ALBANY, NY—New York Governor Andrew Cuomo apologized this weekend for his long-standing habit of sexually abusing young women he holds power over. And while that all sounds quite bad, Governor Cuomo did make it clear to the public that he always wore a mask and socially distanced during these interactions– a fact that has some folks saying he should get off free.

“I have the greatest respect for my employees,” Cuomo explained during a press conference. “Especially the girls—we’ve got a lot of young girls on staff who do a really good job.” Cuomo paused for a moment and seemed to wink at someone offscreen. “And I can guarantee you right now, sure I might be a sexual predator, but not once did I remove my mask, never once broke the six-foot rule during conversations with my girls– at least in 2020. Isn’t that right, Kelly?”

Cuomo went on to explain how some of his sexual jokes may not have landed with the women since they couldn’t see his facial expressions. He also claimed that the women may have misheard him since his words were muffled by his mask and they were standing so far apart.

“Do I regret making those comments?” Cuomo asked as he stood up to leave the press conference. “No. Now if you’ll excuse me I’ve got some strip poker, er– I mean poker, to play.”

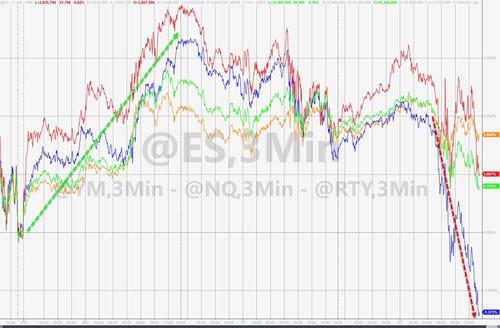

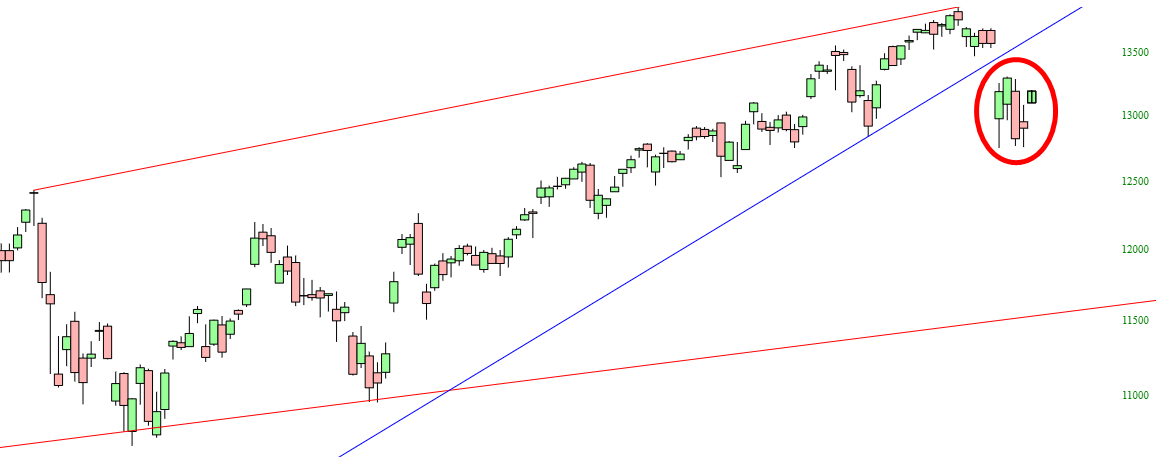

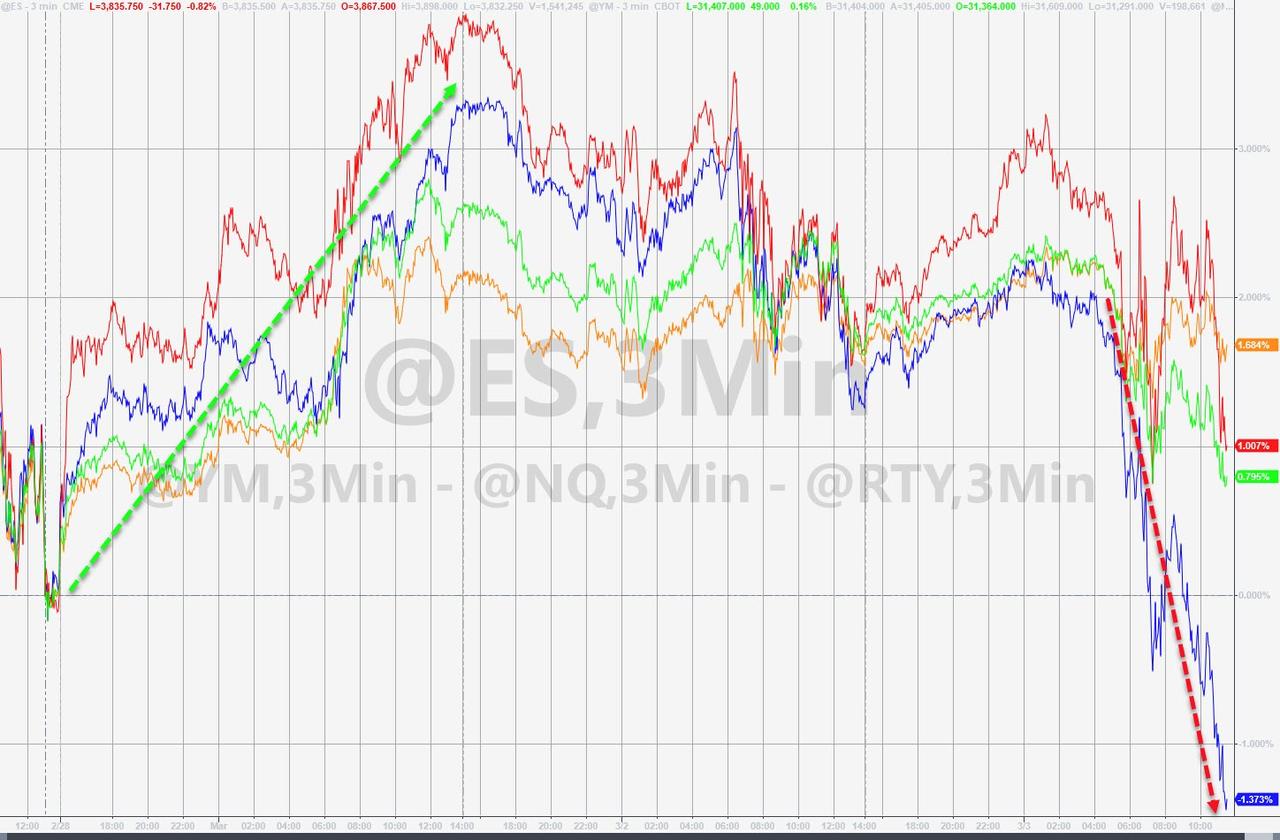

Things have accelerated south as the day wears on, with US equities all down hard led by a 2.5% plunge in big-tech.

Nasdaa is now down almost 1.5% since the end of February (and down almost 5% from Monday’s exuberant highs)…

The losses sped up as Nasdaq broke below its 50-day moving-average…

…and is clinging to the 13,000 level… and 12,800 is the nest level to test

As SpotGamma warned last night, positive gamma refuses to materially build around current SPX price levels, and as such we are growing quite concerned that markets are increasingly susceptible to a “sucker punch”.

If I may quote Faruq Taheed:

“Ladies and gentlemen, are you ready? It’s Robot Fighting time!”

The UAH lower troposphere temperature trends are turning south as the weaker Solar Cycle 25 continues into the Modern Solar Minimum.

The full UAH Global Temperature Report, along with the LT global gridpoint anomaly image for February, 2021 should be available within the next few days here.

The global and regional monthly anomalies for the various atmospheric layers should be available in the next few days at the following locations:

The high frequency solar minimum between Solar Cycle 24 and 25 happened in December 2019, when the 13-month smoothed sunspot number fell to 1.8. Solar Cycle 25 with peak sunspot activity expected in July 2025.

Solar Cycle 24 had the 4th-smallest intensity since regular record keeping began with Solar Cycle 1 in 1755. It was also the weakest cycle in 100 years. Solar maximum occurred in April 2014 with sunspots peaking at 114 for the solar cycle, well below average, which is 179.

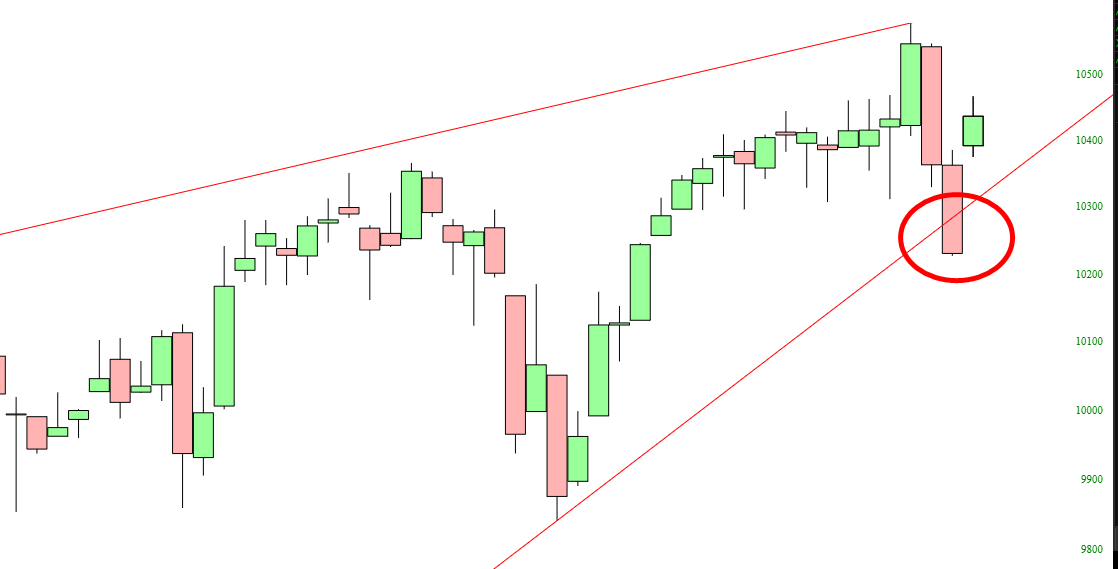

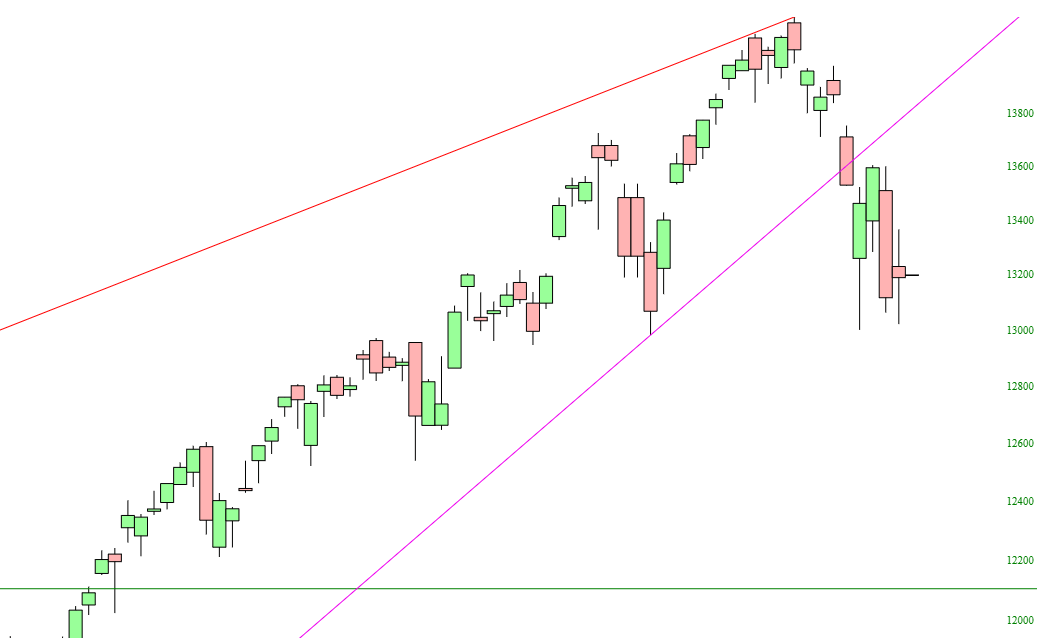

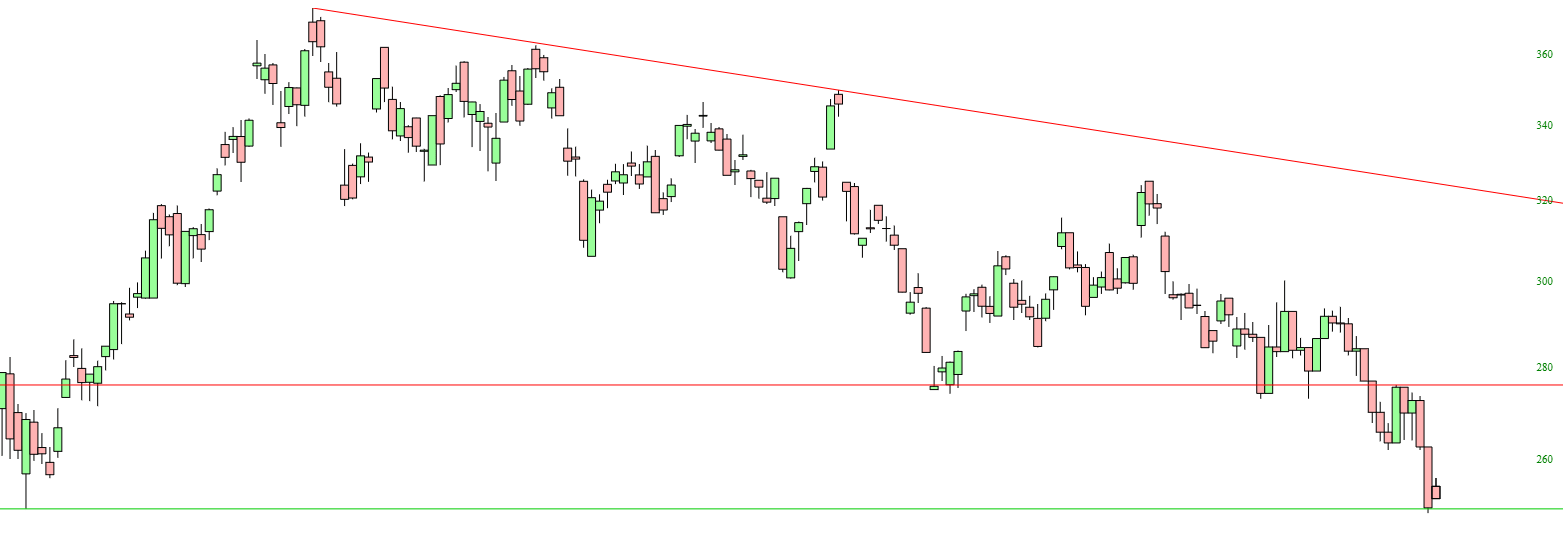

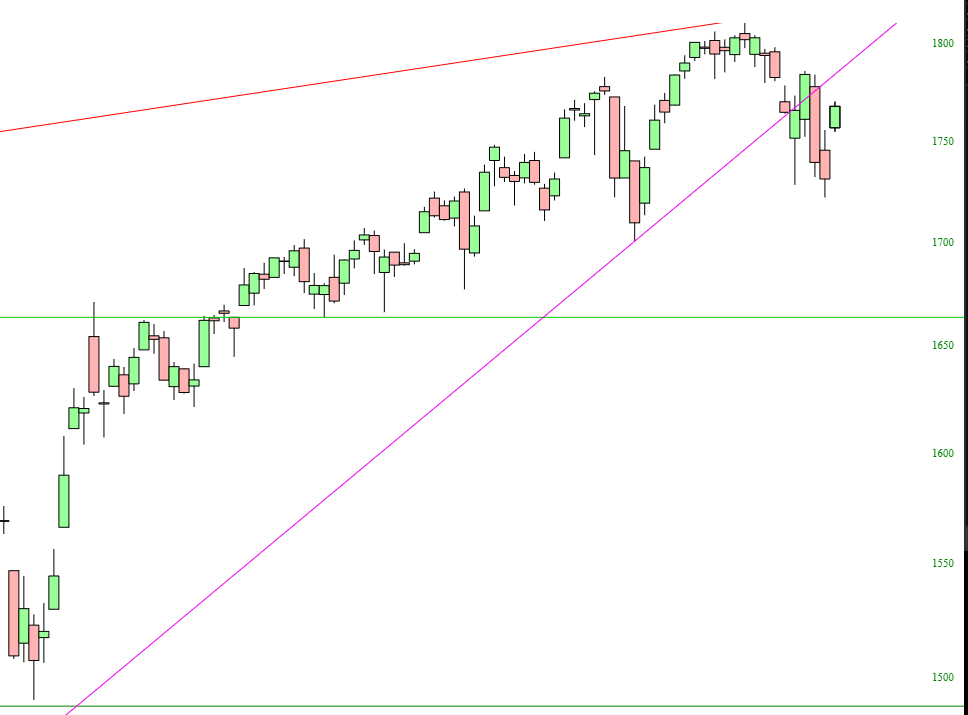

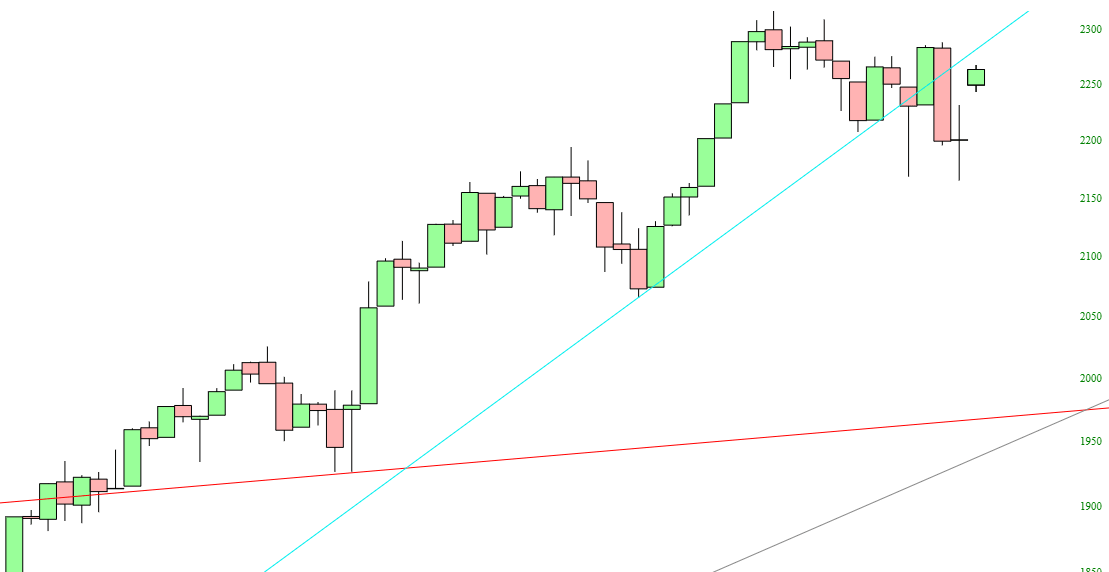

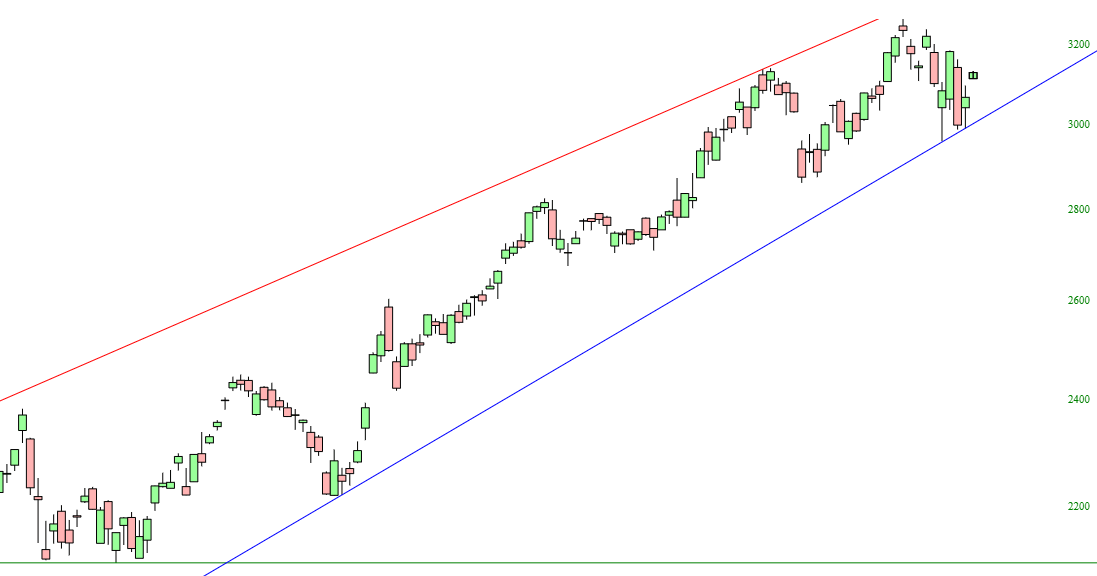

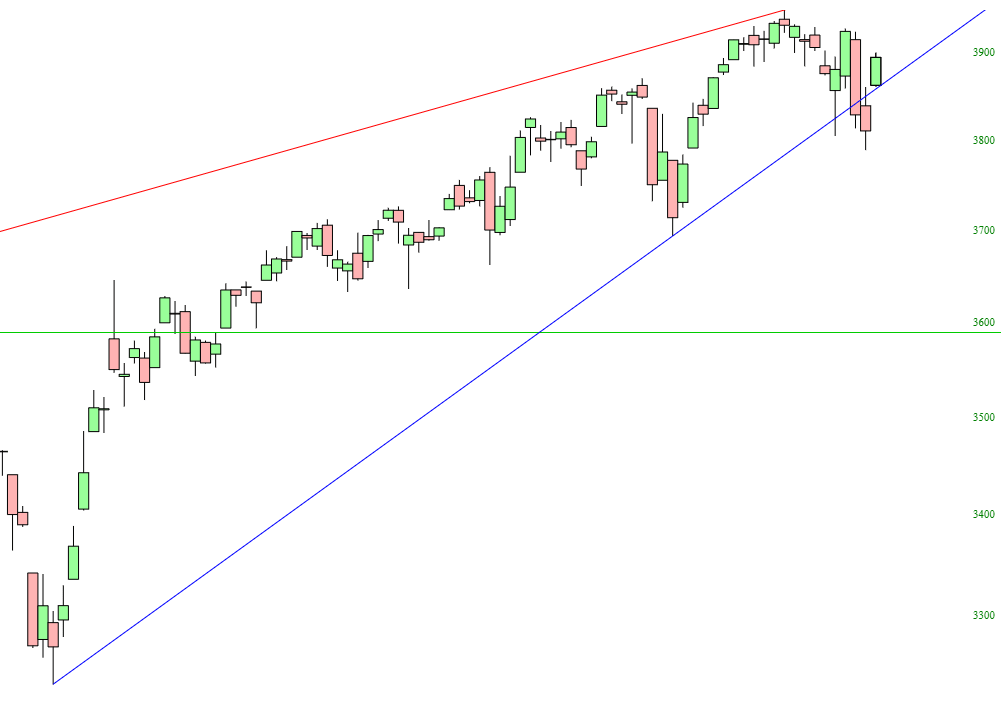

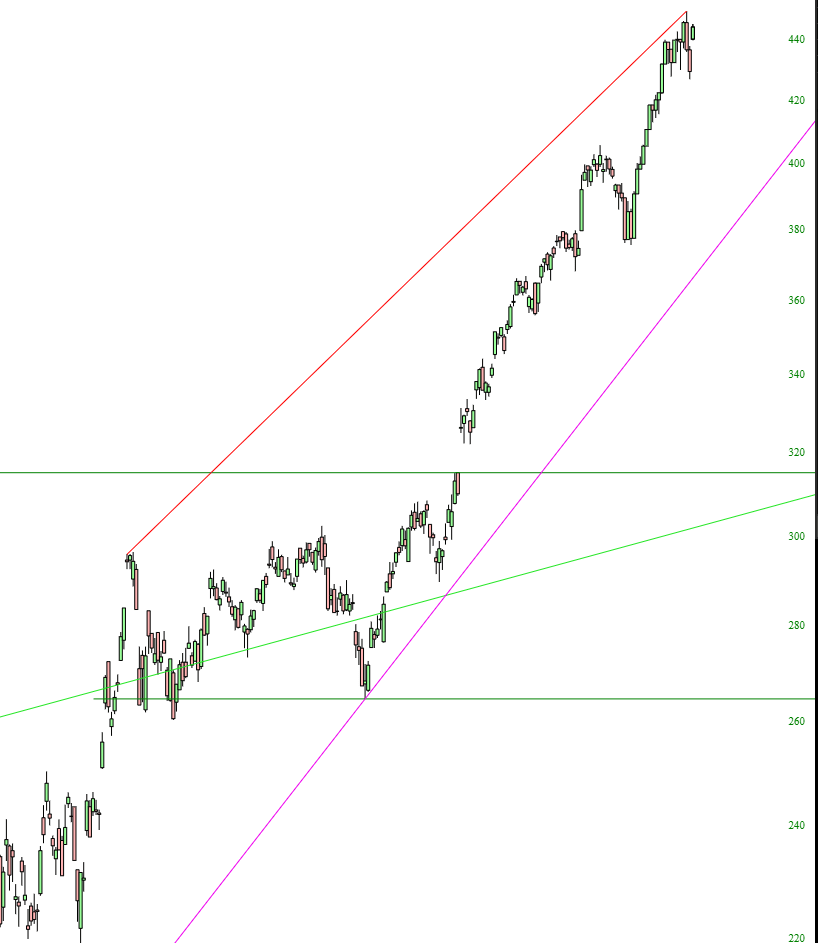

With the giant reversal taking place today, let’s take a fresh look at some important indexes, in alphabetical order.

First is the $COMP, the Dow Jones Composite. This cracked through its trendline on Friday, but it has sprung right back above it. We’ll see if the damage done last week actually signals anything, or if this was just a one-day anomaly. My view is that the trendline break is meaningful.

The NASDAQ Composite hasn’t been quite as forgiving, since its trendline damage was much worse. It spent the entirety of last week below the broken trendline.

Ever since August 6th of last year, precious metals have stunk out loud. We might get a bounce in the gold bugs index, but I think that horizontal line will be the limit.

Similar to the $COMPQ, the NASDAQ 100, symbol NDX, is quite plainly below broken support.

The S&P 100, symbol $OEX, remains below support as well, in spite of the very sizable rally this morning.

The same can be said of the Russell, since last Thursday’s drop was so substantial.

One area of resolute strength for the bulls is the semiconductor index, symbol $SOX, which has been safely within its channel for going on a year now.

The S&P 500, symbol $SPX, teased us all a bit late last week with a trendline break, but it has clamored back above it. We are still below lifetime highs, and I think the ecstasy over the $1.9 trillion in free money that’s about to be distributed will be transitory.

Just as the semiconductor space has been unbroken, so, too, has the Broker/Dealer Index (symbol $XMI). We are sky-high on this.

Lastly, the most vulnerable sector, in spite of all the breathless enthusiasm about crude oil, is the Oil & Gas sector (symbol $XOI). The run-up has been sensational, but that is a massive and powerful top.

You can see the outflow. to the trading houses But where’s the in-flow?

Beginning on September 17, 2019 – months before there was any report of a COVID-19 case anywhere in the world – the Federal Reserve turned on its money spigot to the trading houses on Wall Street. By October 23, 2019 the Fed announced that it was upping these loans to $690 billion a week – again, months before any report of COVID-19 anywhere in the world. Earlier in October 2020, the Fed had also announced that it would be buying back $60 billion a month in Treasury bills.

Within a span of six months, the Fed had pumped out a cumulative $9 trillion in loans to Wall Street’s trading houses, according to its own spread sheets, with no peep as to which Wall Street firms were getting the bulk of that money. It’s more than a year later and the American people still have no idea what triggered that so-called “repo loan crisis” or which Wall Street firms were in trouble or remain in trouble.

The Federal Reserve, as is typical, outsourced this money spigot to the New York Fed, which is literally owned by some of the largest banks on Wall Street. We wrote at the time the New York Fed was making these massive repo loans that this action was unprecedented in Federal Reserve history for the following reasons:

No Wall Street crisis has been announced to the public to explain these massive loans and Treasury buybacks;

Not one hearing has been held by Congress on the matter;

Not one official elected by the American people has authorized these loans;

The loans are not being made to commercial banks (which could re-loan the money to stimulate the U.S. economy). The loans are going to the New York Fed’s primary dealers, which are stock and bond trading houses on Wall Street who count hedge funds among their largest borrowers; (See list below. There is only one bank among the 24 primary dealers.)

Many of the primary dealers are units of foreign banks whose share prices have been in freefall. The Fed is making these loans at approximately 2 percent interest – an interest rate these firms could not come anywhere close to obtaining in the open market;

These same foreign banks are counterparties to mega U.S. banks’ derivative trades – raising the suggestion that this is another bailout of Wall Street’s derivatives mess as occurred in 2008;

The Dodd-Frank financial reform legislation of 2010 was supposed to rein in this exact type of abuse by the New York Fed and, in fact, it states that Congress must be informed as to which banks are receiving the money to be sure it’s not going, once again, to failing financial institutions as happened in the last crisis;

The Government Accountability Office (GAO), when it released its audit of the Fed’s bailout programs of 2007 to 2010 chastised the Fed for failing to document the reasons it was flinging trillions of dollars to Wall Street and foreign banks. Notwithstanding the GAO’s report, the New York Fed is back to its old tricks again;

The New York Fed is owned by its members banks in its region. Representatives of these banks sit on its Board of Directors. It is thus too conflicted to be in charge of this bailout money spigot which is ultimately backstopped by the U.S. taxpayer if the New York Fed fails;

The New York Fed is the regulator of the largest bank holding companies in the U.S. But its failure as a regulator is why these same banks needed to be massively bailed out in 2008 and, apparently, again now. This system lacks any semblance of checks and balances;

The parent organizations of five of its primary dealers have admitted to criminal felony counts brought by the U.S. Department of Justice for frauds against the investing public. Bailing out felons and Wall Street firms with serial histories of wrongdoing perpetuates moral hazard and, thus, more wrongdoing and bailouts.

The House Financial Services Committee has announced that it will hold a hearing on March 23 titled: “Oversight of the Treasury Department’s and Federal Reserve’s Pandemic Response.”

This is part of the ongoing series of hearings where both the U.S. Treasury Secretary and Federal Reserve Chairman show up to pretend that the American people are receiving complete transparency on what the Fed is doing with its money creation powers. (It’s another one of those Big Lies that have come to dominate this era of American history.) While former Treasury Secretary Steve Mnuchin and Fed Chair Jerome Powell starred in this dog and pony show last year, the March 23 hearing will hear from the new Treasury Secretary and former Fed Chair, Janet Yellen, along with Powell.

There is little hope of seeing any new sunshine from this pair, since Yellen hasn’t even disclosed the millions of dollars she received in speaking fees from Wall Street banks and trading houses in 2018, the year she stepped down as Fed Chair. As for Powell, hope for transparency was extinguished when we reported in August of last year that the Wall Street investment manager, BlackRock, was managing upwards of $25 million of Powell’s personal money while landing three no-bid contracts with the Fed to manage part of its emergency lending programs. One of those programs, the Secondary Market Corporate Credit Facility, allowed BlackRock to buy back its own sinking Exchange Traded Funds, some of which were invested in junk bonds.

The Fed has gone out of its way to foster the impression that its middle name is transparency. For example, on April 23 of last year it issued a press release which said:

“Building on its strong record of transparency and accountability around financial reporting and the policymaking process, the Federal Reserve Board on Thursday outlined the extensive and timely public information it will make available regarding its programs to support the flow of credit to households and businesses and thereby foster economic recovery. Specifically, the Board will report substantial amounts of information on a monthly basis for the liquidity and lending facilities using Coronavirus Aid, Relief, and Economic Security, or CARES, Act funding….”

Indeed, the Fed is reporting a substantial amount of information on a monthly basis on some of its Section 13(3) emergency lending facilities, but no one in Congress is demanding transparency on its previous $9 trillion in cumulative repo loans or on three of its ongoing emergency lending facilities that have yet to release one name of a loan recipient: the Primary Dealer Credit Facility (PDCF), the Commercial Paper Funding Facility (CPFF), and the Money Market Mutual Fund Liquidity Facility (MMLF).

The PDCF, CPFF, and MMLF were the first three Section 13(3) emergency lending facilities created by the Fed. All three programs were created in mid-March of 2020. Today is the first day of March 2021 and yet not one name of a loan recipient in those three programs has been released by the Fed.

According to the Fed’s H.4.1 report for Wednesday, April 1, 2020, just weeks after creating the PDCF and MMLF, they had, respectively, loaned out $33 billion and $52 billion to unnamed Wall Street firms.

The Commercial Paper Funding Facility first made an appearance on the Fed’s H.4.1 release on Wednesday, April 15, 2020. At that point, it had already made $974 million in loans to a Special Purpose Vehicle (SPV) that was created to buy up commercial paper that was, ostensibly, too toxic to roll over or find an alternative market for issuance. The end recipient of this Fed largesse has yet to be named.

The CPFF continued to grow exponentially each month after its creation, reaching $12.8 billion by June 17, 2020, according to the Fed’s H.4.1.

The Fed’s most recent H.4.1 for February 24, 2021 shows the following outstanding loans to these three emergency facilities that have never reported one name of the ultimate loan beneficiary: $265 million for the PDCF; $1.6 billion for the MMLF; and $8.6 billion for the CPFF.

Trust will continue to erode in both Wall Street and the Fed until Americans get a transparent accounting of where this money went and why it went there.

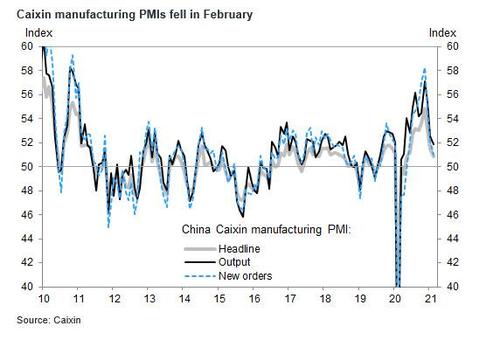

China’s Caixin manufacturing PMI fell to 50.9 in February from 51.5 in January, though still in expansionary territory. Most sub-indexes implied growth momentum moderated in the manufacturing sector. The production sub-index dropped to 51.9 in February from 52.5, and the new orders sub-index fell to 51.0 from 52.2. The new export order sub-index edged up only marginally to 47.5 from 47.4, still below 50 due to the resurgence of COVID-19 infections globally as highlighted by surveyed companies.

Surveyed companies remained cautious in hiring and the employment sub-index fell slightly to 48.1 from 49.6 in January. The raw materials inventory sub-index rose by 0.6pp to 48.8, but the finished goods inventory index edged down to 50.3 from 51.0. Stock shortages and travel restrictions continued to affect suppliers’ delivery in February. Price indicators suggest inflationary pressures moderated slightly but remained relatively high due to rising raw material prices and transportation costs according to the survey. The input price index fell slightly to 58.1 from 58.9 in January, and the output price index was 53.5, moderating from 54.9 in January. On future output, surveyed companies remained optimistic and expect “rising client demand globally once the pandemic comes to an end and planned product releases make debut”.

If that wasn’t enough, a former finance minister warned fiscal risks remain “extremely severe with risks and challenges”, with low revenue for five years ahead and no prospect of any spending cuts ahead, suggesting policy may need to be tightened at some point

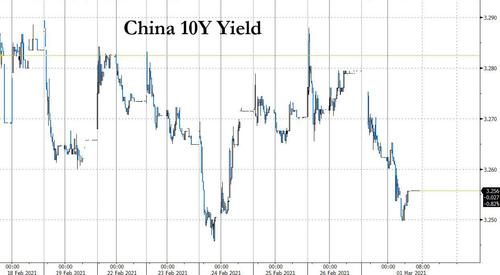

In kneejerk response, China’s 10-year government bond futures closed 0.3% higher, the most since Dec. 22, while In the cash bond market, the yield on 10-year sovereign notes dropped 2 bps to 3.26%, having barely budged in the past week and completely oblivious to the turmoil gripping the rest of the global bond market.

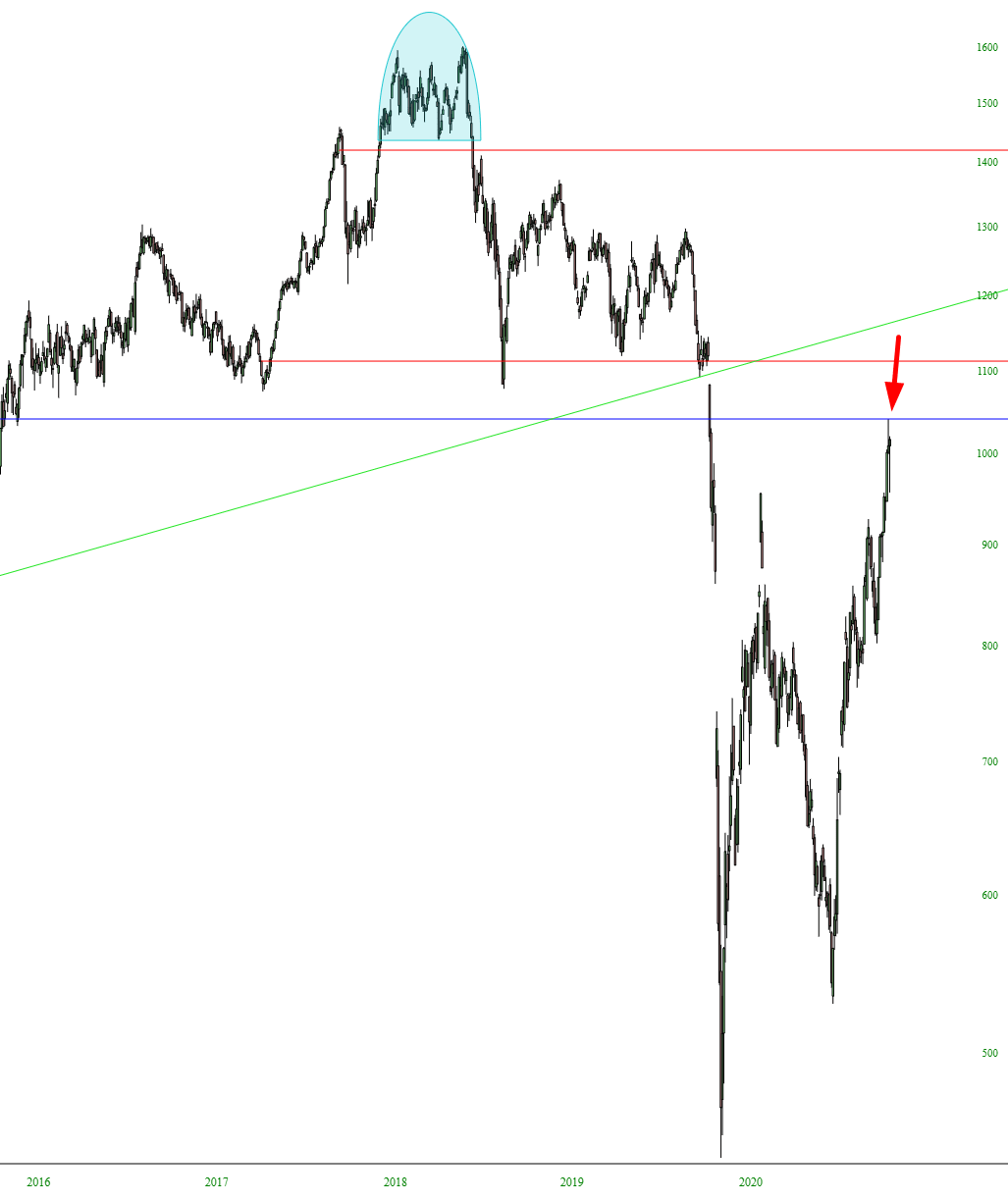

Very early, initial signal of a possible reversal in real estate: the 3x Bearish Real Estate ETF (DRV) broke its downtrend. Some other charts that look interesting in the real estate space. Some are failing at their initial pandemic gaps, some look relatively weak and could be starting meaningful breakdowns if they lose support (assuming a larger bearish move is underway in the market), while others are near pre-pandemic highs.

Check out some “playa”s:

“Investors may think the economic recovery in China has become less strong than expected, which could stoke risk-off sentiment in the short run and help bonds,” said Hao Zhou, senior emerging markets economist at Commerzbank AG in Singapore.

China’s economy is now fading and its credit impulse is set to shrink rapidly.

Not only will this affect reflation assets but also push yields lower. However, thanks to the 6-12 month diffusion lag of China’s credit impulse, we first have about 9 more months of higher yields and commodity prices before the hangover finally arrives.

For more than a year the reverse‐transcriptase polymerase chain reaction (RT‐PCR) test for viral load has been considered a “gold standard” in the diagnosis of CCP/CoVid-19 infection.

Should it be?

RT-PCR is a laboratory technique combining reverse transcription of RNA into DNA and amplification of specific DNA targets using polymerase chain reaction. This technique’s “transformation and amplification” process infers the amount of a specific RNA by monitoring the amplification reaction using fluorescence. Real-time PCR or quantitative PCR (qPCR) are commonly used for analysis of gene expression and quantification of viral RNA in research and clinical settings.

However, the amplification process has its drawbacks. The well-described long tail of RNA positivity after the transmissible stage means that many, if not most, people whose infections are detected during routine surveillance using high-analytic-sensitivity tests are no longer infectious at the time of detection (Mina et al., 2020). Depending on when the test is taken, one could have a positive result and yet be in the post-infectious stage.

A particularly high Ct count further expands the response curve to include larger fractions of post-infectious load.

As reported in The New York Times, most than 50% of infections in Massachusetts and New York identified by PCR-based surveillance had PCR cycle threshold values in the mid-to-upper 30s, indicating low viral RNA counts. Thousands of people are being sent to 10-day quarantines after positive RNA tests despite having already passed the transmissible stage of infection (Mandavalli, 2020).

The exponential growth of the reverse transcribed complementary DNA (cDNA) during the multiple cycles of PCR produces inaccurate end point quantification due to the difficulty in maintaining linearity (Gettemy and Gold, 1998). Combined with detecting post-infectious conditions,

RT‐PCR may also increase the positivity rate, depending on the number of repetitions of this test.

Thus, knowing the cycle number (Ct) is crucial to an accurate and reliable CoVid diagnosis. Per Umemneku et al. (2019), RT-PCR tests are NOT the gold standard.

It is crucial to evaluate diagnostic accuracy studies, analytical validity, and testing for agreement in CT, RT‐PCR, and antibodies tests at the different clinical stages. For the moment, and whenever possible, it is more useful in clinical practice to evaluate tests by several methods because there is no generally accepted reference standard.

Well, Trump isn’t president – sorry, couldn’t resist that one. But interesting timing coincidence anyway.

But why indeed?

As OG observes:

It’s not the vaccines – not even a tenth of the population has been vaccinated while the drop is happening simultaneously in different countries all around the world, and not every country is vaccinating at the same rate or even using the same vaccine.

It’s not the lockdowns – “Sweden, famously, never locked down at all. Yet their “cases” and “Covid related deaths” have been dropping exactly in parallel with the UK”

So why?

Well, here’s OG’s take, referring to the graph on the top of the page:

As you can see, the global decline in “Covid deaths” starts in mid-to-late January.

What else happened around that time?

Well, on January 13th the WHO published a memo regarding the problem of asymptomatic cases being discovered by PCR tests, and suggesting any asymptomatic positive tests be repeated.

What we’re seeing is a decline in perfectly healthy people being labelled “covid cases” based on a false positive from an unreliable testing process. And we’re seeing fewer people dying of pneumonia, cancer or other disease have “Covid19” added to their death certificate based on testing criteria designed to inflate the pandemic.

Mina, M. J., Parker, R., & Larremore, D. B. (2020). Rethinking covid-19 test sensitivity – A strategy for containment. The New England Journal of Medicine, 383(22), e120.

Umemneku Chikere CM, Wilson K, Graziadio S, Vale L, Allen AJ. Diagnostic test evaluation methodology: a systematic review of methods employed to evaluate diagnostic tests in the absence of gold standard—an update. PLoS One. 2019;14(10):e0223832. https://doi.org/10.1371/journal.pone.0223832

In this issue of The Institutional Risk Analyst, we focus on the global tendency toward inflation even as economists insist that price increases remain too low. Everything from bank stocks to bitcoin has been lifted in nominal value by the manic actions of central banks, which make assets scarce even as these banksters with PhDs subsidize exploding public debt issuance. Thus long term bond yields are rising in response.

Do you think Tesla (NASDAQ: TSLA) or bitcoin are the only assets rising fast in this Fed-induced inflation? No. Can you have inflation and debt deflation at the same time? Yes, this QE-fueled price surge is just a pause in the general tendency toward debt deflation. The confluence of these two facts may mean growing demand for dollars and dollar assets in the near term, not less as some analysts suppose. But little of this helps American consumers in terms of jobs or real income.

The flow of new IPOs in the equity markets propelled by special purpose acquisition companies or SPACs illustrates the problem. The special purpose vehicle, of course, is generating returns for the sponsors. Creating investor value is another matter. It is interesting to note that in 2020, more than $12 billion in SPACs were financed via PIPEs, or private investments in public equity.

PIPEs “are mechanisms for companies to raise capital from a select group of investors outside the market,” CNBC reports. “But as PIPEs are increasingly being deployed in conjunction with a surge in SPAC mergers, a larger group of fund managers are seeking access to this security, with limits on who and how many can invest. The heightened prevalence of this product is raising concerns about the potential lack of understanding among the broader cohort of SPAC investors about how these investments work.”

Even as Washington goes off the rails in terms of fiscal policy and many other aspects of national governance, around the globe demand for dollars and near-derivatives is growing. And even as the purchasing power of the dollar declines, the greenback’s popularity grows inversely to value. Liquidity, not quality, is the key criteria it seems.

When we hear people talk about the impending collapse of the dollar, we naturally think collapse into what precisely? When we sell dollars, we take what on the other side of the trade? Bitcoin? Gold? Euros? Nope, too small. None of the available substitutes even begins to have sufficient mass to act as an alternative to the dollar.

Ponder the dilemma of the Middle Kingdom under dictator Xi Jinping. Even as China attempts to use a “dual circulation” strategy to rebalance the economy away from dependence upon the US and other nations, and toward greater focus on supposed internal demand, it faces few good financial alternatives to export led growth. The yuan is inconvertible and cannot support significant investment activity. Only the dollar is big enough for China’s economy.

The tortured liquidation of HNA suggests China remains financially unstable, in part because of the clumsy policies of the Chinese Communist Party. As Barron’s notes, we are still at the beginning of this financial unwind. “It wasn’t cheap credit that led to excesses of HNA or for that matter Anbang, Ant, or Wanda Dalian, but a shift in government policy,” Yukon Huang, senior fellow at the Carnegie Endowment for International Peace and former World Bank country director for China, told Barron’s.

The combination of financial incompetence and rigid policies emphasizing state-led growth, seems hardly a prescription for success. Again, the very messy unwind of HNA is the result of deliberate government policy in Beijing. Just as the majority of US economists think inflation is not a problem, a majority of foreign analysts of China believe that the country’s growing dependence upon state run enterprises and party direction is somehow bullish for economic growth. The HNA example suggests otherwise.

Meanwhile in the US, chaos reigns supreme. The Congress is in a state of disarray after completing the second, unsuccessful trial of President Donald Trump. The city built upon a swamp is focused upon negotiations for economic rescue legislation, but is a rescue required? Outside Washington, an economic surge led by housing is building due to the latest round of monetary manipulation by the Federal Open Market Committee.

The US is in the midst of a bull market in residential real estate that easily rivals the mid-2000s. Not only are home prices currently rising at rates higher than in 2005, but the rate of increase is accelerating due to scarcity of existing homes in many markets. Suburban residential and commercial assets are in great demand, as evidenced by the migration of people and business out of urban centers such as New York City.

In upscale destination markets around the country, more than a decade worth of inventory of pricey and thoroughly overbuilt vacation homes has been consumed in the past year. A wave of buyers fled urban areas such as San Francisco, Los Angeles and Chicago for the less crowded climes of Idaho, Colorado, Utah and Montana. None of these folks are waiting for $1,400 checks from Washington.

A torrent of smart and entitled money crashed upon these small markets and their residents, causing swings in property values that leave many real estate professionals agape. But aside from the benevolence of coastal cash liquefying often glacial mountain real estate markets, there is not a great deal of benefit here for the US economy. Just another ridiculous and entirely American style misallocation of resources and on a transcontinental scale.

When the great correction from the equally great monetary easing comes in 2025 or 2026, prices for homes, stocks and yes even TSLA and bitcoin are likely to suffer. The generic wave of demand for assets will subside and prices will begin to reflect some notion of fundamental value. Just remember that 2020 is likely to be the floor of the next market reset five years out. The price increases between now and then are, well, pure inflation.

And after the great correction, the dollar will still be the global means of exchange, but Americans will have lost a huge amount of purchasing power in the process. Inequality will be even worse and legions of Americans will be homeless and without work, trapped in costly urban ghettos where living expenses are astronomical. And all the while, the economists at the Federal Reserve Board and Treasury Secretary Yellen will tell us that inflation is too low.

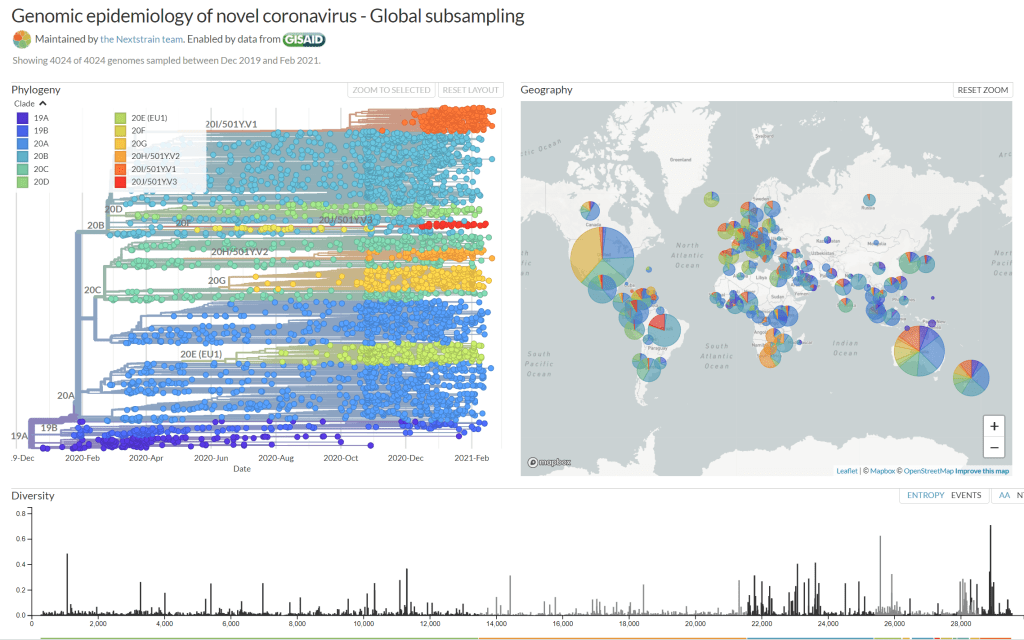

For the longest time, CCP/CoVid-19 has shown remarkable viral genetic stability – remarkable for a zoonotic pathogen that only “recently jumped” species.

Even more remarkable in that the “jump” occurred without any known species as the vector.

And further remarkable that CCP/CoVid-19 is ~96% similar to a virus “discovered” in an abandoned mine in 2013, and only mentioned in 2020 but which no known samples are available (Zhou et al. (2020)).

This stability is particularly remarkable since CCP/CoVid-19 is a single-strand RNA virus – a class of viruses that normally evolve rapidly.

Only after widespread disperson did this stability finally begin to give way to evolution. Note the emergence of the new variants in late Q4, 2020 (upper right of the phylogeny diagram). The sudden ruse in reported COVID-19 cases are attributed to new SARS-CoV-2 variants 501Y.V1 (B.1.1.7) in the UK and 501Y.V2 (B.1.351) in South Africa.

These variants share a key mutation N501Y on the receptor binding domain (RBD) that make them more infectious to humans.

As reported by Tian et al. (2021), RBD N501Y mutations are of higher binding affinity to ACE2 than the wild type, a faster association rate, and slower dissociation rate.

Steered Molecular Dynamics (SMD) simulations on the dissociation of RBD-ACE2 complexes revealed that the N501Y introduced additional π-π and π-cation interaction for the higher force/interaction.

The reinforced interaction from N501Y mutation in RBD should play an essential role in the higher transmission of COVID-19 variants observed to date and likely to continue.

All in, quite “remarkable.”

Reference:

Tian, F., Tong, B., Sun, L., Shi, S., Zheng, B., Wang, Z., … Zheng, P. (2021). Mutation N501Y in RBD of spike protein strengthens the interaction between COVID-19 and its receptor ACE2 (p. 2021.02.14.431117). doi:10.1101/2021.02.14.431117

Zhou, P., Yang, X.-L., Wang, X.-G., Hu, B., Zhang, L., Zhang, W., … Shi, Z.-L. (2020). A pneumonia outbreak associated with a new coronavirus of probable bat origin. Nature, 579(7798), 270–273.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}