“Collectively, our results suggest that the progenitor of Omicron jumped from humans to mice, rapidly accumulated mutations conducive to infecting that host, then jumped back into humans, indicating an inter-species evolutionary trajectory for the Omicron outbreak.”

“SARS-CoV-2 variants of concern (VOC) have arisen independently at multiple locations1,2 and may reduce the efficacy of current vaccines that target the spike glycoprotein of SARS-CoV-23. Here, using a live-virus neutralization assay, we compared the neutralization of a non-VOC variant with the 501Y.V2 VOC (also known as B.1.351) using plasma collected from adults who were hospitalized with COVID-19 during the two waves of infection in South Africa, the second wave of which was dominated by infections with the 501Y.V2 variant. Sequencing demonstrated that infections of plasma donors from the first wave were with viruses that did not contain the mutations associated with 501Y.V2, except for one infection that contained the E484K substitution in the receptor-binding domain. The 501Y.V2 virus variant was effectively neutralized by plasma from individuals who were infected during the second wave. The first-wave virus variant was effectively neutralized by plasma from first-wave infections. However, the 501Y.V2 variant was poorly cross-neutralized by plasma from individuals with first-wave infections; the efficacy was reduced by 15.1-fold relative to neutralization of 501Y.V2 by plasma from individuals infected in the second wave. By contrast, cross-neutralization of first-wave virus variants using plasma from individuals with second-wave infections was more effective, showing only a 2.3-fold decrease relative to neutralization of first-wave virus variants by plasma from individuals infected in the first wave. Although we tested only one plasma sample from an individual infected with a SARS-CoV-2 variant with only the E484K substitution, this plasma sample potently neutralized both variants. The observed effective neutralization of first-wave virus by plasma from individuals infected with 501Y.V2 provides preliminary evidence that vaccines based on VOC sequences could retain activity against other circulating SARS-CoV-2 lineages.”

Abstract: RaTG13 is the closest related coronavirus genome phylogenetically to SARS-CoV-2, consequently understanding its provenance is of key importance to understanding the origin of the COVID-19 pandemic. The RaTG13 NGS dataset is attributed to a fecal swab from the intermediate horseshoe bat Rhinolophus affinis. However, sequence analysis reveals that this is unlikely. Metagenomic analysis using Metaxa2 shows that only 10.3 % of small subunit (SSU) rRNA sequences in the dataset are bacterial, inconsistent with a fecal sample, which are typically dominated by bacterial sequences. In addition, the bacterial taxa present in the sample are inconsistent with fecal material. Assembly of mitochondrial SSU rRNA sequences in the dataset produces a contig 98.7 % identical to R.affinis mitochondrial SSU rRNA, indicating that the sample was generated from this or a closely related species. 87.5 % of the NGS reads map to the Rhinolophus ferrumequinum genome, the closest bat genome to R.affinis available. In the annotated genome assembly, 62.2 % of mapped reads map to protein coding genes. These results clearly demonstrate that the dataset represents a Rhinolophus sp. transcriptome, and not a fecal swab sample. Overall, the data show that the RaTG13 dataset was generated by the Wuhan Institute of Virology (WIV) from a transcriptome derived from Rhinolophus sp. tissue or cell line, indicating that RaTG13 was in live culture. This raises the question of whether the WIV was culturing additional unreported coronaviruses closely related to SARS-CoV-2 prior to the pandemic. The implications for the origin of the COVID-19 pandemic are discussed.

What’s at the root of the supply chain breakdown? That’s a critical question but the answer is almost irrelevant. The supply chain is a complex dynamic system of immense scale. It is of a complexity comparable to the climate as a system.

This means that exact cause and effect cannot be computed because the processing power needed exceeds the combined processing power of every computer in the world.

Most people have some notion of how supply chains work, but few understand how extensive, complex and vulnerable they are. If you go to the store to buy a loaf of bread, you know that the bread did not mystically appear on the shelf.

It was delivered by a local bakery, put on the shelf by a clerk, you carried it home and served it with dinner. That’s a succinct description of a supply chain – from baker to store to home.

Yet that description barely scratches the surface. What about the truck driver who delivered the bread from the bakery to the store? Where did the bakery get the flour, yeast and water needed to make the bread? What about the ovens used to bake the bread? When the bread was baked, it was put in clear or paper wrappers of some sort. Where did those come from?

Even that expanded description of a supply chain is just getting started in terms of a complete chain. The flour used for baking came from wheat. That wheat was grown on a farm and harvested with heavy equipment. The farmer hires labor, uses water and fertilizer and sends his wheat out for processing and packaging before it gets to the bakery.

The manufacturer who built the oven has his own supply chain of steel, tempered glass, semiconductors, electrical circuits and other inputs needed to build the ovens. The ovens are either hand crafted (engineered-to-order) or mass produced (made-to-stock) in a factory that may use either assembly lines or manufacturing cells to get the job done.

The factory requires inputs of electricity, natural gas, heating and ventilation systems, and skilled labor to turn out the ovens.

The store that sells the bread is on the receiving end of numerous supply chains. It also requires electricity, natural gas, heating and ventilation systems and skilled labor to keep the doors open and keep merchandise in stock. The store has loading docks, back rooms for inventory, forklifts and conveyor belts to move its merchandise from truck to shelf.

Every link in these supply chains requires transportation. The farmer relies on trucks or rail for deliveries of seeds, fertilizers, equipment and other inputs. The oven manufacturer also relies on trucks or rail for deliveries of its inputs, including oven components. The bakery and the store rely mainly on trucks for deliveries of their inputs and the finished loaves of bread. The consumer relies on her automobile to get to the store and return home.

These transportation modes have their own supply chains involving truck drivers, train engineers, good roads, good railroads, rail spurs and energy supplies to keep moving and keep deliveries on time.

This entire network (farms, factories, bakeries, stores, trucks, railroads and consumers) relies on energy supplies to keep working. The energy can come from nuclear reactors, coal-fired or natural gas-fired power plants or renewable sources fed to a grid of high-tension wires, substations, transformers and local connections to reach the individual user.

Everything described above sits somewhere in a complex supply chain needed to produce one loaf of bread. Now take everything else in the grocery store (fruits, vegetables, meat, poultry, fish, canned goods, coffee, condiments and so on) and imagine the supply chains needed for each one of those products.

Then take all the other stores in the shopping center (home goods, clothing, pharmacy, hardware, restaurants, sporting goods) and imagine all the goods and services available from those vendors and the supply chains behind each and every one of those.

In case you think I have exaggerated the components and steps in making a loaf of bread in the above example, I didn’t. The example above is a grossly simplified description of the actual supply chain.

A full description of the needed supply chain would reach back further (where do the seeds for the wheat come from?) and branch off in tangential directions (where do the bread wrappers originate?).

A full description of the loaf of bread supply chain with choice of vendor analysis, quality-control tests and bulk purchase discounts among other decision tree branches could easily stretch to several hundred pages.

Now consider all of the supply chain links and possible bottlenecks described above are purely domestic. But very few supply chains are actually that local. CEOs, logistics engineers, consultants and politicians have spent the past 30 years making supply chains global.

You’ve heard discussion of globalization since the early 1990s. What one may not have realized is that the process that was being globalized was the supply chain.

You know your iPhone comes from China. Did you know that the specialized glass used in the iPhone comes from South Korea? Did you know the semiconductors in the iPhone come from Taiwan? That the intellectual property and design of the iPhone are from California?

The iPhone includes flash storage from Japan, gyroscopes from Germany, audio amplifiers, battery chargers, display port multiplexers, batteries, cameras and hundreds of other advanced parts.

In total, Apple works with suppliers in 43 countries on six continents to source the materials and parts that go into an iPhone. That’s a quick overview of the iPhone supply chain. Of course, every supplier in that supply chain has its own supply chain of sources and processes. Again, supply chains are immensely complex.

Once the global perspective is added, we have to expand our transportation options from trucks and trains to include ships and planes. That means ports and airports are additional links in the chain.

Those facilities have their own links and inputs including cranes, containers, port authorities, air traffic controllers, pilots, captains and the vessels themselves. And to our list of trucks, trains, ships and planes we can add pipelines that transport liquids such as petroleum, gasoline and natural gas.

You get the idea. Supply chains may be hidden but they are everywhere. They are interconnected, densely networked and unimaginably complex.

The touchstone of these efforts was the idea of just-in-time inventory (JIT). If you’re installing seats on an automobile assembly line, it is ideal if those seats arrive at the plant the same morning as the installation. That minimizes storage and inventory costs. The same is true for every part installed on the assembly line. The logistics behind this are daunting but can be managed with state-of-the-art software.

All these efforts are fine as far as they go. The cost savings are real. The supply chains are efficient. The capacity of this system to keep a lid on costs is demonstrable.

The supply chain revolution since the early 1990s has been about cost reduction, which gets passed to consumers in the form of lower prices. That practically explains the entire phenomenon.

There’s only one problem. The system is extremely fragile. When things break down, everything gets worse at the same time. One missed delivery can result in an entire assembly line shutting down. One delayed vessel can result in empty shelves. One power outage can result in a transportation breakdown.

In a nutshell, that’s what has happened to the global supply chain. There’s a lack of redundancy. The system is not robust to shocks. The shocks have occurred nevertheless (pandemic, trade wars, China-U.S. decoupling, bank collateral shortages and more) and the system has broken down.

The failures have cascaded. Delays in receiving commodity inputs in China have resulted in manufacturing delays for exports. Energy shortages in China have resulted in further disruption of steel production, mining, transportation and other basic industries.

Port delays in Los Angeles have resulted in component and finished goods delayed in the U.S. Semiconductor shortages have halted production of electronics, appliances, automobiles and other consumer durables that rely on automated applications. You’ve seen how complex the system is.

The bottom line is if supply chains are breaking down, the economy is breaking down. If the economy breaks down, the breakdown of social order is not far behind.

And the costs of social disorder are far higher than any possible savings from supposedly efficient supply chains.

Sarah Connor (Terminator 2): “The Survivors of the nuclear holocaust called the war Judgement Day. They lived only to face a new nightmare: the way against the machines.”

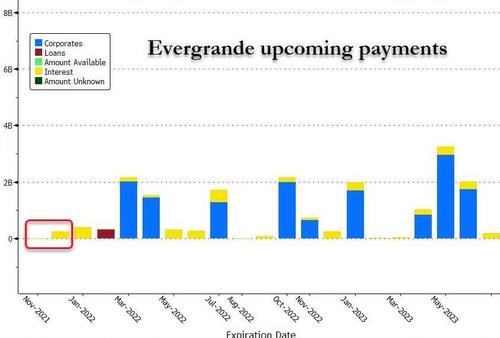

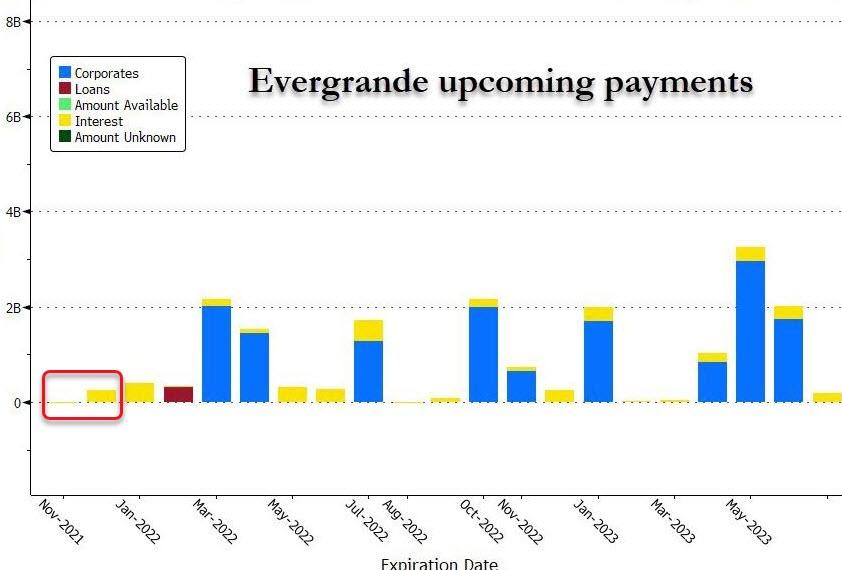

Specifically, offshore (dollar) bondholders did note receive coupon payments by the end of a 30-day grace period, pushing the cash-strapped property developer closer to formal default.

And after this missed payment, there are billions more coming due… and soon ($300 billion in total liabilities)

S&P says it continues to believe that a default by the Chinese developer looks inevitable:

Evergrande’s “liquidity remains extremely weak,” according to the ratings firm.

Fitch piled on with a downgrade to C from CCC-, saying in a statement:

“Default or default-like process has begun, based on the company’s announcement that it has not made payments or reached an agreement with creditors regarding its offshore financing, after it received notice from creditors demanding payment on financings with principal amount of around $651 million following recent rating actions by rating agencies.”

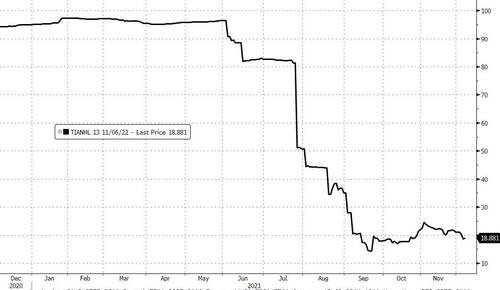

Bond prices are already priced for that ‘inevitable’…

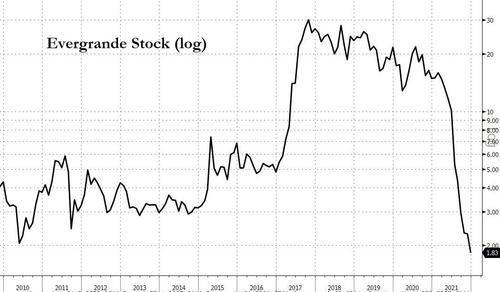

As are Evergrande’s stock price…

Notably, as WSJ reports, the debt blowup is also a landmark in China’s changing attitude to corporate defaults, which were once rare but are growing more common, both onshore and offshore. Recent failures include the chip maker Tsinghua Unigroup and the once-hyper-acquisitive conglomerate HNA Group, which is now undergoing a court-led restructuring in China.

The shifting stance on defaults is partly a recognition that after a huge run-up in the country’s corporate debt pile in recent years, Beijing can’t afford too many bailouts.

A barrage of statements from Chinese regulators, several of which landed just minutes after Evergrande’s announcement on Friday, suggested authorities are striving to contain the fallout on homeowners, the financial system and the broader economy rather than orchestrate a bailout.

And, as a reminder, another developer – Kaisa – is on course for default this week unless it can reach a last-minute agreement with creditors to delay payment. The firm has $11.6 billion in outstanding dollar debt, making it the nation’s third-largest issuer of such notes among property firms.

As Reuters reports, failure by Evergrande to make $82.5 million in interest payments due last month would trigger cross-default on its roughly $19 billion of international bonds and put the developer at risk of becoming China’s biggest defaulter – a possibility looming over the world’s second-largest economy for months.

Non-payment by Kaisa would push the 6.5% bond of Kaisa, China’s largest holder of offshore debt among developers after Evergrande, into technical default, triggering cross defaults on its offshore bonds totalling nearly $12 billion.

With the United States cutting back its own oil production in the name of “climate”, and fueling double-digit inflation, why would we consider shooting ourselves in the foot over Ukraine?

Well, maybe Hunter Biden knows – he’s pulled enough dough out of Ukraine’s oligarchs for himself with “10% for the Big Guy.”

One might want to be careful poking bears. Not our Regime – give lunatics access to nuclear weapons and, well, it reminds me of what Sadavir Errinwright had to say:

“You give a monkey a stick, inevitably he’ll beat another monkey to death with it.”

“The Expanse”

Knocking 12% of global oil production out of USD-denominated SWIFT and into BTC is something only Michael Saylor might dream of.

Here’s Tyler to report the latest lunacy from the Progressive Regime in DC.

Biden Mulls Cutting Russia Off SWIFT Ahead Of Putin Call In “Nuclear Option” Ukraine Response

CNN and others are reporting just a day ahead of the much anticipated video call between Russian President Vladimir Putin and US President Joe Biden that the White House is mulling “nuclear option” level actions against Moscow should it launch a military offensive against Ukraine – which US intelligence has lately said could be imminent based on assessing that some 175,000 troops have been mustered in the Crimea and regions near Ukraine’s eastern border.

This includes discussion of the possibility of disconnecting Russia from the SWIFT international payment system, seen as the most drastic potential measure which further includes fresh sanctions on Putin’s inner circle and on Russian energy producers.

The Kremlin has of course vehemently rejected the Ukraine threat accusations, saying it’s free to move its own troops wherever it sees fit within the Russian Federation’s sovereign territory and borders.

But the White House is now threatening the following, according to CNN on Monday:

People familiar with the discussions said new economic sanctions could target a variety of sectors, including energy producers and Russian banks. The new sanctions could also go after Russia’s sovereign debt.

They are also likely to go after top Russian oligarchs, limiting their ability to travel and potentially cutting off access to American banking and credit card systems.

And in particular, the “nuclear option” – which is now grabbing headlines…

Officials have also been weighing disconnecting Russia from the SWIFT international payment system, upon which Russia remains heavily reliant, according to two sources familiar with the discussions. This is being considered a “nuclear” option. The European Parliament passed a nonbinding resolution in the spring calling for such a move should Russia invade Ukraine, and the US has been discussing it with EU counterparts.

On Russia’s side, it has the “energy option” vis-a-vis Europe – something that the US has long warned the EU about, especially when it comes to the controversial Nord Stream 2 pipeline coming online. “The fear is Russia then tries to retaliate by holding back production,” a top US official told CNN.

NEW: "Pretty damn aggressive" sanctions package in works by US & Europe should Russia invade Ukraine, sources say. 1 option "very much on the table": disconnecting Russia from SWIFT intl payment system & denying Russian energy producers from debt markets. https://t.co/HGwd5H6Upt

“We have put together a pretty damn aggressive package,”an unnamed administration official additionally said to CNN, adding further that if Russia invades Ukraine “the US and Europe together will impose the worst economic sanctions that have ever been imposed on a country, outside of Iran and North Korea,” according to the report.

It should be noted that with such an “option” in play, if things actually escalated to the historically unprecedented level of Russia’s being blocked from SWIFT – such a scenario would mark a huge future day for cryptos, given cryptos have been suggested as the first space Putin would likely migrate to amid total isolation for the West-based payment system used by banks around the world.

By Mark Cranfield, Bloomberg Markets Live commentator and analyst

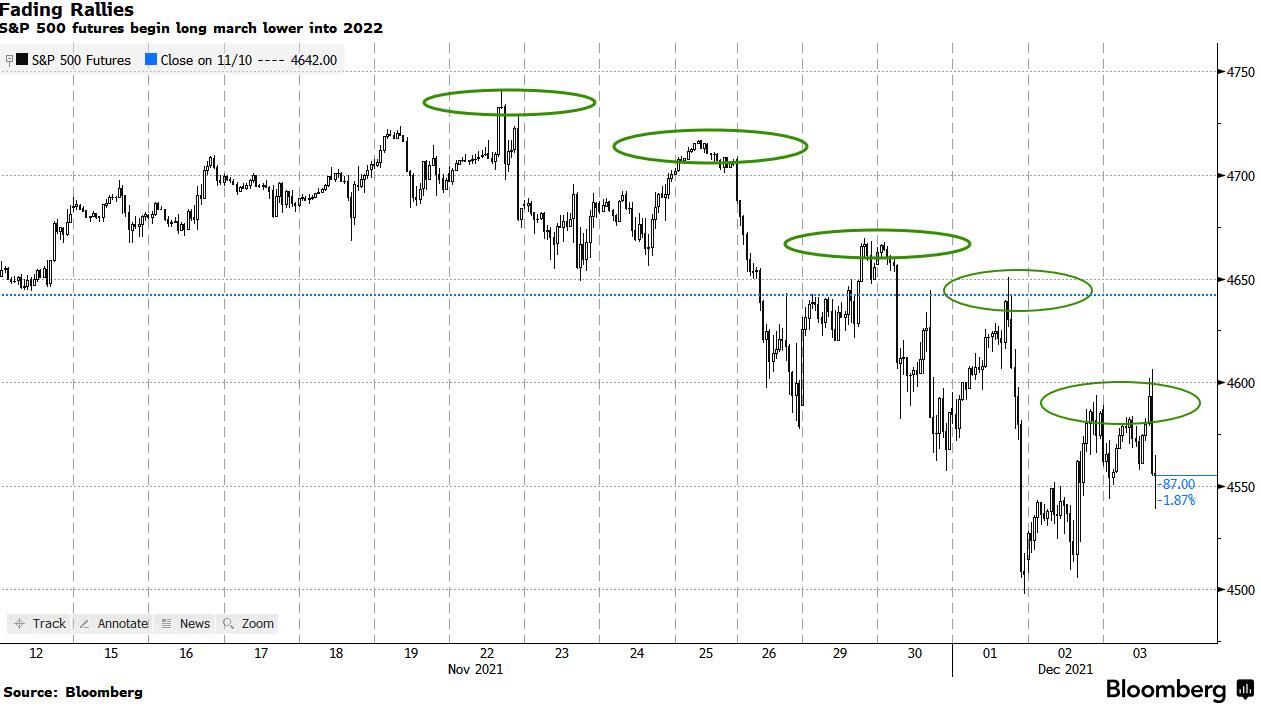

S&P 500 futures have a distinctly bearish tone after a week of whiplash trading, which began with the post-Thanksgiving Day meltdown.

Though it hasn’t been a one-way street lower, intraday bounces for the contract have been fading at lower peaks.

That is a clear enough signal for short-term traders to see if they are positioned for a declining asset.

And even though non-farm payrolls did miss forecasts, the Fed won’t be derailed from its path to tighter policy.

Moreover, the blackout period ahead of the Dec. 15 FOMC decision begins this weekend, which means there won’t be any walking back of the hawkish noises heard this week.

The decline from November’s peak for S&P futures is starting to look like the turning point in a long march lower, which will set the pace for a global bear market next year.

Retail has broken its channel. I was bragging about my brilliant bear call from the tippy-top of the channel but apparently the comically-overvalued market is starting to dawn on even non-Slope readers, so channels like this are getting shattered.

Energy sector is doomed. The raging success we’ve had with bearish calls on energy of the past month are, I believe, merely the beginning.

Biotechnology sector, which would make us all six foot tall, blonde-haired, blue-eyed Adonis-like creatures, appears to have hit a bump in the road. This entire sector has already been nuked, but it seems to me only the first few ICBMs have exploded, and the global thermonuclear war has only just started. There’s nothing but empty air below the now-broken top.

The predictions focus on a series of unlikely but underappreciated events which, if they were to occur, could send shockwaves across financial markets:

The plan to end fossil fuels gets a rain check

Facebook faceplants on youth exodus

The US mid-term election brings constitutional crisis

US inflation reaches above 15% on wage-price spiral

EU Superfund for climate, energy and defence announced, to be funded by private pensions

Women’s Reddit Army takes on the corporate patriarchy

India joins the Gulf Cooperation Council as a non-voting member

Spotify disrupted due to NFT-based digital rights platform

New hypersonic tech drives space race and new cold war

Medical breakthrough extends average life expectancy 25 years

As culture wars rage across the world, it’s no longer a question of if we get a socioeconomic revolution, but a question of when and how. But which revolutionary prediction do you think is most likely?

Saxo CIO Steen Jakobsen summarizes the theme for 2022 Outrageous Predictions is Revolution.

There is so much energy building up in our inequality-plagued society and economy. Add to that the inability of the current system to address the issue and we need to look into the future with the fundamental outlook that it’s not a question of whether we get a revolution, but more a question of when and how. With every revolution, some win and some lose, but that’s not the point—if the current system can’t change but must, a revolution is the only path forward.

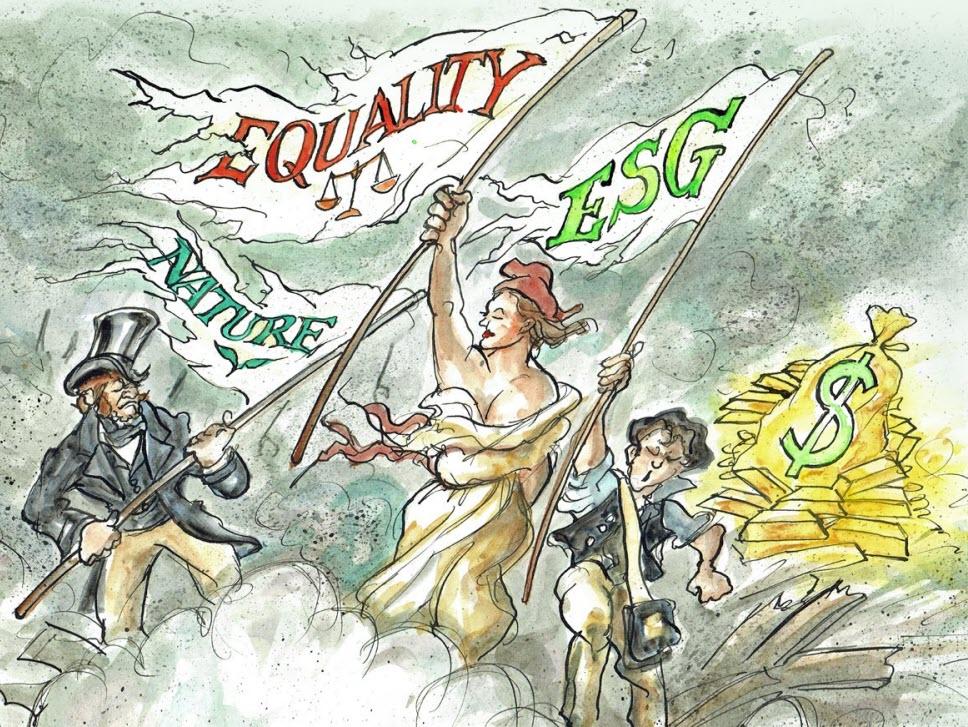

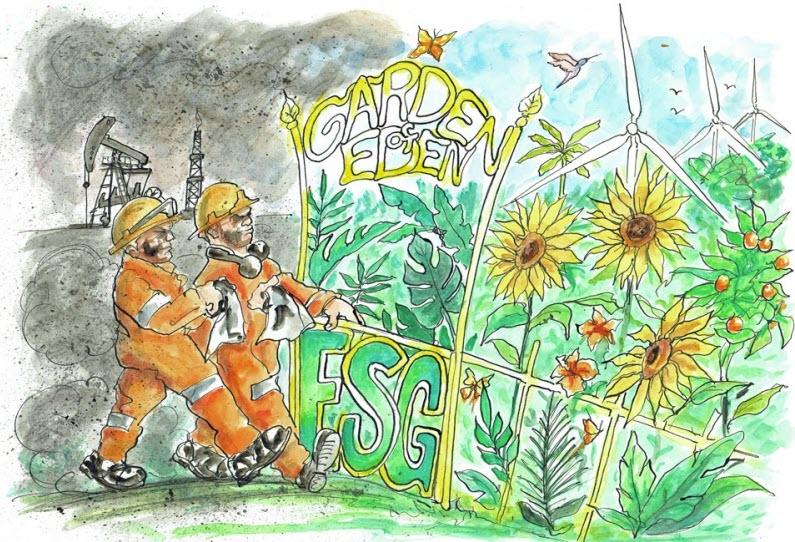

A culture war is raging across the globe and the divide is no longer simply between the rich and the poor. It’s also the young versus the old, the educated class versus the less educated working class, real markets with price discovery versus government intervention, stock market buy-backs versus R&D spending, inflation versus deflation, women versus men, the progressive left versus the centrist left, virtual signalling on social media versus real changes to society, the rentier class versus labour, fossil fuels versus green energy, ESG initiatives versus the need to supply the world with reliable energy—the list goes on.

What’s interesting for me, having done this Outrageous Predictions list for twenty years, is that all of the above issues point to a cycle ending rather than a continuation of more of the same. Post-pandemic (well, mostly) the market is hoping that things will continue as before, but as an old mentor of mine used to say, when I answered one of his questions with “I hope”: “Listen, son, save hope for church on Sundays, and come back when you have something more concrete.” The year 2022 is likely to see far less of what markets are hoping for and far more in the way of volatility as revolutionary movements kick into gear that challenge the status quo as we grope our way towards a new paradigm. Some of these movements will get things right, some of them will make mistakes, but we need to get started. Pretty much everything needs to change if we are to achieve zero emissions, less inequality, stable energy and importantly, more productivity.

2021 was a year in which we thought we could firmly put Covid behind us, but as 2022 rolls into view, we’re simply not there yet. It was a year with unprecedented fiscal transfers, especially to lower-income households, which created excess demand in a geopolitically and supply chain–fragmented world. The physical world simply became too small to absorb the good, if misguided, intentions of politicians and central banks to keep the economy on an even keel. Now we find ourselves with an energy crisis on our hands—and that’s not an outrageous call. But how we deal with it could create both policy mistakes and fundamental changes. A cold winter, for example, could spark a counter-revolution against the current alternative energy narrative, requiring that we reconfigure our expectations around how quickly we can abandon fossil fuels (Outrageous Prediction number 1 for 2022!) and even reclassifying nuclear energy as green. Doing anything else is simply not viable if we want to avoid a collapse in the real economy.

We do realise that the Revolution theme for OP 2022 can create negative associations. To many of us, the word Revolution calls forth the 1789 French Revolution with its call for “Liberty, Equality, and Fraternity”, but also the Russian Revolution and its “smash the capitalists” principles.

But our intent is the broader definition of revolution: not the physical overthrowing of governments, but eurekalike moments that trigger a change of thinking, a change of behaviour and a rejection of the unsustainable status quo. Hopefully, each of the Outrageous Predictions echoes that general point, with a couple of the revolutions triggered by the “involuntary” implications of technical progress: hypersonic missiles and longevity therapy. We need more liberty from governments in some areas, like a less heavy-handed monetary policy and the moral hazard of unproductively backstopping markets it brings. And we need more regulation in others, like avoiding the dangers of a hyper-financialised economy, too-powerful monopolies and inequality. Most urgently, we need to provide a brighter outlook for the world’s young people and better cooperation among nations instead of the present trend away from globalisation and multilateral institutions.

We collaborated globally on Covid vaccines in 2020 and 2021. Now we need a new Manhattan Project–- type endeavour to set the marginal cost of energy, adjusted for productivity, on the path to much lower levels while eliminating the impact of our energy generation on the environment. Such a move would unleash the most significant productivity cycle in history: we could desalinate water, make vertical farms feasible almost anywhere, enable the leap to quantum computing, and continue to explore new boundaries in biology and physics.

Remember that the world is forever evolving if at varying speeds, while business and political cycles are always finite. We are betting that in 2022 the speed of evolution kicks up a few notches into a revolutionary state as a new cycle gets under way. ‘Change is good’ needs to be the new mantra, or at minimum: “trial and error”. Let’s at least try and err some more rather than trying to forever kick the can down the road!

Finally, we must emphasise our annual caveat, that these Outrageous Predictions should not be seen as our official view on the market and politics. This year, more than ever, we’re trying to provoke you and ourselves to think outside the box and to engage in discussing the important topics we raise. Let the fun, and the future, begin.

* * *

The plan to end fossil fuels gets a rain check

Summary: Policymakers kick climate targets down the road and support fossil fuel investment to fight inflation and the risk of social unrest while rethinking the path to a low-carbon future.

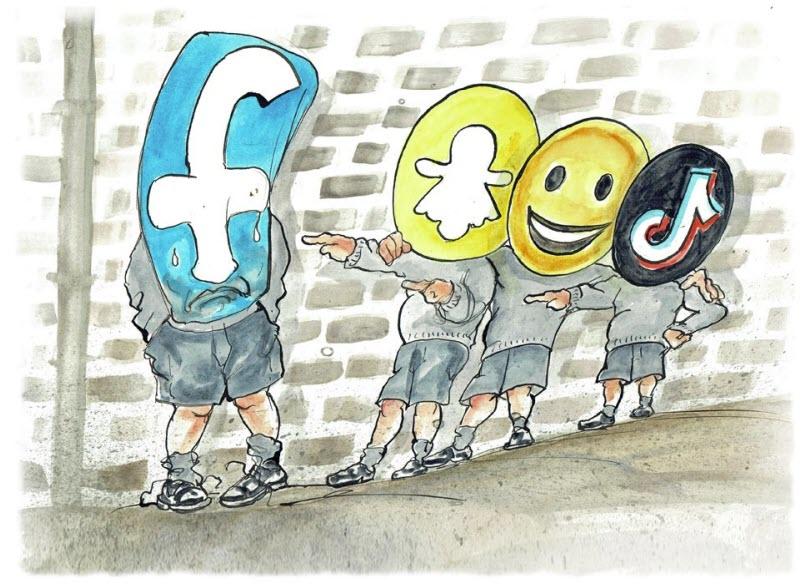

Facebook faceplants on youth exodus

Summary: The young abandon Facebook’s platforms in protest against their mining of personal information for profit; the attempt by Facebook parent Meta to reel them back in with the Metaverse stumbles.

The US mid-term election brings constitutional crisis

Summary: The US mid-term election sees a stand-off over the certification of close Senate and/or House election results, leading to a scenario where the 118th Congress is unable to sit on schedule in early 2023.

US inflation reaches above 15% on wage-price spiral

Summary: By the fourth quarter of 2022, US CPI inflation reaches an annualized 15% as companies bid up wages in an effort to find willing and qualified workers, triggering a wage-price spiral unlike anything seen since the 1970’s.

EU Superfund for climate, energy and defence announced, to be funded by private pensions

Summary: To defend against the rise of populism, deepen the commitment to slowing climate change, and defend its borders as the US security umbrella recedes, the EU launches a bold $3 trillion Superfund to be funded by pension allocations rather than new taxes.

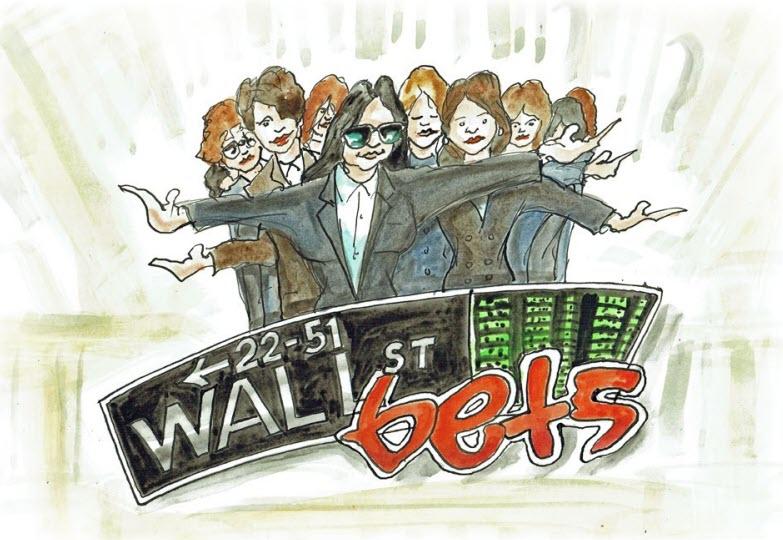

Women’s Reddit Army takes on the corporate patriarchy

Summary: Mimicking the meme stock Reddit Army tactics of 2020-21, a group of women traders launch a coordinated assault on companies with weak records on gender equality, leading to huge swings in equity prices for targeted companies.

India joins the Gulf Cooperation Council as a non-voting member

Summary: The world’s geopolitical alliances will lurch into a phase of drastic realignment as we have an ugly cocktail of new deglobalising geopolitics and much higher energy prices.

Spotify disrupted due to NFT-based digital rights platform

Summary: Musicians are ready for change as the current music streaming paradigm means that labels and streaming platforms capture 75-95 percent of revenue paid for listening to streamed music. In 2022, new blockchain-based technology will help them grab back their fair share of industry revenues.

New hypersonic tech drives space race and new cold war

Summary: The latest hypersonic missile tests are driving a widening sense of insecurity as this tech renders legacy conventional and even nuclear military hardware obsolete. In 2022 a massive hypersonic arms race develops among major militaries as no country wants to feel left behind.

Medical breakthrough extends average life expectancy 25 years

Summary: Young forever, or for at least a lot longer. In 2022, a key breakthrough in biomedicine brings the prospect of extending productive adulthood and the average life expectancy by up to 25 years, prompting projected ethical, environmental and fiscal crises of epic proportions.

When debt overwhelms a shrinking working population – the ever widening chasm of an economy serving a barely growing “We the People” versus an economy twisted/tortured to serve the needs of an infinitely “growing” financial system serving “the Few”.

The fuel for economic growth, particularly in a nation running gargantuan trade and budget deficits, is population growth. Not any population growth, but working age population growth. It is the growth of this cohort that drives potential employment growth, potential consumer growth, potential homeownership growth. Absent that growth, the means to continue “growing” is to substitute cheaper debt, more debt, more stimulus, etc. and claim those substitutes as real growth.

There is a natural level of “full employment” that has been established since the full inclusion of women in the labor force. This is to say there are only so many persons among the working age population willing, capable, and available to work. Once that cohort of available workers is employed…full employment is achieved and the fuel for further organic growth is spent. Absent further potential growth (because no more fuel exists, we call this a “recession”).

Absent that working age population growth, the only means to create more potential “fuel” are massive job loss events (given names such as “sub-prime crisis” and “Corona-Virus crisis”). Then, in the wake of these mass layoff events, large “job gains” can be claimed via ZIRP, federal debt / stimulus, Federal Reserve QE. But they are not job gains…they are simply re-employing the same cohort.

So, due to the decelerating growth, and now declining working age population versus ever more aggressive means to re-employ those same persons…the crisis are coming faster and hitting more intensely due to the demographic reality we now face. These “full employment” moments where stimulative policy led to an exhaustion of potential employees have taken place in ’89, ’00, ’07, ’19, and now again in 2022.

I’ll detail this impact first among the 25 to 54 year old population and then widen out the the broadest possible working age population of 15 to 74 year olds.

Below, 25 to 54 year old population, employees. Core population growth began decelerating end of the century and ceased as of 2007. Those employed among this age group have essentially stagnated since 2000…but the chart below shows an additional 2 million more employees than are currently employed which is likely to be achieved by early 2022.

Below, adding in federal funds rate (black dashed), marketable federal debt (red), and Federal Reserve balance sheet (QE, yellow line).

Below is the critical chart…with the addition of those 2 million more jobs (this cohort lost about 14 million jobs, has regained 12 million) against a total 25 to 54 year old population which has not grown…we are at full employment. Point is, by early to mid 2022, approximately 80.5%’ish employment/population ratio will be achieved…and that is typically the end of the line where the engine simply runs out of gas. Typically, “full employment” coincides with initiation of interest rate cutting cycles, federal deficit spending, and more recently large Federal Reserve balance sheet growth (yes, just as the Fed is initiating a QE tapering and discussing interest rate hikes and the federal government is reducing stimulus?!?). This combination of full employment versus tightening is almost sure to initiate deceleration and recession.

Below, looking at the largest possible working age population, 15 to 74 year olds and those employed among them. Note the large deviation from trend line in those employed versus population, This is the declining labor force participation of the only portion of this population that is growing…the 65+ aging population. The employed assumes 2 million more employees than are presently employed against little to no population growth.

Again, adding in federal funds rate, debt, and Federal Reserve balance sheet.

I save the most important for last. While the 25 to 54 year old population isn’t growing, the “full employment” ratio is generally flat at about 80.5%. Conversely, the still growing 15 to 74 year old population (thanks entirely to the elderly portion of this population) is seeing a continual decline in what constitutes “full employment”. Thanks to the participation levels among the 65+, full employment (and the end of economic “fuel”) will only continue to decline regardless continued ZIRP (NIRP?), QE, federal debt/stimulus, MMT/UBI, etc.

Demographics simply are and care not what the Federal Reserve or Wall Street or the White House need to bridge the ever widening chasm of an economy serving a barely growing “We the People” versus an economy twisted/tortured to serve the needs of an infinitely “growing” financial system serving “the Few”. This series of supposed financial crisis have been nothing of the sort…they are so obvious and predictable. 2022 is just the next demographic chapter where full employment is achieved. Regardless how it is cloaked via some ongoing or new version of “crisis”, be prepared because this will almost surely be the launch of unimaginable debt, NIRP, QE, UBI, MMT, and acronyms not even in existence yet. Whether it is called the “great reset” or hyper-inflation or whatever…this is the end of one historic period and the beginning of another.

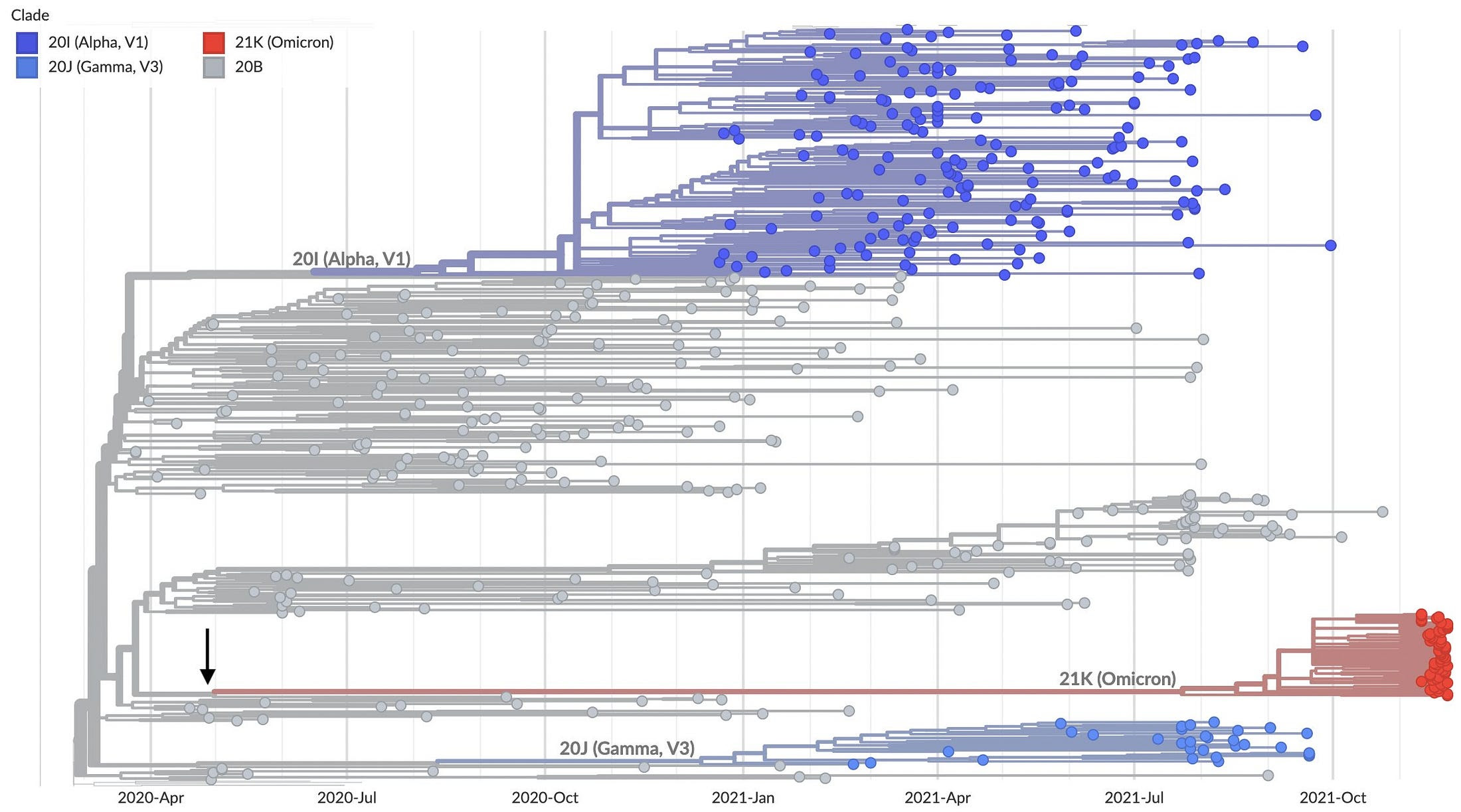

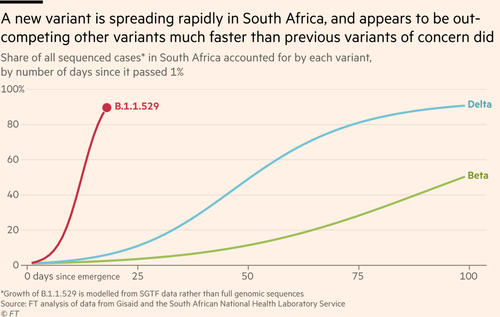

Summarizing of our post from last night (which we urge everyone to read) for those who are just now waking up to the global chaos resulting from the B.1.1.529 variant, which today got the Greek letter designation Omicron, skipping the widely expected letter Nu (and certainly the one following it, Xi), here is what we know, courtesy of Newsquawk, Credit Suisse and Citi.

Background

Regarded as the most heavily mutated variant of the Coronavirus, thus far, as it has 32 mutations in the spike protein and 50 overall. More specifically, scientists have highlighted that there are 10 mutations vs 2 in the Delta variant regarding the receptor binding domain, which is the portion of the virus that makes initial contact with cells.

The Nu variant was identified 5 days ago initially in Botswana with subsequent confirmation and sequencing in South Africa with about 100 confirmed cases. Cases have been detected in Israel and Hong Kong and as of this morning, in Belgium.

Sequencing data suggests 8.1.1.529 has a different evolutionary pathway, but shares a few common mutations with the C.1.2, Beta and Delta variants.

That said, as we cautioned last night, a significant number of mutations may not necessarily be a ‘negative’ as it is dependent on how these mutations function, which scientists are yet to establish. Then again, since it is the job of science to fearmonger so that Pfizer can buy an even bigger yacht, assume it will be “very very horrifying” until proven innocuous.

Is it more deadly

It is currently too early to determine if the new variant has higher mortality than previous variants. Reported cases only started rising in South Africa on 19 November, so any impact on hospitalizations and COVID-related deaths will not have yet emerged.

Testing and Detectability

Tulio de Oliveria, the Director of the Centre for Epidemic Response & innovation (CERI), South Africa, has written that the variant can be detected by a normal PCR test and as such it will be “easy for the world to track it”. It wasn’t immediately clear if this is one of those “excess false positive PCR tests” but it’s safe to assume for now that it is.

According to Credit Suisse, “one silver lining may come in the ease of identifying this variant via qPCR tests. B.1.1.529 has a deletion within the s-gene which can be identified easily via widely-used PCR tests. More complex sequencing analysis is needed to differentiate the delta variant. This will help track the spread of B.1.1.529, both within Southern Africa and across the globe.”

How widespread is it

As of Thursday there were almost 100 cases detected in South Africa, where it’s become the dominant strain among new infections. Early PCR test results showed that 90% of 1,100 new cases reported Wednesday in the South African province that includes Johannesburg were caused by the new variant, according to de Oliveira.

In neighboring Botswana, officials recorded four cases on Monday in people who were fully vaccinated. In Hong Kong, a traveler from South Africa was found to have the variant, and another case was identified in a person quarantined in a hotel room across the hall. Israel has also identified one case in a man who recently traveled to Malawi. Belgium has also reported two new cases.

According to de Oliveira, this new variant, B.1.1.529 “seems to spread very quick! In less than 2 weeks now dominates all infections following a devastating Delta wave in South Africa (Blue new variant, now at 75% of last genomes and soon to reach 100%)”

This new variant is really worrisome at the mutational level. South Africa and Africa will need support (financially, public health, scientific) to control it so it does not spread in the world. Our poor and deprived population can not be in lockdown without financial support. pic.twitter.com/CeJIXudUIA

Oliveria, explains that the new variant is spreading very quickly, in under two-weeks it is now dominating all infections in South Africa following the Delta waves domination – writing that it the variant is “now at 75% of last genomes and soon to reach 100%”.

Additionally, the virus contains mutations that have been seen in other variants and appear to make transmission easier.

Outside of Africa, two cases have been reported in Hong Kong, one from a traveller from the region and another who was quarantining in the adjacent hotel room. Most recently, a case has been reported in Israel.

In response to this, the UK has placed much of southern Africa on the red list, with Israel India, Japan and Singapore also taking similar measures. Additionally, EU Commission President von der Leyen is to propose activation of the emergency air brake, to halt travel from southern Africa.

Vaccines

It is too early to accurately determine the vaccine response to the new variant. However, the significant number of variants increase the likelihood that current vaccines, which were designed with the original COVID-19 strain in mind, may be less effective.

Known variants include those that make it more challenging for antibodies to recognise their presence.

Laboratory testing is already underway according to the South Africa National Institute for Communicable Diseases Initial thoughts from the institute are that partial immune escape is likely, a view that seems possible given the numerous mutations in comparison to the sequence that existing vaccines were designed against. The first view on this to be from in vitro immunogenicity test or perhaps from computer modelling of the sequence. Credit Suisse estimates initial lab data could take less than 1 week to generate given the sequence is already known and work is already ongoing.

New Vaccine Would be Available in 100 days

According to Pfizer, if a vaccine-escape variant emerges, the company expects to develop, produce a tailor-made vaccine against that variant in 100 days.

Impact of efficacy of existing drugs antibodies is unknown.

There have been significant advances in treatment of COVID since it emerged in the disease waves of 2020: the use of widely-available steroids, and anti-inflammatory drugs, such as Roche’s Actemra have significantly improved survival outcomes.

More recently, antibody therapies targeting COVID (LLY, REGN/Roche, AZN) have significantly improved outcomes against COVID variants to date. It will need to be seen if their efficacy is equal against the new B1.1.529 variant.

Lastly the recent positive data from oral anti-viral agents (PFE, MRK/Ridgeback) may also have the potential to slow the spread of any new waves of COVID. The effectiveness of these treatments against new variants of concern will need to be tested, but lab results should be expected relatively quickly. In-human studies should also yield results relatively quickly if they are run in areas where the prevalence of 8.1.1.529 is high.

What’s next

According to Citi, concern over Nu needs to be balanced against the failure of other concerning variants such as Beta (also first identified in Africa) to out-compete delta.

The next two weeks will be critical to: (i) determine whether Nu outcompetes delta in high delta prevalence countries (2-3 weeks), (ii) engineered pseudoviruses for Nu to determine neutralization by serum of vaccination and previously infected patients (2-4 weeks), and (iii) real world data to determine rates of hospitalisation and death (c. 6-8 weeks). The implementation of travel restrictions and public health measures may push back some of the above timeline estimates. Novel oral anti-virals should retain activity against Nu but resistance may emerge with time.

Some times saying less can say more. Given that, I’m going to offer four variables relating to housing and hopefully let them and their relationships do the talking.

1- US median home price versus total US employees. 1970 through 2021 (YE est.).

Since 2019:

—Home prices +28%

—Total Employees -1.9%

2- Year over year changes in median house prices versus YoY changes in total US employees. Worth noting the accelerating divergences between home price appreciation and employees highlighted in the four boxes below.

3- Same chart below, but inclusive of periods of Federal Reserve rate cutting cycles. Hmmm.

4- Time to add in one last variable, year over year changes in Federal Reserve holdings of MBS (mortgage backed securities). Hmmmm.

As the Federal Reserve embarks on its tapering (decelerating purchases) of MBS, as the growth in employment has begun its natural deceleration as “full employment” of the working age population nears (detailed below), and as inflationary pressures suggest the Fed should consider rate hikes…remember these charts and the impact on home prices. Why US will reach full employment in 2022 and cease further employment growth…detailed below. 1- 15 to 64 year old US population versus those employed among that age group.

1.1- While many housing pundits discuss a housing shortage, I offer the same view of the working age versus total US housing units.

1.2- To ensure the “housing shortage” is shown in full, I show the full US population to total housing ratio…and rather than a shortage, the US is at an all time high of housing units per capita (back to the previous peak seen in 2008).

2- Year over year change in 15 to 64 year old population versus year over year changes in employment among them. Population growth is the natural governor to potential employment growth…regardless interest rate cuts, debt, QE.

3- Pulling together the variables, working age population / those employed among them versus the Federal Funds rate % (black), marketable US federal debt (red), and Federal Reserve balance sheet (yellow). As population growth has decelerated, federal government and Federal Reserve have substituted cheaper debt, more debt, and QE to maintain artificially high consumption / “growth”.

4- Lastly, the population to employment ratio is rapidly heading for “full employment” typically hit around 72% (that is, since women became fully integrated into the labor force). At that 72%’ish point, typically employment growth ends, economic growth ends, and the next round of interest rate cuts / federal debt / Fed balance sheet growth ensues.

So, just as the Federal Reserve is attempting to tame a housing bubble via undertaking tapering and discusses dot plot rate hikes in 2022, and inflation runs amok…the demographic / employment cycle is already nearly tapped out…typically the sign of impending Federal Reserve rate cuts / balance sheet expansion, and federal government debt fueled stimulus. Those concerned about impending hyper-monetization perhaps leading to hyper-inflation quickly followed by a hyper-deflationary depopulationary depression may not be as crazy as they seem?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}