime reveals that “the largest net selling in US TMT Mega Caps since Mar ’20 driven by short sales” and the aggregate long/short ratio (MV) in FAAMG dropped -34% week/week on the GS Prime book to 10.41, which is the lowest level since Mar ’20 and in the 19th percentile vs. the past five years.

One final – and perhaps remarkable observation in light of the juggernaut that FAAMG had been for much of 2020 – the TMT Mega Caps (FAAMGs) collectively now make up 13.5% of the overall US net exposure in Single Names, down from 13.9% at the end of last week and 14.6% at the start of this year, according to GS Prime. The current level is in the 16th percentile vs. the past year and in the 55th percentile vs. the past five years. In short: traders are rapidly rotating away from the best performing sector of 2020.

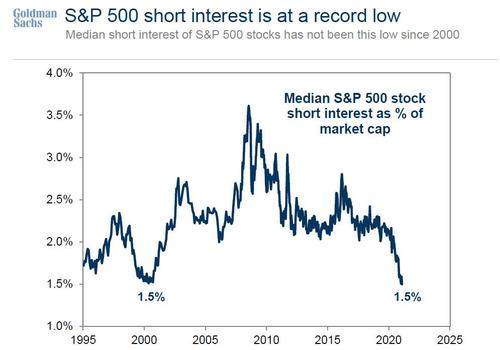

Adding insult to injury the latest Goldman Prime data also shows that hedge funds haven’t generated any net alpha since the start of 2020 (!) for one simple reason: while the longs are modestly in the green, it is the collective shorts that keep steamrolling the “2 and 20” space, and every time hedge fund layer on shorts, an initial spike in covering leads to a furious cascade of closing out of bearish positions perhaps as a result of the market’s muscle memory where every attempt to go short has lead to pain and suffering for the bears leading to the lowest marketwide net short in history!

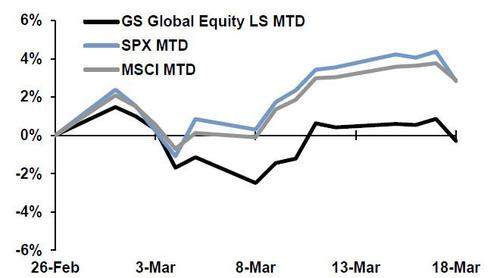

What does all this mean? Well, as a result of last week’s aggressive attempt to pile on shorts – the most since Dec 2018 when stocks collapsed due to Powell’s final rate hike which was seen as a huge policy mistake – we are once again facing the threat of a massive short squeeze, one exacerbated by the fact that hedge funds are now once again red for the year, as shown by the black line below…

… making them extremely jittery and likely to close out any potentially devastating shorts at the sign of even the faintest of bullish catalysts. Well, with not one, not two but three appearances by Fed Chair Powell this week, all eager to make up for his latest FOMC fiasco that sent yields to fresh 2021 highs, there will be ample triggers for another face-ripping squeeze in the week ahead, and we are confident that in just a few days we will be once again discussing the latest “mega squeeze” leading to another historic market meltup with the full blessing of the Federal Reserve.

Recall Tyler in Fight Club:

The first rule of Fight Club is: You do not talk about Fight Club. The second rule of Fight Club is: You do not talk about Fight Club. Third rule of Fight Club: someone yells stop, goes limp, taps out, the fight is over. Fourth rule: only two guys to a fight. Fifth rule: one fight at a time, fellas. Sixth rule: no shirts, no shoes. Seventh rule: fights will go on as long as they have to. And the eighth and final rule: if this is your first night at Fight Club, you have to fight.

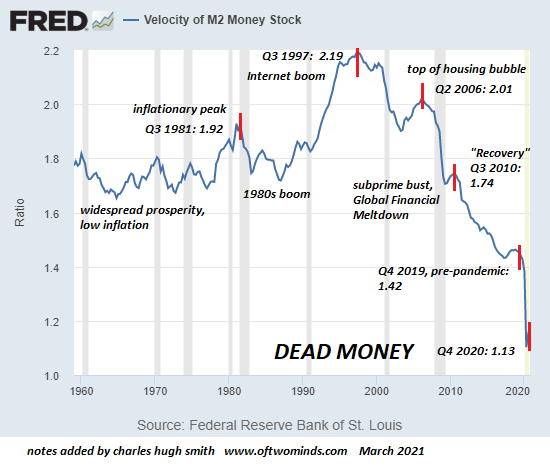

In the era of widespread prosperity in the 1960s and 1970s, the velocity of money ratio remained in a band between 1.7 and 1.8, moving up toward 2 in the inflationary late 70s as it made sense to trade cash that was losing value for goods and services before it lost even more purchasing power.

Velocity returned to this range in the 1980s boom, and then rocketed to postwar highs at 2.2 in the Internet boom of the 1990s. Since that top in 1997, money velocity has been in a secular decline. As every Fed-inflated financial bubble pops, money velocity takes another leg down. Even before the pandemic, it was in a steady free-fall even as the supply of money steadily rocketed higher.

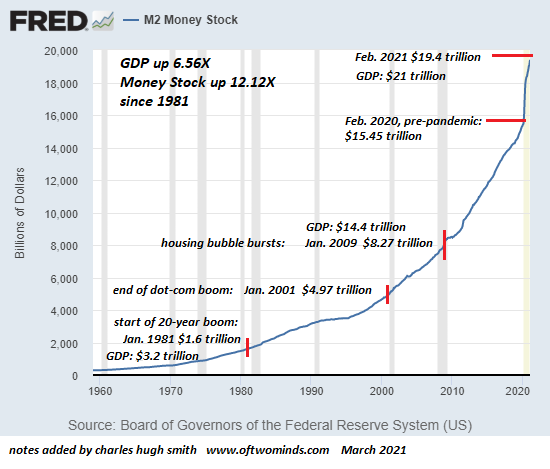

So what do we make of this stunning expansion of money and equally stunning collapse of money velocity? Ours is a Dead Money Economy. New money is created in the trillions of dollars, but it is either shipped overseas to exporters selling goods to Americans or it’s being stashed somewhere rather than being exchanged for domestically produced goods and services.

Despite the record unemployment rate, widespread hardship to businesses, strains on the healthcare system, political turmoil, and general disruption to daily life in 2020, U.S. consumers have managed to ramp up their habit of buying things. Demand for physical goods replaced some of the previous demand for in-person service-related experiences and much of that demand was met with a surge of imports from China as domestic production slowed down due to lockdown measures. Up until recently, global supply chains managed to find their footing and could meet demand, but news has emerged that reveals stresses on the world’s shipping infrastructure and uncovers clues about the economic outlook.

Container Shortage and Chinese Exports

Global logistical networks recently began to suffer from a shortage of shipping containers as demand has suddenly risen. Freight rates from China to the U.S. have jumped by 300%. The container situation has become so extreme that hundreds of thousands of containers have been sent off empty from U.S. ports, mostly to China as exporters demand empty containers with increasing urgency. An estimated 177,938 containers, were rejected from loading U.S. export items at the ports of Los Angeles and New York/New Jersey alone and then sent across the Pacific.

The recent imbalance of shipping containers illustrates the latest state of affairs surrounding the US and Chinese economies. As exports of consumer goods from Asia eclipse exports of mostly commodity and raw materials from the U.S. — in this case, even blocking US agricultural exports from having shipping containers to reach foreign markets — the trade deficit between the two countries may become more important to these highly competitive economies.

When Trade Deficits Matter

The Austrian perspective on the U.S. trade deficit has long been that given the continued relative productivity of the U.S. economy, foreign desires to invest in the U.S., and demand for the dollar abroad, the trade deficit is a ‘pseudo-problem.’ The US competitive advantage vis-à-vis other countries in recent decades has made running a trade deficit highly probable and even favorable for Americans as they enjoy the consumption of cheaper imports.

Thus far, the parties involved have been satisfied with this arrangement as U.S. consumers bring in goods at favorable prices and producers receive a reliably stable world reserve currency; the U.S. dollar. However, the underlying conditions particular to the U.S. economy in relation to China may be changing. There are two aspects of the U.S.-China trade deficit that merit attention. The first is the effect of net consumption by the U.S. coupled with dovish monetary and fiscal policies whereas the second is what China plans to do with U.S. dollar accumulated through exports.

On the U.S. side of the equation, easy money from the central bank coupled with fiscal stimulus extended to consumers has juiced buying activity as the lockdowns have forced people to stay home and spend. It’s no wonder that shipping containers are rushing to get back to China. With the U.S. taking big hits to production and foreign investment in 2020, along with explosive increases in the money supply, critical questions arise regarding the nature of this trade deficit and how long the status quo can continue as the country pushes the boundaries of its exorbitant privilege. Indeed, the health of the dollar itself as it relates to trade deficits would be an indicator to watch in coming years.

In running a trade surplus with the U.S., China has traditionally exchanged its U.S. dollars for U.S. Treasuries to add to its balance sheet and to maintain its export advantage. In recent years, however, China has reduced its holdings in Treasuries. This trend has also coincided with massive spending on the part of China in the last decade on the Belt and Road Initiative (BRI) infrastructure and trade corridor project which involves 71 countries across Eurasia and Africa that encompass two-thirds of the global population and one-third of world GDP.

Given the continued global dollar demand, it would be shrewd for China to use accumulated dollars to acquire foreign assets and invest in projects that have the potential to generate future income. The trade war with the US in recent years has driven China to deepen its flow of trade toward surpluses with other emerging markets and forge strategic global relations.

As containers carry goods from China to the U.S. and rush to return empty to bring more, the moment provides a glimpse into a potentially precarious arrangement between the two countries. While the U.S. presently consumes itself into debt and liabilities, China has leveraged its productive surpluses from this relationship into increasingly influential assets that may strengthen its position and further challenge the U.S., and perhaps even the dollar itself.

In a nutshell, the Federal Reserve is printing money and the US government is giving it to unemployed people who aren’t producing anything. As Peter pointed out, “They’re buying the stuff that people in other countries are employed making.”

“So, it’s the productivity of the rest of the world that Americans are living off of, and the trade deficit evidences that and shows you that our whole economy, our whole recovery, is a fraud.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}